Today we are fortunate to be able to present a guest contribution written by Georgios Georgiadis (European Central Bank), Helena Le Mezo (European Central Bank) , Arnaud Mehl (European Central Bank), and Cédric Tille (Graduate Institute for International and Development Studies, Geneva). The views expressed in this column are those of the authors and do not necessarily reflect those of the ECB or the Eurosystem. They should not be reported as such.

The dollar occupies a dominant role in international good and financial markets that goes well in excess of the economic weight of the United States. A central question in international economics is how solid that role is. While the creation of the euro has not displaced the dollar, the economic rise of China could represent a larger challenge to the greenback, especially as Chinese policy makers are keen to promote the international role of the renminbi, in contrast to the more hands-off approach of the Europeans.

Are such policies effective? In a recent paper (Georgiadis et al., 2021) we focus on the invoicing of international trade and contrast the impact of economic fundamentals and policy measures. Invoicing is a relevant dimension of the international role of currencies, as the position of the dollar is dominant but not exclusive, and the role of the renminbi, while still small, is increasing. Specifically, the dollar is used in 40% of international trade flows, while only 10% of trade involves the U.S. as the source or destination country (Goldberg and Tille, 2008; Gopinath, 2015; Boz et al., 2020). This indicates a substantial use of the dollar as a vehicle invoicing currency (Gopinath et al., 2020).

A broad look at the impact of economic fundamentals

A large literature has looked at the economic determinants of invoicing. A salient dimension is the presence of strategic complementarities, which lead exporters to limit the fluctuations of the price of their goods relative to that of their competitors (e.g. Mukhin, 2021). In a context of sticky prices, exchange rate movements play a large role in driving relative prices and exporters have an incentive to invoice in the same currency as their competitors. As domestic firms represent a sizable share of the competition faced by exporters, we would expect trade flows to the U.S. and the euro area to be more likely to be invoiced in dollars and euros, respectively. Also, the need to limit relative price movements is more relevant in sectors where goods are more homogeneous.

The rise in global value chains (GVC) can also play a role, as firms that are part of such a chain sell goods that include a sizable share of imported inputs, with a correspondingly lower share of domestic value added. This provides an incentive to invoice exports in the same currency used for imports in order to provide a natural hedge of costs.

We empirically assess the role of economic fundamentals using a broad sample with information on invoicing currencies building on Boz et al. (2020). The data cover 115 countries after 1999 and indicate the shares of the dollar, euro, domestic currency, and others in the countries’ exports and imports. The data for this broad sample do not systematically contain information on the renminbi, however.

A panel analysis confirms the role of fundamentals. Exporters to the U.S. or the euro area make more use of the dollar and euro, respectively. A similar pattern is observed for exports to countries that are pegged to the dollar or the euro. Trade in goods that are more homogeneous makes more use of the dollar, at the expense of the euro. The participation in GVC has no significant impact, except that it promotes use of the euro in the invoicing of exports, but only among euro area countries.

The rising role of the renminbi

While the euro has long been seen as the only potential challenger to the dollar, the rising economic weight of China has opened the possibility that the renminbi could become another challenger. We assess this using a smaller sample of countries (not including China itself) for which we have information on the use of the renminbi in addition to the dollar and the euro.

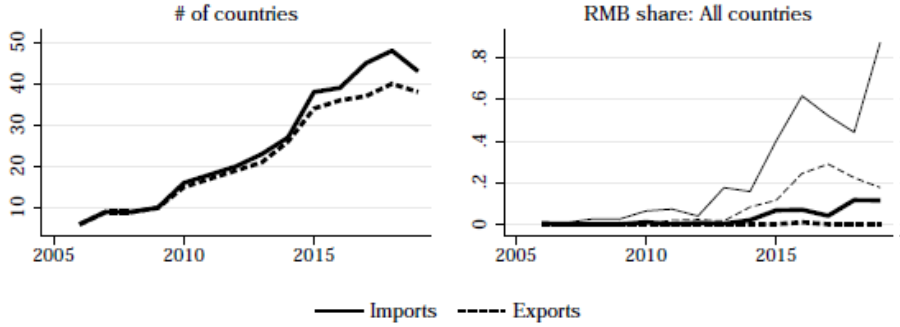

The use of the renminbi remains quite limited, but it is growing. The left panel of figure 1 shows the number of countries for which data on renminbi invoicing are available. The right panel depicts the share of trade invoiced in renminbi in countries that use it to some extent, including the median (thick lines) and 75th percentile (thin lines). We clearly see that the Chinese currency is not yet a sizable competitor to the other currencies, being used only in a small share of trade. Nonetheless, there are outliers with a larger share of renminbi invoicing, and the trend is clearly positive.

