NFP underwhelms and prior months revised downward, civilian employment and civilian employment adjusted to NFP concept moving downward.

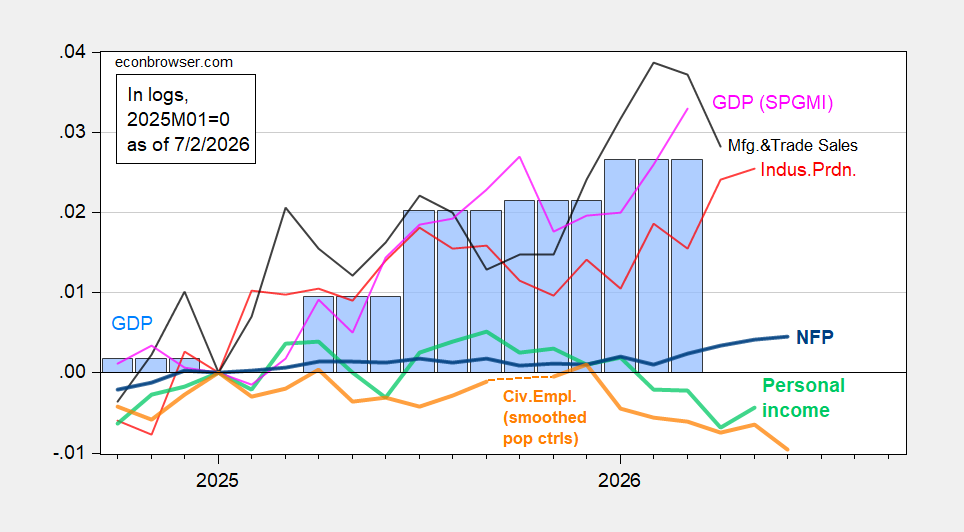

Figure 1: NFP employment (bold blue), civilian employment with smoothed population controls (bold orange), industrial production (red), personal income excluding current transfers in Ch.2017$ (bold light green), manufacturing and trade sales in Ch.2017$ (black), and monthly GDP in Ch.2017$ (pink), GDP (blue bars), all log normalized to 2025M01=0. Source: BLS via FRED, BLS, Federal Reserve, BEA 2026Q1 3rd release, S&P Global Market Insights (nee Macroeconomic Advisers, IHS Markit) (5/7/2026 release), and author’s calculations.

At +57K on nonfarm payrolls, half of consensus (+114K), employment is still growing above breakeven (for constant unemployment rate). Civilian employment is decreasing on trend; while month-to-month changes are noisy for household survey based data, the trend is worrisome.

Note that ADP private NFP was also below consensus, as was BLS private NFP (+59K vs +110K); hence lackluster growth cannot be attributed to government employment cuts.

