I was in New York on Friday attending the U.S. Monetary Policy Forum. One of the sessions was on how central banks could better communicate their plans for using unconventional monetary policy. Federal Reserve Bank of Chicago President Charles Evans presented some very interesting ideas.

Author Archives: James_Hamilton

Use of logarithms in economics

Why do economists always want to take the natural logarithm of everything? Here’s the answer,if you don’t mind looking at a few equations and graphs.

Continue reading

Digital transaction security

Bits and bytes can be stolen just like the cash under your mattress.

Who anticipated the Great Depression?

Here’s the abstract from a paper by Doug Irwin in the February issue of the Journal of Money, Credit, and Banking:

The intellectual response to the Great Depression is often portrayed as a battle between the ideas of Friedrich Hayek and John Maynard Keynes. Yet both the Austrian and the Keynesian interpretations of the Depression were incomplete. Austrians could explain how a country might get into a depression (bust following a credit-fueled investment boom) but not how to get out of one (liquidation). Keynesians could explain how a country might get out of a depression (government spending on public works) but not how it got into one (animal spirits). By contrast, the monetary approach of Gustav Cassel has been ignored. As early as 1920, Cassel warned that mismanagement of the gold standard could lead to a severe depression. Cassel not only explained how this could occur, but his explanation anticipates the way that scholars today describe how the Great Depression actually occurred. Unlike Keynes or Hayek, Cassel analyzed both how a country could get into a depression (deflation due to tight monetary policies) and how it could get out of one (monetary expansion).

CBO deficit projections

The U.S. federal deficit fell from around $1.1 trillion for fiscal year 2012 to under $700 billion for 2013, and is projected by the Congressional Budget Office to be below $500 B by 2015. Although it sounds like continuing improvement, the CBO’s projected path is actually unsustainable. Here’s why.

Economics of Bitcoin

Bitcoin is a digital currency for which no government, bank, or corporation takes responsibility. Like many others, I was curious to learn how it works and why it seems to be succeeding.

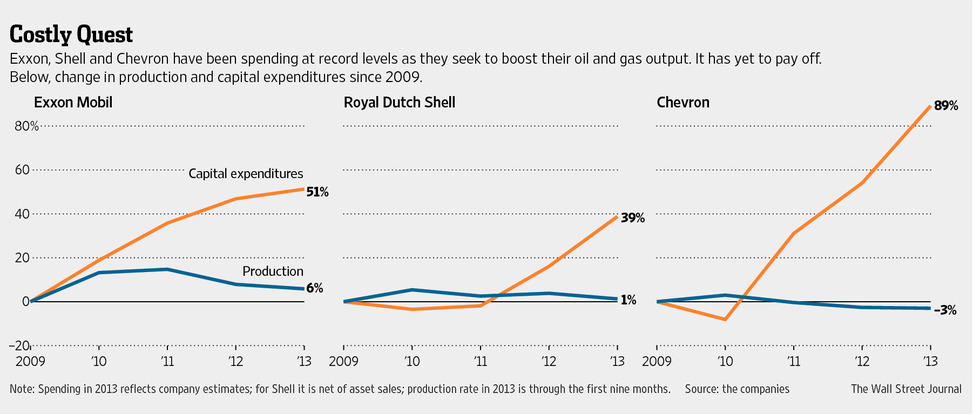

Big oil companies spending more and producing less

From the Wall Street Journal:

U.S. economy gaining momentum

The Bureau of Economic Analysis announced today that U.S. real GDP grew at a 3.2% annual rate in the fourh quarter. That’s two quarters in a row now of above average growth. Given recent experience, that sounds pretty good.

Econbrowser now on WordPress

We have migrated our blog-management system over to WordPress, which will give Econbrowser a slightly different look and help us keep up better with improving technology. For example, by clicking on the appropriate icon that you’ll now find at the end of each post, you can instantly communicate anything you find of interest through other social media such as Facebook and Twitter. Please let us know if you have trouble with any old links, encounter any problems with the new system or have other suggestions.

Thanks to my tech-savvy daughter for helping us to make the switch. You can learn about her company at AdditiveAnalytics.com.

Changes coming for Econbrowser

We will be making some exciting changes to Econbrowser, moving to a new system for managing posts and comments. In preparation for the transition, we have temporarily closed all comments, and at some point during this weekend the complete site may be unavailable. We hope to have a new and better system completely functioning by the end of the weekend, and apologize for the temporary inconvenience.