Figure 1: Evolution of renminbi invoicing

Source: Georgiadis et al. (2021). Notes: The left panel sows the number of countries with data on renminbi invoicing. The right panel shows the share of exports and imports invoiced in renminbi, with the median (thick lines) and the 75th percentile (thin lines).

Our analysis indicates that the rising role of the renminbi in part reflects the same economic fundamentals considered for the euro and the dollar, albeit in a very heterogeneous way. Overall, higher trade with China is associated with more dollar use at the expense of the euro. Focusing on specific regions shows a differentiated pattern. Among European countries, a higher share of imports from China leads to more euro use at the expense of the dollar. By contrast, countries in South-East Asia and Oceania make more use of the dollar, at the expense of the euro, when they trade more with China. Fundamentals, however, have little impact on the use of the renminbi, except for trade of Oceania countries with China .

Active policy

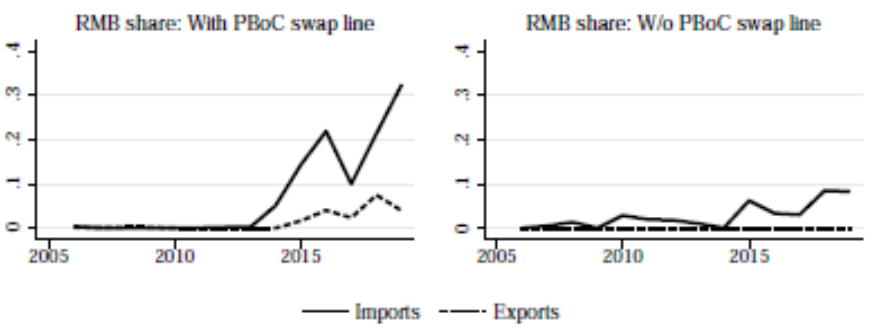

While European officials argued until recently that the international role of the euro is essentially driven by market forces, Chinese counterparts have taken a more active role. Specifically, the People’s Bank of China (PBoC) has established currency swap lines with central banks in other countries to facilitate payment in renminbi and promotes its use in international trade. Bahaj and Reis (2020) show that policies that reduce financial transaction costs through the establishment of swap lines can in theory lead to a higher use of the corresponding currency in international trade invoicing.

We indeed document that swaps lines have been associated with greater use of the renminbi in international trade invoicing. Figure 2 shows the share of renminbi in the invoicing of exports and imports, contrasting the countries that have set up a swap line with the PBoC at some point (left panel) with those that have nott (right panel). We clearly observe a higher renminbi use in the former group.

Figure 2: Renminbi invoicing and currency swap lines

Source: Georgiadis et al. (2021). Notes: The figure shows the median share of renminbi invoicing in countries that have established a swap line with the PBoC (left panel) and the ones that did not (right panel).