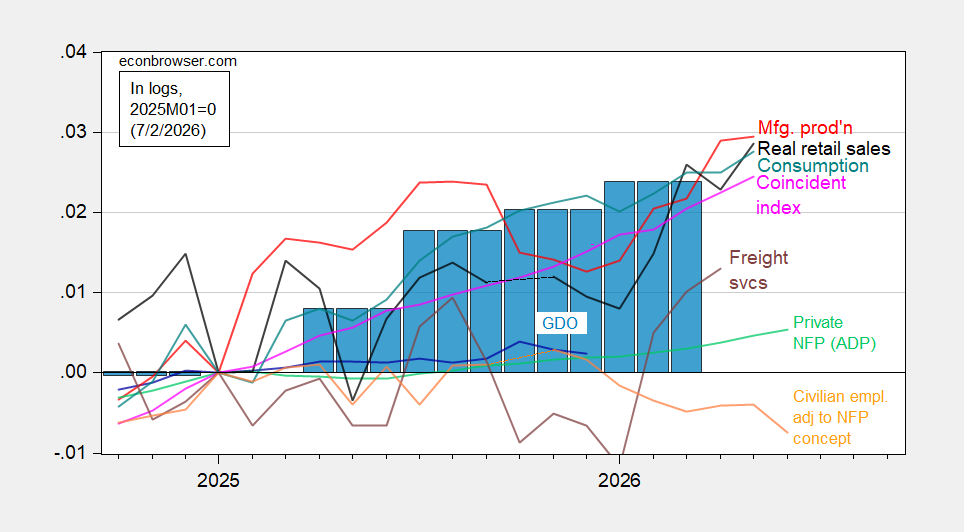

Figure 2: Civilian employment adjusted to NFP concept smoothed population controls, using experimental controls for 2025 (bold orange), manufacturing production (red), ADP private nonfarm payroll employment (light green), real retail sales, CPI deflated (black), freight services indexes (brown), and coincident index in Ch.2017$ (pink), GDO (blue bars), all log normalized to 2025M01=0. Source: BLS, ADP via FRED, Philadelphia Fed, Bureau of Transportation Statistics, Federal Reserve via FRED, BEA 2026Q1 3rd release, and author’s calculations.

One remarkable point is that the coincident index grows more slowly than official GDP or monthly (SP Market Insights) GDP — reflecting the divergence between labor market (which the coincident index relies upon) based indicators and output based.

Today’s employment release highlighted the fact that employment growth is intact insofar as the establishment survey is concerned; further note that the mean absolute revision on month-on-month changes in employment going from 1st to 3rd release is +53K in 2025, so the 2nd release might show an upward revision.

On the other hand, employment — in terms of persons employed — is declining on trend since January.

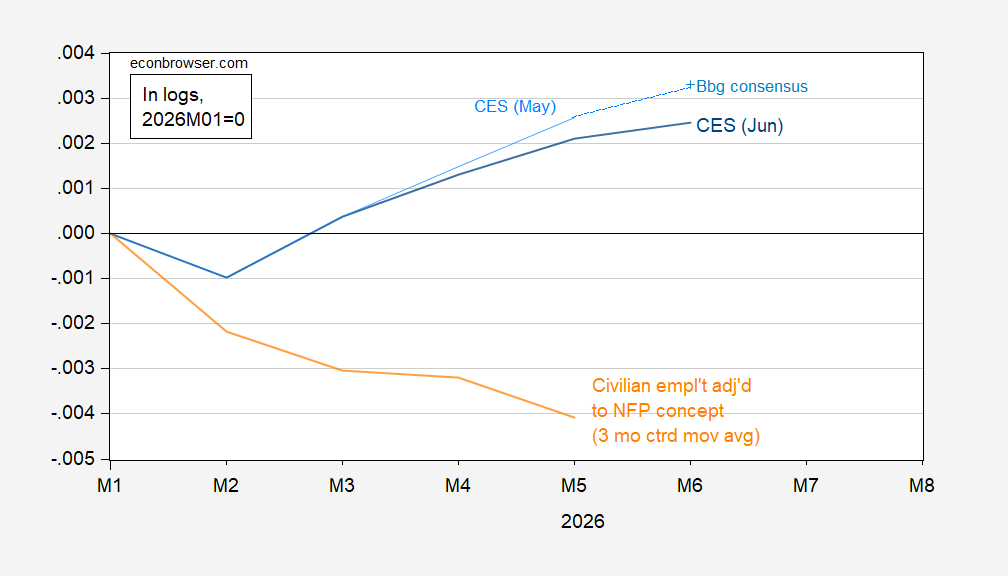

Figure 3: Nonfarm payroll employment, June release (blue), May release (light blue), Bloomberg consensus (light blue +), civilian employment adjusted to nonfarm payroll employment concept, 3 month centered moving average (orange), all in logs 2026M0=0. Source: BLS and author’s calculations.

This was a noticeable downshift in employment growth. The civilian employment series adjusted to NFP concept has been declining since year’s beginning, which is troubling to the extent that these observations are estimated using the same population controls.

The civilian employment and labor force numbers are both down by over a million since April 2025, and the employment-population ratio is at its lowest non-pandemic level in 12 years.

This seems to be a problem, and given that the Trump-Miller Administration seems to be ramping up ICE activity again, I don’t see where that gets better anytime soon. Add in wage growth that is lower than inflation, and what is the engine of growth going forward? Magic productivity gains that only help the owners?