Rapid and broad based employment growth

First, nonfarm employment has exceeded the previous peak level.

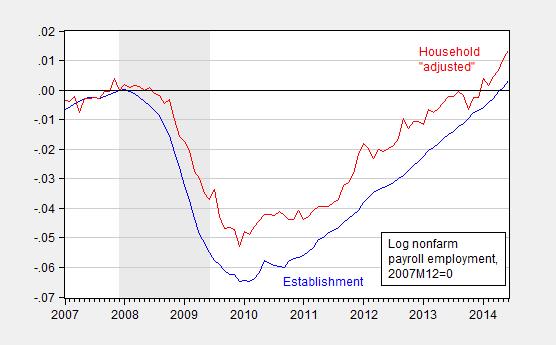

Figure 1: Log nonfarm payroll employment from establishment series (blue), and from household series adjusted to conform to NFP concept (red), 2007M12=0, seasonally adjusted. NBER defined recession dates shaded gray. Source: BEA, NBER, and author’s calculations.

It is of interest to note that the household adjusted series — touted by conservatives during the G.W. Bush era as a better measure of nonfarm payroll employment — first exceeded the previous peak in January 2014, with no apparent mention by those same individuals. By that metric, total nonfarm employment has exceeded its previous peak by nearly one percent.

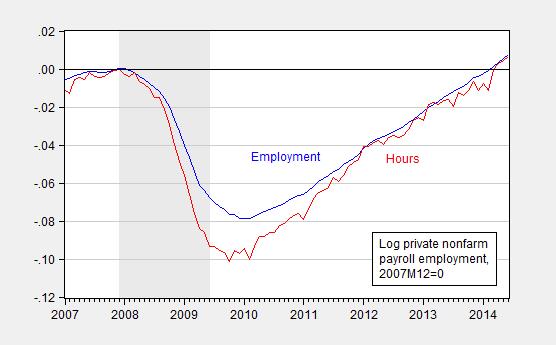

Private employment exceeded its previous peak in April. Employment and hours are now 0.8% above the previous peak.

Figure 2: Log private nonfarm payroll employment from establishment series (blue), and aggregate hours (red), 2007M12=0, seasonally adjusted. NBER defined recession dates shaded gray. Source: BEA, NBER, and author’s calculations.

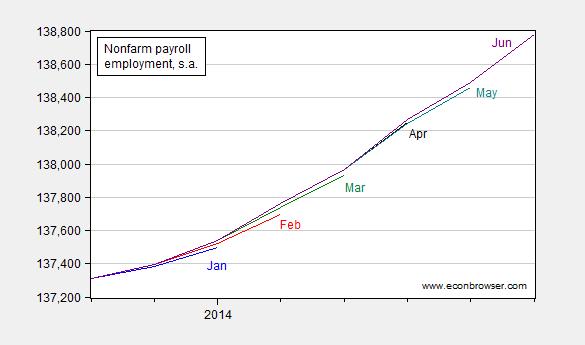

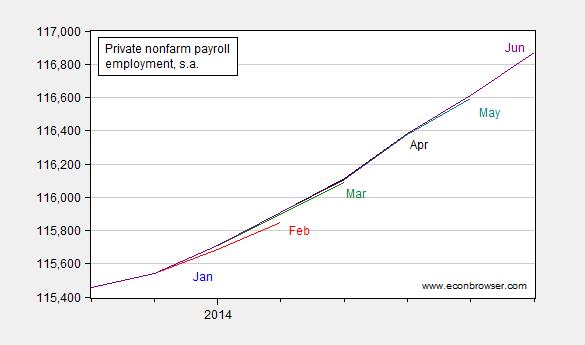

Not only has growth (by either total or private employment) over the past five months matched or exceeded 200K, revisions are typically to the upside.

Figure 3: Nonfarm payroll employment January release (blue), February release (red), March release (green), April release (black), May release (teal), and June release (purple). Source: BLS.

Figure 4: Private nonfarm payroll employment January release (blue), February release (red), March release (green), April release (black), May release (teal), and June release (purple). Source: BLS.