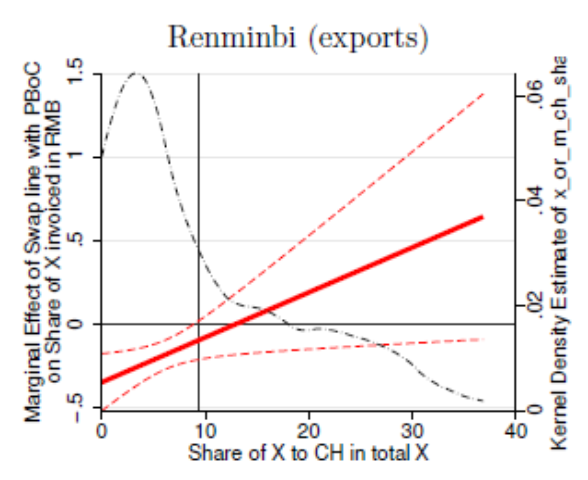

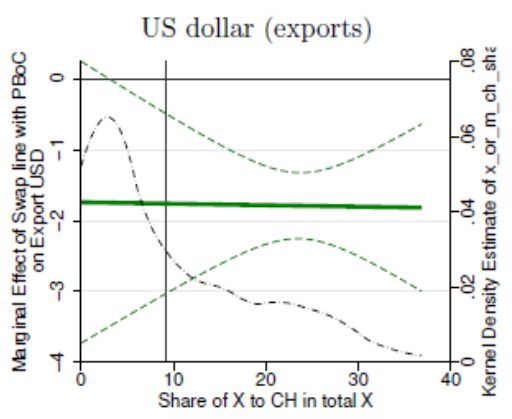

Looking more closely at the data, we find that the swap lines are associated with more use in the renminbi only in countries for which China is a sizable trading partner. Figure 3 shows the effect of having a swap line on renminbi invoicing depending on the share of exports that go to China (the pattern is similar for imports). While setting up a swap line with a country that does not trade much with China lowers the use of renminbi slightly, the effect becomes less negative and turns positive for countries where a higher share of exports are destined for China.

Figure 3: Impact of swap line on renmibi invoicing

Source: Georgiadis et al. (2021). Notes: The figure shows the marginal effect of a PBoC swap line on renminbi invoicing depending on the share of a country’s exports going to China. The solid line indicates the point estimate and the dashed line the 90% confidence interval. The blue dashed line is the kernel density estimate of the distribution of the share of exports going to China.

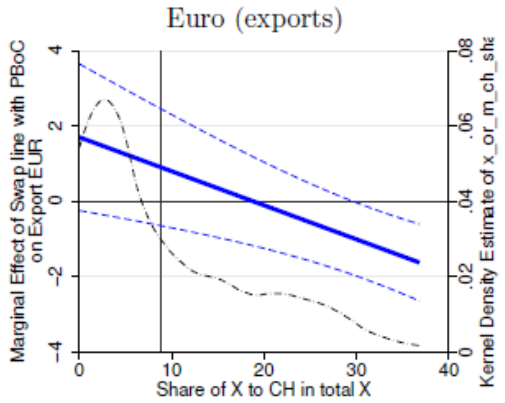

In which competitor currency’s share is the additional use of the renminbi mirrored? Figure 4 shows the impact on dollar (left panel) and euro (right panel) invoicing constructed along the same lines as figure 3. The higher renminbi use comes at the expense of the dollar, for which the effect is negative regardless of the extent to which a country trades with China. Invoicing euro is also reduced, but only in countries that trade a lot with China. In addition, the magnitude of the effect on the euro remains much smaller than the impact on the dollar.

Figure 4: Impact of swap line on dollar and euro invoicing

Source: Georgiadis et al. (2021). Notes: The figure shows the marginal effect of a PBoC swap line on dollar invoicing (left panel) and euro invoicing (right panel) depending on the share of a country’s exports going to China. The solid line indicates the point estimate and the dashed line the 90% confidence interval. The blue dashed line is the kernel density estimate of the distribution of the share of exports going to China.

The rising invoicing role of the renminbi reflects economic fundamentals, albeit only on a regional basis, and the PBoC policy of establishing swap lines to promote the use of its currency. Our analysis reveals that the specific currency whose use is reduced depends on the invoicing driver considered. Economic fundamentals show that China’s integration in world trade has benefited the dollar and the renminbi (to some extent) at the expense of the euro, and therefore reinforced the dominance of the dollar. In sharp contrast, the establishment of swap lines has raised the use of the renminbi at the expense of the dollar, with a much more moderate impact on the euro.

Our analysis thus shows that a rising role of a new challenger currency does not necessarily come at the expense of existing challengers but can come at the expense of the dominant currency. The exact pattern depends on which specific factors are behind the rising role of the new currency.

References

Bahaj, S., and Reis, R. 2020. Jumpstarting an International Currency. CEPR Discussion Paper 14793

Boz, E., Casas, C., Georgiadis, G., Gopinath, G., Le Mezo, H., Mehl, A., Nguyen, T., 2020. Invoicing Currency Patterns in Global Trade. Vox, 9 October.

