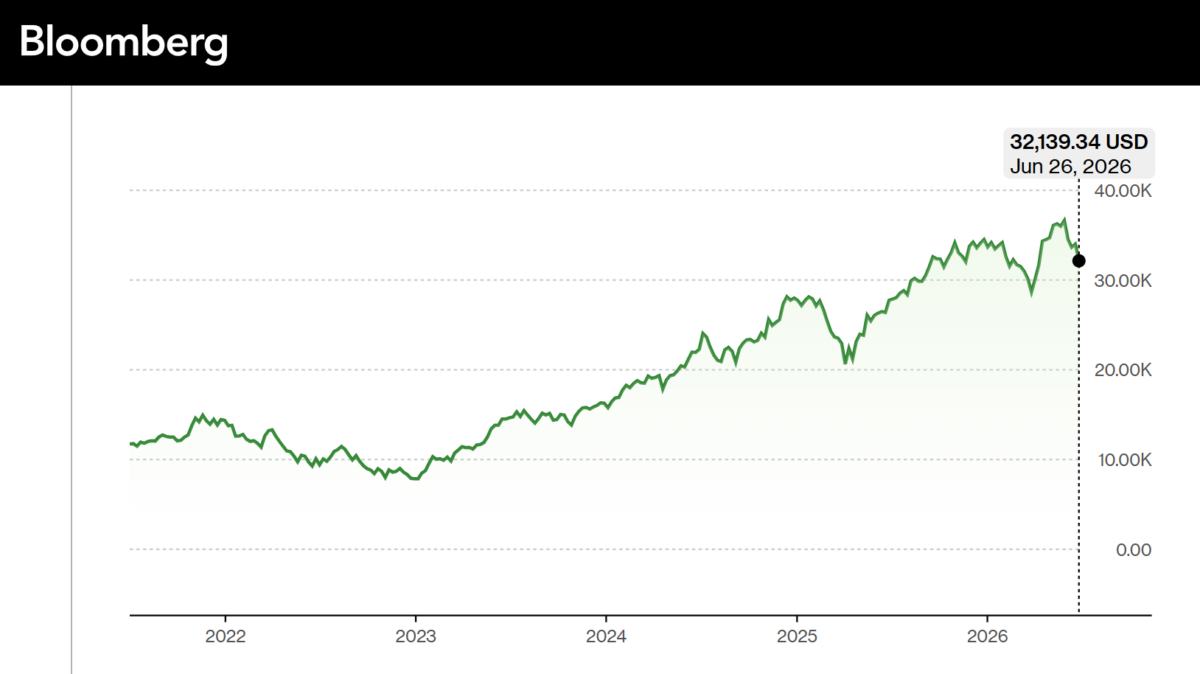

I have no particular expertise in this subject, aside from being around during the dot-com boom (and being a contributor to ERP 2001). Once dot-com related equity prices declined, investment dried up. Bloomberg’s Mag-7 index is now 12.2% below the May 29 peak.

Source: Bloomberg.

The index could recover, say with lower policy rates, or reduced policy uncertainty. Still, suppose a peak has been reached; the stock market peaked at the end of 2000Q1, and by 2000Q4, nonresidential fixed investment peaked.

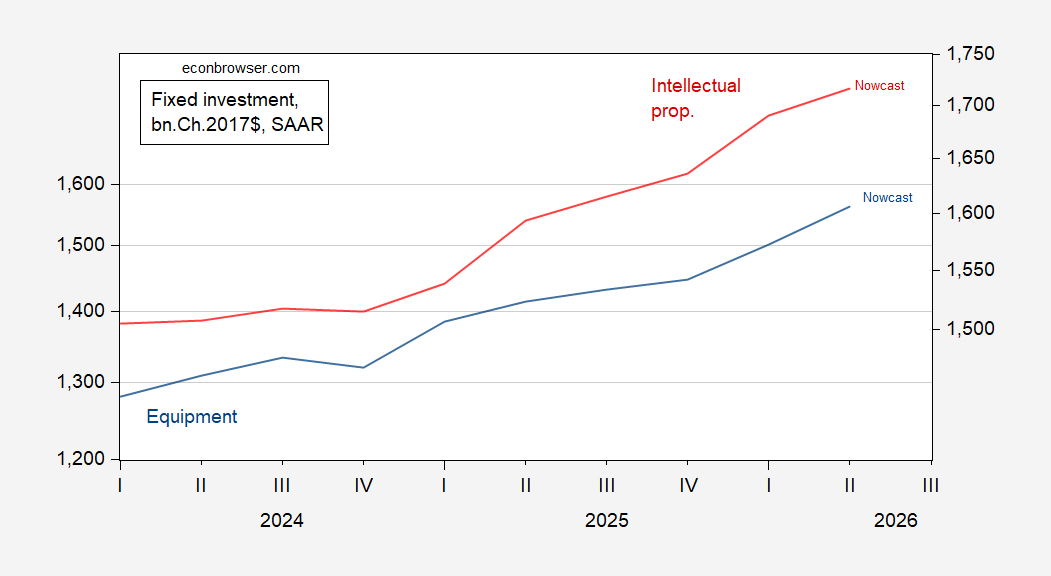

What’s investment look like now? Looking at equipment and software, it looks like the skies the limit.

