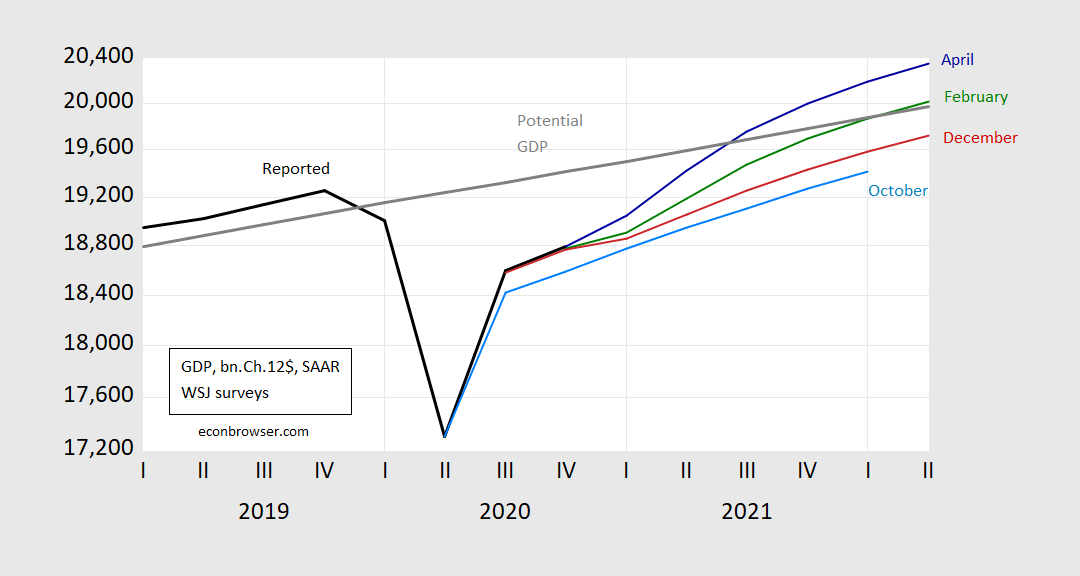

The survey results are out, and once again, the outlook improves.

Figure 1: GDP actual (bold black), WSJ April survey mean (blue), February (red), December (green), October (light blue), CBO estimate of potential GDP (gray), all in billions Ch.2012$, on log scale. Forecasted levels calculated by cumulating growth rates to latest GDP level reported. Source: BEA (2020Q4 3rd release), WSJ surveys (various), CBO (February 2021), and author’s calculations.

The implied output gap by 2022Q2 is 1.9%, compared to 1.3% from last month’s survey (discussed here).

Despite the improvement in the central tendency of forecasts, there remains wide disagreement.