Georgios G., Le Mezo, H., Mehl, A., Tille, C., 2021. Fundamentals vs. Policies: Can the US Dollar’s Dominance in Global Trade Be Dented? CEPR Discussion Paper 16303. [ungated version, GIIDS working paper]

Gopinath, G., 2015. The International Price System. NBER Working Paper 21646.

Gopinath, G., Boz, E., Casas, C., Diez, F.J., Gourinchas, P.O., Plagborg-Møller, M., 2020. Dominant currency paradigm. American Economic Review 110, 677-719.

Goldberg, L., Tille, C., 2008. Vehicle-currency Use in International Trade. Journal of International Economics 76, 177-192.

Mukhin, D., 2021. An Equilibrium Model of the International Price System. Mimeo.

This post written by Georgios Georgiadis, Helena Le Mezo , Arnaud Mehl, and Cédric Tille.

Economic fundamentals show that China’s integration in world trade has benefited the dollar and the renminbi (to some extent) at the expense of the euro, and therefore reinforced the dominance of the dollar. In sharp contrast, the establishment of swap lines has raised the use of the renminbi at the expense of the dollar, with a much more moderate impact on the euro….

[ Really nice paper. ]

“GVC” hitting auto sales in China. That seems to be a dramatic drop. They told/sold it differently in the China Daily headlines:

https://www.reuters.com/article/china-autos/china-vehicle-sales-fall-18-in-august-industry-body-idUSKBN2G60FX

http://www.chinadaily.com.cn/a/202109/10/WS613b1855a310efa1bd66eb51.html

If you look at the line graph of the sales from roughly September of 2020 to the latest August data, it looks like Barkley Junior’s version of a “V recovery”

I stopped reading the intellectual garbage from the National Review a long time ago but this line really is beyond absurd:

‘Beyond the serious legal and process issues raised by using a rarely invoked OSHA emergency authority to deputize private businesses to prod 80 million Americans into getting vaccinated, there are serious practical questions.’

But the National Review would be elated if we deputized businesses and total strangers to spy on a women’s choice with respect to her own body.

There is SO much intellectual garbage here:

https://www.nationalreview.com/corner/the-practical-problems-with-bidens-employer-vaccine-mandate/

I guess I should blame Kevin Drum for making me read this nonsense but his rebuttal is quite good:

https://jabberwocking.com/bidens-vaccination-rules-are-more-message-than-mandate/

https://fred.stlouisfed.org/graph/?g=CcnS

January 15, 2018

Real Broad Effective Exchange Rate for United Kingdom, Euro Area, United States, Japan and China, 1994-2021

(Indexed to 1994)

https://fred.stlouisfed.org/graph/?g=CcnY

January 15, 2018

Real Broad Effective Exchange Rate for United Kingdom, Euro Area, United States, Japan and China, 2007-2021

(Indexed to 2007)

https://fred.stlouisfed.org/graph/?g=lwgj

January 30, 2018

Total Reserves excluding Gold for China, 2007-2021

https://fred.stlouisfed.org/graph/?g=F7qB

January 30, 2018

Total Reserves excluding Gold for China, 2017-2021

[ Also, the Chinese sovereign wealth fund was worth $1.2 trillion by the close of 2020. ]

The reason for invoicing exports in a reserve currency is obvious. The domestic reserve authority will happily exchange domestic for reserve currencies. The RMB, at only 2.45% of global reserves, is not a currency most reserve authorities want.

China’s use of swap facilities lowers the cost of invoicing in renminbi, when it could instead lower the cost for domestic firms of doing business in other currencies. China is taking the place of reserve authorities, creating renminbi liquidity, so that invoicing will be in renminbi. It could as easily use swap lines to facilitate invoicing in trading partners’ currencies. So why do it this way?

As a practical matter, China is behaving differently than Eurozone authorities because the euro accounts for about 21.2% of global reserves, not 2.5%. China’s swap lines make up for the fact that pretty much nobody really wants renminbi reserves.

But this isn’t a practical matter — it’s political. China already has lots of influence through economic ties. Invoicing in renminbi, in addition to being a big ego thing, is a way to extend political influence. It’s a way of saying “China, China, China” to exporters in other countries, the way ltr says “China, China, China” in comments here.