Figure 1: Nonresident investment in equipment (blue, left log scale), in software (red, right log scale), in bn.Ch.2017$ SAAR. Q2 is GDPNow estimate of 7/2/2026. Source: BEA, Atlatna Fed, annd author’s calculations.

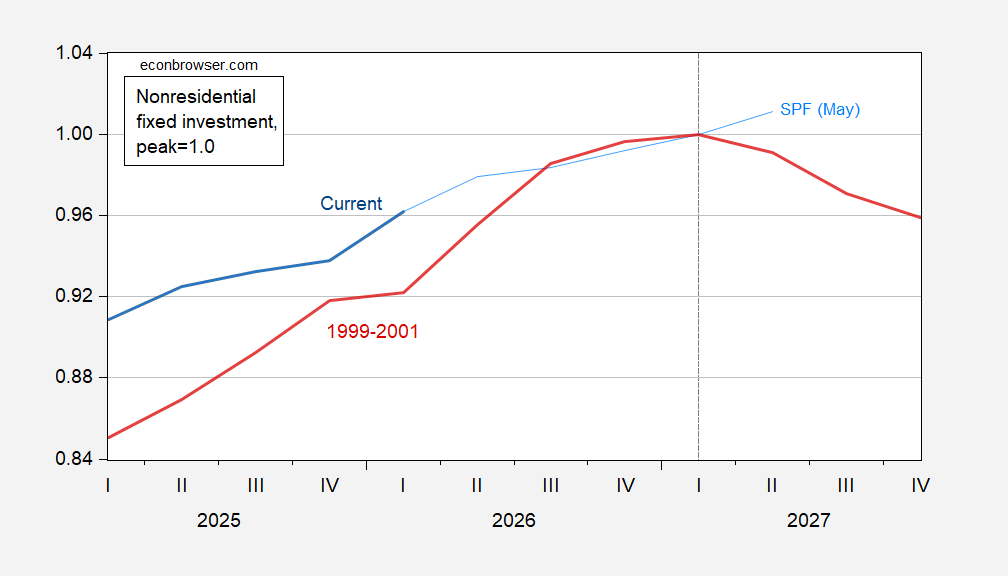

The analogy with 2000 is not apt insofar as most of the Mag-7 firms had sufficient retained earnings to internally fund investment spending, and the big firms are only now tapping debt markets. Suppose there were a three quarter lag between equity peak and investment peak. What would the comparison to 2000 look like?

Figure 2: Nonresidential fixed investment, actual and SPF (blue), lagged 105 quarters (red), both normalized to peak (2027Q1, 2000Q4). 2026Q2 is GDPNow estimate of 7/2. Source: BEA 2026Q1 3rd release, Atlannta Fed, and author’s calculations.

Professional forecasters assume continued investment growth, while a peak in AI-related equity prices (if it is a peak) suggests an imminent downturn.

“If something cannot go on forever, it will stop.”

Herbert Stein

I take it that Menzie has in mind the build-out of AI infrastructure maturing. Makes sense, since that’s what happened with railroads, automobiles, electrification, Y2K and the like. In nearly every case, there has been a large speculative element to the build-out – Y2K was an exception, but worked out pretty much the same. In every case, there was a bust. We don’t know how many data centers we need, just like we didn’t know how many rail lines we’d need. We do know there have been headlines about firms throttling back on use of AI once the bills show up.

There is also a resource constraint issue. If demand for AI data centers runs into supply problems, forecasts build purely on demand will go awry. The current U.S. administration has championed AI. Gregg Abbott has championed AI. Even they are now realizing that AI data centers are putting unsustainable demands on electricity and water resources:

https://gizmodo.com/energy-department-wants-data-centers-to-stop-draining-the-grid-during-brutal-heat-wave-2000780886

https://www.newsweek.com/after-backing-ai-boom-why-greg-abbott-is-turning-against-ai-data-centers-12155521

Heck, Jeff Bezos seems to think that human demand for water is getting in the way of AI expansion. Let’s see who comes out on top!

But maybe I’m being too hard on Bezos:

https://www.snopes.com/fact-check/bezos-water-consumption-ai-quote/

thanks a lot of information greatfull