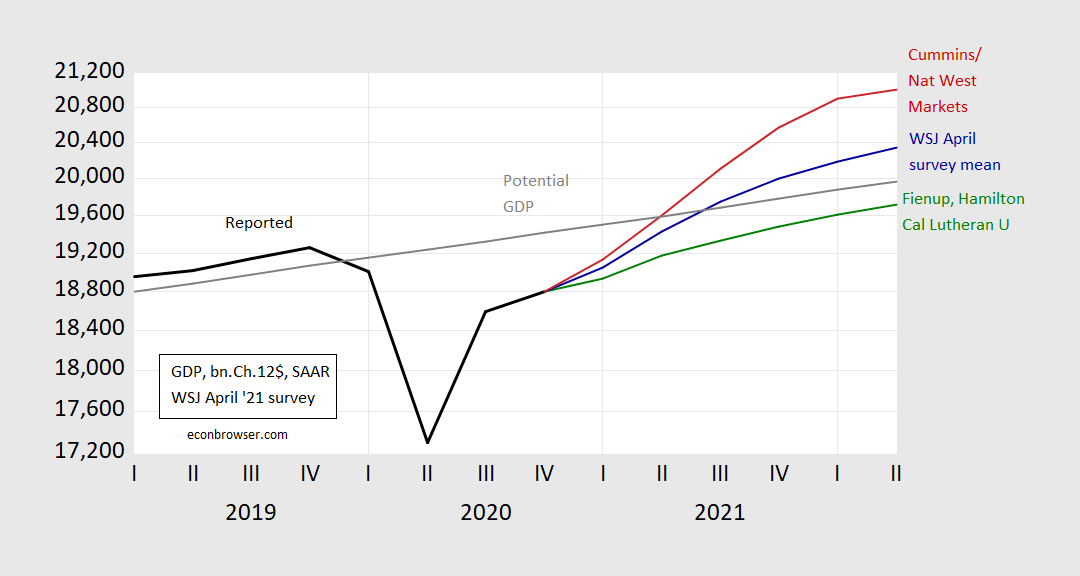

Figure 2: GDP actual (bold black), WSJ April survey mean (blue), Cummins/Nat West Markets (red), Fienup, Hamilton/California Lutheran University (green), CBO estimate of potential GDP (gray), all in billions Ch.2012$, on log scale. Foreacasted levels calculated by cumulating growth rates to latest GDP level reported. Source: BEA (2020Q4 3rd release), WSJ surveys (various), CBO (February 2021), and author’s calculations.

The low forecast implies that an output gap of -1.3% remains by 2022Q2 (the high is 5.1%). In other words, some economists view as plausible the existence of slack in mid-2022 (and it’s possible that even with the high estimates of growth, slack will exist given a high estimate of potential – see this post).

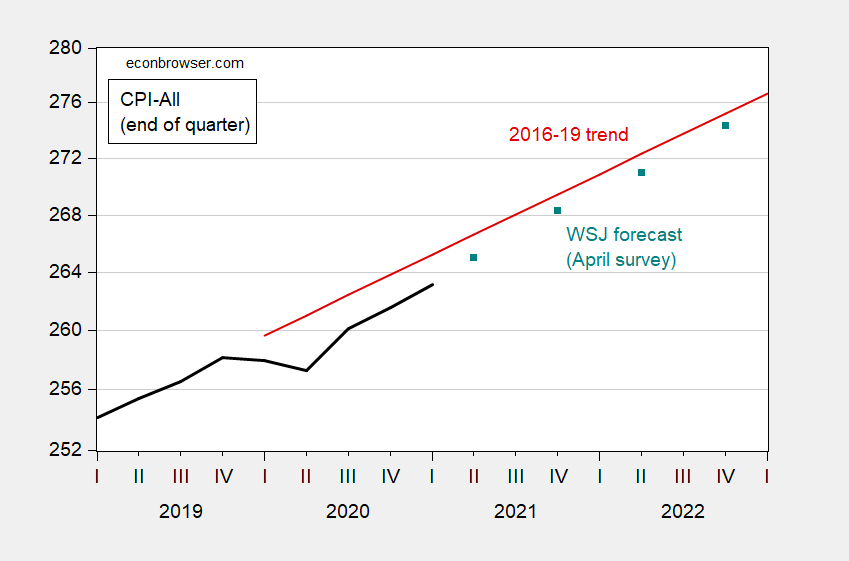

Unsurprisingly, the inflation forecasts have been marked up as well. However, even with 12 month inflation in December 2021 being marked up to 2.58% from 2.48%, the price level will still be below 2016-19 trend.

Figure 3: CPI-all (bold black), CPI implied by WSJ April survey (teal squares), and 2016-19 trend (red), all at end of quarter, on log scale. Source: BLS via FRED, WSJ April survey, and author’s calculations.

So many forecasts, so many estimates of potential output, so little time.

I bet McConnell has two sets of slides:

(1) When discussing where Biden wants to increase spending, pull out the CBO measure of potential output and that latest WSJ forecast;

(2) When arguing for tax cuts for the rich and more defense spending, pull out the less optimistic forecasts but also those higher estimates of potential output.

Interesting update on inflation expectations. I can’t help wonder how this impacts the committee. Will it? What does (will) this say about credibility, of which the literature tells us is ever so important. The committee’s PCE forecast range is 2.1%-2.6% (1.9%-2.5% for core) for 2021Q4 under appropriate monetary policy.

@ EConned

Did you have a personal Dr’s prescription on what the Fed should do at this stage policy wise?? If you’re going to poke fun of the FOMC later, then you better tell us what you would do NOW, in the current context. If you like, you can tell us with Biden’s corporate tax increases or without corporate tax increases. With the stimulus, without the stimulus. Would you have them purchasing low-grade corporate bonds to hold up the bond market (social welfare for bad corporate actors)?? What would you do to rates between now and July 2022??