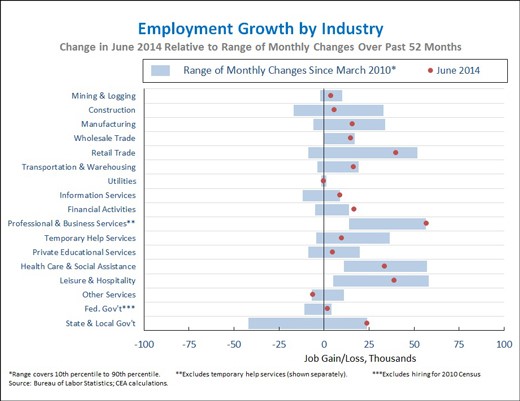

A reassuring point, made by Jason Furman at the CEA, is that the advance in employment is broad based.

Figure 5: Source: Furman/CEA.

None of the foregoing should be viewed as a triumph of macroeconomic policy. For once I agree with Joint Economic Committee Chair Kevin Brady who stated “Today’s strong jobs report comes as a welcome relief to Americans on Main Street. Unfortunately, as good as today’s report is, the rate of job growth still isn’t sufficient to eliminate the private sector jobs gap by the time President Obama leaves office.” And the reason for that, in addition to the hangover from the debt binge of the 2000’s, is the imposition of too-early and unwise fiscal contraction (think sequester, cutting off extended unemployment, failure to extend SNAP, and failure to undertake additional infrastructure investments). Had there been less single-minded obstructionism, fiscal policy would have been much more counter-cyclical in nature, and the employment recovery accelerated.

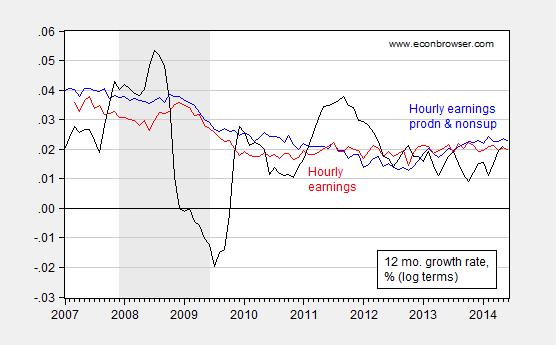

With the acceleration in employment growth, there is ample discussion of tightening labor market and — without too much evidence — rising compensation costs. [1] The latest release does not provide much additional evidence of accelerating wage costs.

Figure 6: 12-month percent change in average hourly earnings for private sector production and nonsupervisory workers (blue), and for all private sector workers (red), and for CPI-all, all calculated as 12 month log differences. NBER defined recession dates shaded gray. Source: BLS via FRED, NBER, and author’s calculations.

For more on the employment release, see CalculatedRisk, Madigan/WSJ RTE, Tim Duy, Applebaum/NYT Upshot, Norris/NYT Upshot, and Stone/CBPP.

“…the imposition of too-early and unwise fiscal contraction (think sequester, cutting off extended unemployment, failure to extend SNAP, and failure to undertake additional infrastructure investments).”

Also, when taxes were raised in 2013, U.S. real GDP growth slowed to 1.8% for 2013, and contracted 2.9% in Q1 2014.

• The expiration of the so-called “Bush tax cuts” enacted in 2001 and 2003 and extended to December 31, 2012 will draw $165 billion out of the economy.

• The renewal of the regular payroll tax, back to 6.2% from the temporary 4.2% extended to December, will draw another $125 billion out of the economy.

• The expiration of the Alternative Minimum Tax (AMT) “patch” designed to protect middle-class taxpayers from this “wealthy-only” tax will now apply to them as well and will extract another $119 billion.

• The expiration of numerous other tax cuts, tax cut extenders, the reimposition of the “death tax” and the elimination of 100% “expensing” for business investment will withdraw an additional $51 billion, and

• The imposition of five of the thirteen new taxes imposed by Obamacare effective January 1, 2013 will be responsible for the balance.

Grand total: $494 billion, or almost four percent of the country’s gross domestic product to be extracted and transferred to the federal government.

Full-time employment fell while part-time work surged.

