May NFP growth at +172K outpaces +85K Bloomberg consensus (87K surprise vs. 53K Mean Absolute Revision goinng from 1st-3rd release in 2025), on top of upward revisions in April and March.

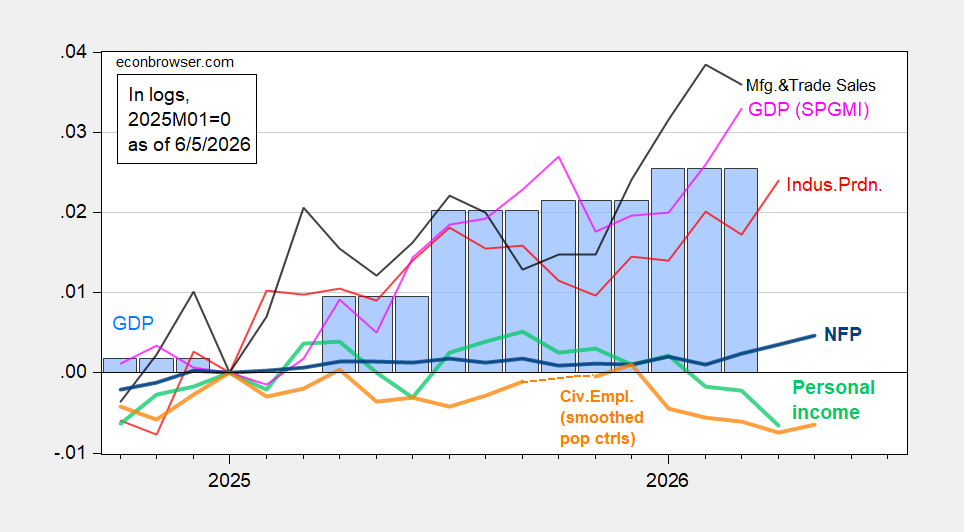

Figure 1: NFP employment (bold blue), civilian employment with smoothed population controls (bold orange), industrial production (red), personal income excluding current transfers in Ch.2017$ (bold light green), manufacturing and trade sales in Ch.2017$ (black), and monthly GDP in Ch.2017$ (pink), GDP (blue bars), all log normalized to 2025M01=0. Source: BLS via FRED, BLS, Federal Reserve, BEA 2026Q1 2nd release, S&P Global Market Insights (nee Macroeconomic Advisers, IHS Markit) (5/7/2026 release), and author’s calculations.

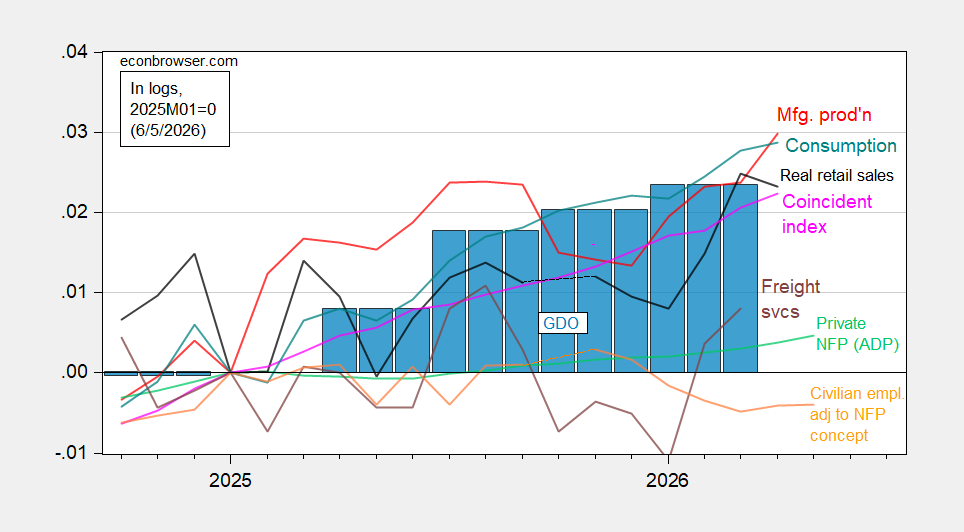

Figure 2: Civilian employment adjusted to NFP concept smoothed population controls (bold orange), manufacturing production (red), ADP private nonfarm payroll employment (light green), real retail sales, CPI deflated (black), freight services indexes (brown), and coincident index in Ch.2017$ (pink), GDO (blue bars), all log normalized to 2025M01=0. Source: BLS, ADP,via FRED, Philadelphia Fed, Bureau of Transportation Statistics, Federal Reserve via FRED, BEA 2026Q1 2nd release, and author’s calculations.

Yesterday, the priced-in odds for steady rates at year end were 47.4%. After the jobs data, now 28.2%

Odds of a 25 basis point rate hike by year end are now priced at 42.7%, at 22.8% for 50 bps.

Tens up 6 bps at 4.54%. S&P down 2.3%. Data still matter, despite the war. Or perhaps because of the war, what with inflation and all.

More big private credit funds have restricted withdrawals this week:

https://www.cnbc.com/2026/06/03/private-credit-jitters-kkr-blackstone-blue-owl-ares-partners-group-pressure.html

Partners Group warns that redemption pressure is spreading to “other asset classes”, which apparently means private equity. And of course redemption pressure is spreading. Whatever the motivation for private credit redemptions – increase cash, reallocate, cut risk – it can be accomplished by cashing in elsewhere if not from private credit.

Part of the problem here is the rising cost of borrowing, since private credit firms borrow in order to lend. Part of the problem may be other side-effects of the Iran war. The U.S. is better shielded from the supply shock than most countries, but high energy costs, lower growth prospects and, perhaps, growing community resistence to the spread of data center are all likely to lower risk-adjusted returns. There’s plenty of safer debt coming on the market as Republicans bloat the deficit every time they legislate.

Because private credit can legally prevent runs by limiting withdrawals, one pathway for the spread of systemic risk is closed off. That is not the only pathway. Private credit shares are falling, as limits on withdrawals are interpreted to be a sign of trouble. Private credit is a major source of investment capital these days, so we could be entering a credit crunch, despite withdrawal limits.