If you see yourself as above answering these questions “today”, may we assume you relinquish all rights to future hypercriticism of Fed actions??~~~or just assume that you enjoy criticizing Fed moves under any Democrat WH administration??

Optimally, I’d like to see them target NGDP.

Realistically, I’d like to see them reassess IOER, if not the above then do price level targeting instead of average inflation targeting, and possibly increase asset purchases – let’s get expectations of inflation (both market and their own) higher. And hopefully that helps to push inflation itself higher. Isn’t that the goal?

On a side note, what on earth is your comment about? The tone is very distasteful.

1) “I better…”?

2) Assume I “relinquish all rights to future hypercriticism of Fed actions”?

3) Assume that I “ enjoy criticizing Fed moves under any Democrat WH administration”?

Seriously? I actually didn’t criticize (much less “hypercriticize”) the Fed – I only reiterated that (as Menzie showed) market expectations and their own projections under proper monetary policy won’t likely get them to their stated objective. You seem hypersensitive to my comment for no good reason. Relax. Enjoy a drink (or whatever is your thing) and engage in fruitful and meaningful discussion of economics. I’ll look forward to your contributing. Cheers!

I’m glad you found the courage to put your thoughts related to Federal Reserve policy on record. It is interesting that most folks on the political right don’t like asset purchases by the Fed under a Democrat President and most people on the right are always saying they fear inflation.

Don’t you think it’s kind of dumb in the current context for the Fed to purchase assets, when it appears inflation for the next 18 months will largely take care of itself?? Wouldn’t it be nice/smart to “organically” move away from the ZLB, and for once let a problem “take care of itself” (or at least be solved more through fiscal policy rather than monetary policy) ??

No

I’m not sure what’s courage about my comments and I’m not sure what relevance your anecdote regarding what people on the right like under a democrat POTUS. The former is very much strange and the latter is very much irrelevant.

I have no idea what “it appears inflation for the next 18 months will largely take care of itself” even means. The FOMC’s projections have suggested that inflation will revert to their policy desires for a number of years now – are you one of those who over the past decade has suggested the “next 18 months” the committee will get it right? Yes, 18 more months should do the trick *eyeroll*.

I fear what you mean by ““organically” move away from the ZLB, and for once let a problem “take care of itself””. But it sounds like your being “hypercritical” of the Fed. Maybe you’re thinking we should “purge the rottenness from the system” à la Mellon? I can’t see how your suggestions will assist inflation expectations – it seems they’ll do the exact opposite.

And I’m in the camp of a firm “no” wrt attempting to solve inflationary concerns “through fiscal policy rather than monetary policy”. You lost me before but now I’m jumping on a different train heading in the opposite direction. Nope. Count me out.

it seems that monetary policy has been ineffective at pushing up inflation over the past decade. it has been effective at keeping us from descending into deflation, however. so if we are in agreement, econned, that we need a higher inflation rate, it would appear the next available tool is fiscal policy? i don’t think the fed can pull this off alone.

baffling –

I will not sign my name to the following assertion: “ i don’t think the fed can pull this off alone.”

baffling –

While it’s technically true to say that in the US “it seems that monetary policy has been ineffective at pushing up inflation over the past decade”, we must acknowledge that it seems (via revealed preferences) the committee wasn’t as concerned with pushing inflation to their stated 2% target as their statements would suggest. As such, it could easily be argued that the committee might very well be to blame for being “ineffective at pushing up inflation over the past decade”.

“As such, it could easily be argued that the committee might very well be to blame for being “ineffective at pushing up inflation over the past decade”.”

econned, perhaps you could offer up some solutions if you disagree? you mentioned additional asset purchases. we have already done that at large scale, and it supported our efforts against deflation but did not really provide inflation. the fed kept interest rates at basically zero for years, and it did not induce much inflation. other nations tried negative rates, and still no inflation. exactly what can the fed do to scale that will push up inflation, given what has already occurred and its results? if you want to provoke inflation, you are going to have to get fiscal policy involved. empirically, it appears we have some inflation today, and recent stimulus (ie fiscal policy) seems to be a major driver. not fed policy directly. indirectly the fed is helping by not raising rates. but it appears something outside of monetary policy is required to kick start the inflation cycle. unfortunately, we have a lot of folks out there still arguing the fed should be raising rates…not sure how that will help the inflation situation.