Now, if only we can somehow persuade 125,000 peak Boomers per month to leave the labor force over the next 2 years, create 2-3 part-time jobs for each of the remaining unemployed and underemployed, we can achieve mass OVEREMPLOYMENT of low-paying part-time workers, augmented by food stamps and Obummercares, and reduce the U rate to 4-4.2% by the next selection of Hillbillary in 2016.

Can it get any better than that?

Yeah, I guess we can finally put the secular stagnation thesis to rest. The slow recovery was just a massive recession combined with PRO-cyclical policy. So, it took longer than normal to come back. It was not the beginning of a “new normal” permanent lack of aggregate demand, It was not v-shaped recovery simply because it was a huge hole that the Ayn Rand cultists refused to fill. Slowly but surely, the USA is coming back to the “old normal”.

XO: “Slowly but surely, the USA is coming back to the ‘old normal’.”

Only if the “old normal” is the 1830s-40s, 1880s-90s, 1930s-40s, and Japan since the 1990s, which, in fact, is what is happening:

https://app.box.com/s/qendym296b81lf9er0z4

https://app.box.com/s/4ccj1how2oy9hw3h9s09

https://app.box.com/s/g1qd63k4cq7vxpu6ojic

https://app.box.com/s/07jsyuk64zc738quwtje

https://app.box.com/s/5dcle1n37nf6jqqjsktr

https://app.box.com/s/uk5zoyu3vws73jn11xne

https://app.box.com/s/5mn3uxfovpbevonufq59

https://app.box.com/s/wgcx7z1rzfjtnu3s3cd9

But don’t allow facts to dissuade you from your beliefs and hope. We Americans are particularly well conditioned to internalize misinformation and develop a personal and collective self-delusion.

Government spending, including defense spending, raises GDP.

I think, we needed bold tax cuts, to pay-down household debt (including high interest rate credit card debt), which would’ve lowered monthly payments to raise discretionary income, strengthen the banking system, and raise private consumption, rather than the small and slow tax cuts, which seemed to put a floor on the economy rather than jolting the economy into a self-sustaining cycle of consumption-employment (where consumption generates employment and employment generates consumption, etc.).

Low prices and low interest rates over the “long boom,” from 1982-07, induced demand resulting in a build-up of household debt. Strong demand was maintained through lower prices and lower interest rates causing diminishing marginal utility (or the opposite of pent-up demand).

The recession was inevitable. However, it could’ve been shallow, or the recovery stronger. Large tax cuts were desperately needed to strengthened household balance sheets and allow the spending to go on.

I am looking at the graphs above. I am referring to a specifc set of facts in those graphs that we all can see. And then you say “don’t allow facts to dissuade you”. Instead of linking outside of these facts that we all can see, why not explain why the rapid change in employment is consistent with secular stagnation.

And, if I wanted to link to a set of outside facts to further critique sec-stag, I could. Most importnat of which is that the population is far more stabile in the USA than the thesis requires. One of its three foundations is negative population growth, and our ratio is better than many assume.

Note at a deeper level, I am simultaneously critiquing Summers and Krugman, and Ayn Rand cultists. For me it is not ideology, but data. And then you scold me to look at the data.

the household survey takes the bloom off that rose, menzie…with the understanding that the margin of error in the count of the unemployed in that volatile survey is at +/- 300,000, a seasonally adjusted 118,204,000 reported they were working full time in June, 523,000 less than in May, while 28,018,000 reported they were working part time, an increase of 799,000 part time workers over May’s count…

rjs: I suggest you read this post which details the paranoic allegations when the reverse occurred in the September 2013 release. Plotting the first difference as in that post (and log first differences) will lead you to a less alarmist perspective. Further, if you try to examine the trends, perhaps by calculating the three month changes, you will be even less alarmed.

i understand that, menzie…my own post on the the household survey includes this caveat: “we’d caution to wait to see if trends shown here don’t reverse in successive surveys”

& im hardly alarmist about employment; my headline on the establishment survey coverage reads “Employers add 288,000 Jobs in June in Best First Half Since 1999 “

rjs: Apologies. I stand corrected.