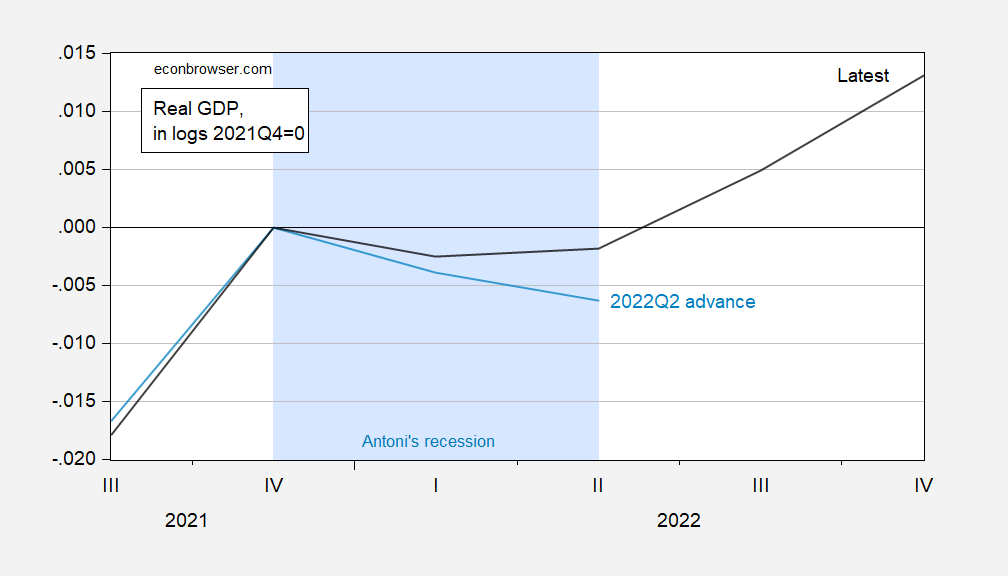

Tons of politically motivated commentary in Canada about the implications of 2 consecutive quarters of negative GDP growth and a “technical recession” [1], even though it’s clear most mainstream economists in Canada fail to read much more into the event. I post a figure from 9 months ago, recapping the the 2024 episode in the US.

Figure 1: Real GDP from 2025Q2 2nd release (black), and 2022Q2 advance release (light blue), both in logs 2021Q4=0. EJ Antoni’s recession shaded light blue. Source: BEA via FRED, ALFRED.

The 2 quarter dip was revised away, as shown in Figure 1. In any case, there was little talk of a recession call in the face of rising strongly rising employment.

Addendum, 6/4/2026:

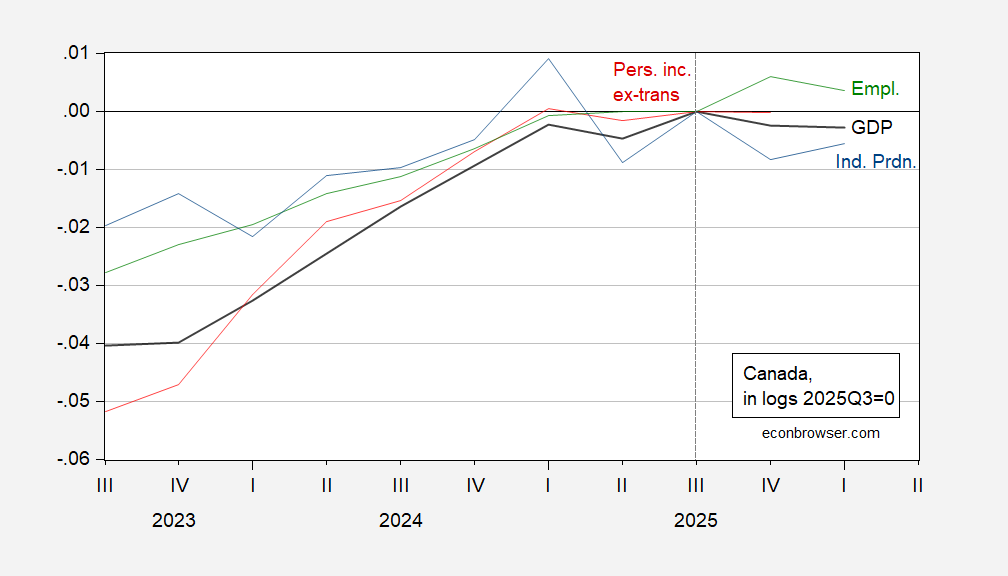

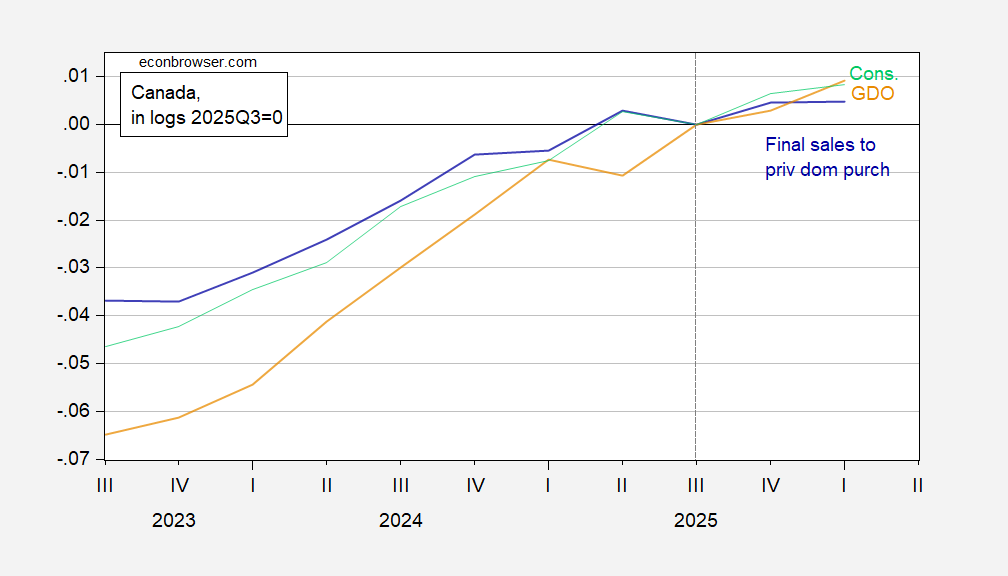

Some additional graphs, of Canadian analogues to variables of relevance to BCDC in the US case:

Figure 2: Canadian GDP (black), industrial production (blue), employment (green), personal income ex-transfers (red), all in logs 2025Q3=0. Personal income seasonally adjusted by author using X-13 2022-2026. Source: StatCan, accessed 6/4/2026..

Figure 4: Canadian GDO calculated as average of GDP and GDP measured on income basis (tan), consumption (light green), final sales to private domestic purchasers (blue), all in logs 2025Q3=0. Source: StatCan, accessed 6/4/2026..

There’s certainly no doubt it’s a mixed picture; with employment rising through Q4, and consumption rising through 2026Q1, it would be hard to (at this point) argue that a recession is underway.

Addendum, 6/5/2026:

CD Howe Institute statement on the GDP release and implications for a recession call.

“Technical recession” is a misnomer at best, often a falsehood. “Technical” in idiomatic English indicates a formal standard which one wishes to dismiss, as in “Technically, the sitting president is a felon, serial bankrupt and rapist, but…” or “Technically, attacking a sovereign country for reasons other than self defense is a breach of international law, but…” “Technically” means something happened by formal definition, not that it happened by some casual rule-of-thumb. When politicians say failure to make interest payments on time is only a “technical default”, they are right, but intentionally misconstrue the meaning of “technical”.

A “technical recession ” is one declared by NBER in the U.S. Arguably there is no such thing as a “technical recession” in Canada, since there are a handful of different recession timers in Canada, C.D. Howe foremost among them, and the government doesn’t get involved.

Technically speaking, two quarters of contraction is not a “technical recession” anywhere that has not adopted a two-quarter contraction as the official definition.

Off topic – Deals are hard for the deal-maker:

https://www.ms.now/news/trump-july-4-freedom-250-america-250-funding-ufc-concert?link_source=ta_bluesky_link&taid=6a2176f3f1fc95000107c1d4

Insiders are saying the war-criminal-in-chief has lost interest in negotiating with Iran; he’d rather work on “his” 250-year U.S. birthday party. Thst doesn’t bode well for reopening the Strait of Hormuz.

Maximalist demands only work when one side is absolutely dominant, and that isn’t the case with Iran. We can see the result of such demands in Russia’s war against Ukraine – years of fighting with little change on the ground. The war criminal has made maximalist demands and is now drifting away from the negotiation. That is not a formula dor reaching agreement.

Meanwhile, Iran has reason to hold out until the next Congress is seated. The House has already passed a war powers resolution to end attacks on Iran. Assuming this Senate balks at doing the same, maybe the next one will. The war criminal will be a lame duck and the public will become angrier about the war as the effects pile up over time.

Kalshi shows progressively lower odds for opening Hormuz before October, now just 46%, and the time value of the “option” certainly doesn’t explain the drop. Sadly, there are no contracts for November or December.

as I said before, Iran has absolutely no incentive to solve this crisis soon. trump takes a far bigger beating than Iran will, politically, the longer this goes on. and the rest of the world suffers far more than the usa does on the energy front, turning allies into angry allies.. the art of the deal will end up with Iran gaining far more than they had prior to the war. they will have tolls on oil through the strait. they will have market access for their oil. they will still have a nuclear program operating secretly, but now even more fortified. and they will have leaders willing to use those nukes after the losses they have suffered.

Inflation worry update – Screwworms are here:

https://www.straitstimes.com/world/united-states/samples-from-texas-calves-tested-for-possible-screwworm-rattling-cattle-markets?ref=inline-article

So far, only one infection has been detected in the U.S., 30 miles north of the border with Mexico. Prior to that, the last report I’d seen put the wormfront about 50 miles south of the border.

Anyhow, surveillance and intervention are likely to pick up dramatically now. Y’all know the implication for beef prices if the worm spreads widely. Heck, we’ve already felt it, due to the ban on imports of Mexican cattle.

Hassett on the next Fox News Sunday: “Another Biden failure.”