baffling – the experience of 2016-2019 suggests the committee was not committed to its 2% goal. I don’t know how it can be viewed otherwise. Maybe this damaged their credibility.

https://fred.stlouisfed.org/graph/fredgraph.png?g=D6Uj

“baffling – the experience of 2016-2019 suggests the committee was not committed to its 2% goal. I don’t know how it can be viewed otherwise. Maybe this damaged their credibility.”

econned, that is not an accurate statement. as soon as the fed realized expenditures quit rising, the fed also stopped raising rates. and they dropped rates when they found expenditures falling. at the time, 2% was the goal, not over 2%. that was a mistake. they did pretty good in real time, where they had a lag in the pce numbers you show. hindsight is 20/20.

you may also note that the fed was also following the policy that trump said they should follow until 2019. this was the policy he campaigned on. so if you want to lay blame on the fed, even more applies to trump economic policy. i was not in the camp of raising interest rates at the time. that is what trump campaigned on, however. as for damaged credibility, it probably reinforces the idea the fed should be shielded from political influence. this means “eminent” partisan hacks should not be on the fed board, in my view.

baffling –

We will have to disagree. It’s clear that the committee increased IOER some 6 times despite core PCE never hitting 2%. Hell, the first hike was during a time core PCE was below 1.5% and two consecutive hikes in 2017 occurred as core PCE was falling and never within a full quarter percentage point of the target. I seem to recall nearly every FOMC statement saying something along the lines of the transitory nature of low inflation and that the committee expects inflation will stabilize around 2% over the medium term and for years this was the case. Go read the June 2017 statement – they raise the target Fed funds rate despite acknowledging “inflation has declined recently” and “running somewhat below 2 percent” and “market-based measures of inflation compensation remain low”. Core PCE during the 2 months prior to the meeting was 1.6% and dropped the two months following the rate hike all the way to 1.45% in August. Moreover, you’re not accurate in asserting that

“at the time, 2% was the goal, not over 2%”

as Chair Yellen was very clear in various statements that 2% was a goal (as you state) but that 2% was NOT a ceiling (counter-your assertion). Anyways, I’m certainly not shining light on an area others (e.g. Scott Sumner) haven’t discussed before I have… but the light seems to be shining quite clearly if one simply opens their eyes.

Also, I couldn’t care less about Trump’s suggestion(s) of monetary policy now or during his presidency and I put faith that the committee was (for the most part) indifferent as well. As to “”eminent” partisan hacks” not being on the Fed board, I agree but this seems irrelevant to the Fed hiking IOER despite not hitting 2% core PCE unless your assertion there were “eminent partisan hacks” on the committee during those years.

” It’s clear that the committee increased IOER some 6 times despite core PCE never hitting 2%. ”

econned, that is not the same thing as “committee was not committed to its 2% goal.”, as you assert.

the committee was not raising rates to keep inflation from reaching 2%. i believe the fed was happy with 2% inflation, they simply pursued the wrong policy to keep it there. that is different from not being committed.

If you look at the data and/or you (re)read my comment you’ll realize that your following comment is in error:

“the fed was happy with 2% inflation, they simply pursued the wrong policy to keep it there. that is different from not being committed.”

It is in error because core PCE was not at 2% and was declining further below 2% just prior to (and following) the June hike. As such, the committee’s actions suggest that they were not truly committed to hitting their 2% target. Why? Because the increased IOER not only before ever hitting 2% but also as core PCE declined further from the 2% target.

Here’s Minnesota Neel from the minutes:

“Mr. Kashkari dissented because he preferred to maintain the existing target range for the federal funds rate at this meeting. In his view, recent data, while suggesting that the labor market had improved further, had increased doubts about achievement of the Committee’s 2 percent longer-run inflation objective and thus had not provided a compelling basis on which to firm monetary policy at this meeting. He preferred to await additional evidence that the recent decline in inflation was temporary and that inflation was moving toward the Committee’s sym- metric 2 percent inflation objective. He was concerned that raising the federal funds rate target range too soon increased the likelihood that inflation expectations would decline and that inflation would continue to run below 2 percent.”

And more from in the minutes from following hike in December 2017:

“In Mr. Evans’s view, with inflation continuing to run substantially below 2 percent and measures of inflation expectations lower than he believed to be consistent with a symmetric 2 percent inflation objective, it was im- portant to pause in the process of policy normalization. Leaving the target range at 1 to 11⁄4 percent for a time would better support an increase in inflation expecta- tions, increase the likelihood that inflation will rise to 2 percent and perhaps modestly beyond, and thus pro- vide more support for the symmetry of the Committee’s inflation objective. Such a pause also would better allow the Committee time to assess the degree to which earlier soft readings on inflation were transitory or more persis- tent.

In Mr. Kashkari’s view, while employment growth re- mained strong, wage growth had not picked up and in- flation remained notably below the Committee’s 2 per- cent target. In addition, the yield curve had flattened as long-term rates had not moved higher even though the Committee raised the federal funds rate target range. He was concerned that the flattening yield curve was partly due to falling longer-term inflation expectations or a lower neutral real rate of interest. He preferred to wait for inflation to move closer to 2 percent on a sustained basis or for inflation expectations to move up before fur- ther raising the target range for the federal funds rate.”

The forecast range is of less importance than the median estimate and central tendencies. The median estmates for the core PCE deflator was up 0.1% from January estimates for both 2022 and 2023. That is good news from the Committee’s perspective, but not much of an acceleration. If inflation does pick up, that is in keeping with the Fed’s stated goal, and should improve credibility wheree the Fed most wants credibility – in its ability to control inflation in both directions.

In March, the FOMC’s own funds rate projections were unchanged at 0.1% through 2023. If your question includes the Fed’s likely policy behavior in the face of a modest pick-up in inflation, the FOMC’s own projections are a good place to start.

The range is important because it tells us how far apart some committee members might be. And could suggest where the central tendency might shift in the future. In any case, the central tendencies don’t differ much from the range.

My question is how will the market forecasts present by Menzie impact the committee (although it could be suggested that markets forecasts largely follow committee forecasts). The committee’s recent projections differ from what Menzie has presented. And I seem to recall research suggesting PCE is roughly 0.4 percentage points lower than CPI. E.g. Menzie states “However, even with 12 month inflation in December 2021 being marked up to 2.58% from 2.48%, the price level will still be below 2016-19 trend”. And, as I noted, the committee’s projections for Dec 2021are 2.2% and 2.4% for headline and core PCE respectively. Also, policy certainly doesn’t stop at the Fed funds rate.

Policy doesn’t stop at the funds rate, but as long as the median estimate of the funds rate is at effective zero, odds are reasonably good the Fed will be adding to the portfolio. The recent history of the Fed ending asset purchases is instructive. In the post-GFC episode, the Fed repeatedly resumed asset purchases, realizing they were mistaken in deciding to end them with rates at the floor.

When the Fed’s goal is to induce inflation rather than to stimulate growth, the lessons of the prior cycle may not apply, but I’m not aware of a body of research arguing that asset purchases are the wrong tool to stimulate inflation, nor have I heard Fed officials making that argument. Some have argued against asset purchases for other reasons, but not because they are the wrong tool to boost inflation.

I realize Fed officials discourage the use of members’ own estimates as forecasts, but those estimates are the only objective means by which we poor mortals can glean thoughts on timing from the Fed. They seem to expect another 2+ years of near-zero rates. That suggests to me continued asset purchases for most of that period.

If you have increased fiscal spending it might make those asset purchases less necessitative. If they pass the package Biden is asking for, I think a decent argument for “normalcy”, letting the rate climb on its own, can be made. I’m not ready to get into internet fisticuffs about it, but I think a decent argument for tapering is there. Again this assumes a decent sized fiscal package.

macroduck – I agree with much of your comment so I think maybe we were speaking past one another. Also, my reference to the committee’s projections was explicitly about PCE.

“If you have increased fiscal spending it might make those asset purchases less necessitative. ”

agreed. this is why i said the fed cannot go it alone. they fed is necessary, but not sufficient, to boost inflation. i have yet to see the fed have the ability, in the current environment, to accomplish this task alone. despite what some others on this board have implied.

I should have produced this chart earlier. After all, I often make my breakfast listening to Morning Joe take down Trump from a conservative perspective. The host loves to whine that Trump spends like a drunken sailor. Colorful but is it true? Here is real government purchases over time:

https://fred.stlouisfed.org/series/GCEC1

Yea there is a large increase from 2014 to mid 2020 but notice the huge drop off during the 2010 to 2014 period. I would call this Tea Party fiscal policy with the 2014 to 2020 increase simply reversing this period of fiscal austerity.

Odder still is the fact that as the economy slumped from the pandemic, real government purchases fell. Herbert Hoover fiscal policy.

Yes Biden wants to increase government purchases on things like infrastructure. Can we afford it? Sure we can. Do we need it? Absolutely. How to pay for it? Raises taxes on the ultra rich. This seems to be an easy case to make.

Sometimes the obvious hides in plain sight.

What strikes me is that the prospect of higher tax rates doesn’t seem to be having much of an effect on projections. In a year or two, we may find out that higher tax rates didn’t cause economic catastrophe. We might have to look to the Eisenhower administration to see how badly the tax rate caused the economy to slump, and how little got done then. Like the interstate highway system. That couldn’t have been initiated during a high tax era, could it?

Thanks for reminding us of the Eisenhower interstate highway system. If reminds me of one of those patented Princeton Steve series of long winded rants where he starts off by declaring we should only finance infrastructure with user fees followed by noting that the construction of this interstate highway system was not financed by user fees. What was his point you ask? Princeton Steve has no clue. Of course he never does.

You are correct, I think, that the tax rate makes very little difference. Instead of putting the focus on that transfer mechanism (which is completely incidental) the focus should be: where does money go a. if Mr. and/or Mrs. one-percent hold it and b. if the government holds it. The investment and spending targets are different and in the end that is the only substantive difference. Those differences are what will produce differing end results.

“You are correct, I think, that the tax rate makes very little difference.”

they make a difference, but at rates far far higher than where we are today. we are not close to the tax rates that would be a negative for the economy, today.

Kevin Drum has been tracking the number of vaccines given in the US each day using this source:

https://ourworldindata.org/covid-vaccinations

The graphs that first come up show by nation total vaccines per capita by nation as well as the rate of increase. The US situation looks pretty good in total and the pace of new vaccines is also one of the higher ones per capita.

I got my 2nd dose of the Pfizer vaccine last Thursday. Still wearing the mask and socially distancing but will get a very needed haircut in 10 days. Please get vaccinated if you have not already.

Unfortunately, most of the Western Hemisphere is a mess when it comes to mass vaccinations; which means that about the same time we become optimally vaccinated, a new generation of coronaviruses, likely quite resistant, should be arriving from let’s say Lima or Belem by the winter.

Unless we chose to act very soon. which is, bluntly, a fantasy. We’re not built for that.

Looking so forward to my annual if not semi-annual booster shots, and hoping that my aging immune system holds up…

i will get my second jab of pfizer next week. but keeping the mask and social distancing well into the summer. we can beat this, if we commit to winning.

I get Pfizer jab two on Friday. I expect to keep wearing a mask in pubic until the fall, more or less. It doesn’t stop me from doing anything except eat at restaurants and drink at bars. I don’t do those things more than a few times a year anyway. Boring people like me are bad for the economy.

https://jabberwocking.com/as-always-inflation-is-lurking/

Kevin Drum reads the WSJ so we do not have to:

Ronald Reagan was in the White House, “Return of the Jedi” was in theaters, and economic growth hit an astonishing 7.9%. The U.S. has produced many more Star Wars films since 1983, but growth has never approached that level—until this year, if economists are right. Those surveyed by The Wall Street Journal boosted their average forecast for 2021 economic growth to 6.4% … That boom might have a potentially troubling side effect. Inflation, as measured by the consumer-price index, is expected to jump sharply from 1.7% in February when March data is released Tuesday.

Kevin replies to the inflation fear mongering:

thanks to unusually low inflation at the start of the pandemic last year, the headline inflation rate for the next few months is going to be unusually high. This is not because inflation is actually high. It’s just a mechanical result of the arithmetic. It’s as if you were comparing your electricity usage to a year ago when you were on vacation for a week. It would look like your usage was up 25%, but it’s not. It’s just a mechanical result of the previous year being artificially low.

Kevin is not an economist but this is a really good point. Princeton Steve is not an economist either but he clearly does not understand what Kevin said here.

If 2% inflation is an increase of 3% over 1% deflation, it’s still a 3% increase in the inflation rate. Something like that. Were we facing deflation during the pandemic?

I’m not afraid of inflation, even though I lived through the 1970s and 1980s. I’m just a little confused.

Someone leaked this Biden-Harris presentation to the OECD expressing how the US thinks of something called Pillar 1 and Pillar 2:

https://mnetax.com/wp-content/uploads/2021/04/US-slides-for-Inclusive-Framework-meeting-of-4-8-21-2.pdf

It gets deep in the weeds of the international tax proposals. Biden-Harris is a bit hard on Pillar 1 as they are on those stupid ideas in Trump’s TCJA. In my view, we should scrap all of this confusing mess.

But Pillar 2 has an idea that dates back 60 years to the brilliant work of Peggy Musgrave who proposed a global minimum tax. That sort of became US tax law for a while but we mucked this up and treated it like the Brady gun registration bill aka poke it with more holes than Swiss cheese. If we can get major nations like China to join us imposing a global minimum tax, the race to the bottom with massive profit shifting to tax havens would come to an end. Now this would make a lot of overpriced international tax attorney and accountants unemployed, which would be a wonderful thing.

“If we can get major nations like China to join us imposing a global minimum tax, the race to the bottom with massive profit shifting to tax havens would come to an end.”

i am not sure that china is the bad guy in that respect. they tax their people pretty heavily overall, either personally or on the business front. china is not really tax friendly. what you need to address are the small countries who simply operate as tax havens. not sure if they have much incentive to change.

My suggestion is actually something Dr. Lorraine Eden has noted. Which is basically if the largest nations do this – it will not matter too much what smaller nations end up doing. I guess one has to listen to one of her seminars to appreciate where she is coming from.

The Irish seem to be culprits more than the Chinese when it comes to tax dodges.

that is my thought as well. china benefits from lower wages. but china still wants its cut of taxes. ireland simply played the discount broker game. if enough business transactions flowed through their system, a small tax could add up to a large amount. and since the nation itself was not growing, that was enough to cover many of the costs of its people. ireland would have had a problem if all those businesses had actually relocated there, and funds were needed to grow the infrastructure. they were not collecting enough tax to cover those types of growth costs. but ireland was taking away tax revenue from other parts of the world that was growing. that was an uneven playing field, and an issue that globalization will need to address.

https://jabberwocking.com/hey-nbc-grocery-prices-are-not-soaring/

Kevin Drum reminds me why MSNBC needs to ditch Stephanie Ruhle:

So there I am, channel surfing in the living room, when Lester Holt tells me that the cost of groceries is “soaring.” He throws to Stephanie Ruhle, who reports that there’s “sticker shock” in the grocery aisle and then interviews a guy who says his grocery bill has doubled. That’s followed immediately by a graphic showing that the price of eggs and hamburger has gone up 7%.

HYPERINFLATION! Seriously – this is Princeton Steve level stupidity. Ruhle has this annoying theme “let’s get smarter” which is followed by her babbling nonsense with equally stupid Ali Velshi. Ruhle’s claim to fame is that she worked for Deutsche Bank handing out loans to Donald Trump. Now I get watching cable news generally makes one dumber in terms of economics but damn – even Faux News is not that stupid.

I used to be a pretty big Lester Holt fan. You know how occasionally I like to boast that I am very perceptive about people??~~ but occasionally I get fooled. Examples: Elizabeth Warren (who I liked very much back in 2008-2009 time frame), Tulsi Gabbard, others I can’t think of at the moment, I might list more later if I think of them (like anyone cares). Lester Holt is one of the ones who completely fooled my self-proclaimed highly perceptive capabilities:

https://www.yahoo.com/news/nbc-host-duped-north-korea-reporting-staged-ski-resort-100310902.html

Not getting the Walter Cronkite award for excellence in journalism. Judy Woodruff and Brent Goff get my time if I am watching TV, not Lester the suit-wearing clown. For the record, I don’t watch Brian Williams either, but Brian NEVER had me fooled, and I am eternally mystified how MSNBS still employs the proven pathological liar.

The Gaetz party girls may want to say they are not prostitutes but you bet they got paid for the sex and there were lots of drugs provided. Now Gaetz declares he never paid for this. Of course not – some rich donor paid for the drugs and the girls in exchange for political favors from Gaetz.

https://www.cnn.com/2021/04/14/politics/gaetz-parties-women-drug-use-sex-payments/index.html

The OECD has a neat cross national comparison of government support for R&D in terms of direct funding and tax support:

https://www.oecd.org/sti/rd-tax-stats.htm#countries