Yes ltr’s cheerleading for China, China, China is obnoxious but she is not as bad as the World Gold Council. I would hope Menzie does a post taking out their latest stupid ad:

https://www.bing.com/videos/search?q=world+gold+council+ad&docid=608042501667360048&mid=8A016506F025FCC5E62C8A016506F025FCC5E62C&view=detail&FORM=VIRE

Gold is “liquid and agile”? Like no other asset is? Gold provides you with a “strategic advantage”? WTF is that advantage. Oh wait – the lady in the commercial is cute so if she is a gold digger, the creep doing this announcement thinks he has a chance with it? The only people who would be impressed by this stupid ad are already fans of Tucker Carlson anyway.

You want Menzie to do a blog post on a commercial made by an industry association whose near sole function is to promote thee sale of gold?? Personally I think Menzie’s time is more valuable than that and spending his time like that isn’t why he got his post-graduate education. Maybe YOU should do that post. Seems very suitable to your skill set.

Looks very reasonable and probably what is going on, a gradual increase in reliance in international trade on rmb, while it is still very low in such usage. There remain some serious obstacles to it getting anywhere near the use of the euro, much less the USD, for such purposes, such as continuing capital controls. But probably these will gradually dissipate over time. It will continue to get more important, but it is a long way from becoming the world’s leading currency for such purposes.

Two key take-aways:

“Chinese policy makers are keen to promote the international role of the renminbi…”

— The ones who fall into this camp are the technocrats, not the political leaders. When it comes to releasing significant control over monetary policy, these technocrats will be asked “How does it work? What’s the upside, and what’s the downside?” They will most certainly not be asked to decide the issue.

Invoicing … really? Aren’t the overwhelming majority of currency transactions purely financial, with no goods or services anywhere to be seen? Aside from China’s desire to more closely tie her neighbors to the Chinese economy, the currency of choice in an actual trade transaction is moot.

Aren’t the overwhelming majority of currency transactions purely financial, with no goods or services anywhere to be seen?

[ Ministers of countries subject to United States economic sanctions have claimed that trade becomes limited or even made impossible in a range of currencies. Why might this be so? ]

It isn’t rocket science; it’s political science…

The job description of trade ministers generally does not include forex transactions, but it might include currency manipulation.

Remember, the issue is not “will foreign trade ministers complain about China’s exchange rate,” but rather “will the Rmb become a core international currency on par with the euro or yen.”

This is an issue for central bankers, not trade ministers.

Remember, the issue is not “will foreign trade ministers complain about China’s exchange rate,” but rather “will the Rmb become a core international currency on par with the euro or yen.”

[ Thank you so much, but I was referring to US economic sanctions against a range of countries such as Cuba. Cuban ministers claim that the US sanctions virtually preclude trade. The same claim is made by ministers of other US sanctioned countries. As for China, the point is for China to be able to trade with say a Cuba no matter the US sanctions. This is a serious matter that needs to be addressed.

Thank you for the kind response. ]

@ ltr

Why don’t you tell the Propaganda Minister of China (your father-in-law I assume??) that you gain more respect in the international community by achieving things, not by going on the television with Kleenex held up to your eyes. Japan can do it with a smaller population base than China. Why don’t you try this way?? This is real achievement, not hiding Covid-19 death counts and purging science data.

https://www.bloomberg.com/news/articles/2021-08-30/first-autonomous-cargo-ship-faces-test-with-236-mile-voyage

https://news.cgtn.com/news/2021-09-11/Chinese-mainland-reports-25-new-confirmed-COVID-19-cases-13sGjnnefEQ/index.html

September 11, 2021

Chinese mainland reports 25 new COVID-19 cases

The Chinese mainland recorded 25 new confirmed COVID-19 cases on Friday including 1 locally transmitted in Fujian Province, the latest data from the National Health Commission showed on Saturday.

In addition, 21 new asymptomatic cases were recorded, while 371 asymptomatic patients remain under medical observation.

This brings the number of confirmed COVID-19 cases on the Chinese mainland to 95,153, with the death toll unchanged at 4,636.

Chinese mainland new locally transmitted cases

https://news.cgtn.com/news/2021-09-06/Chinese-mainland-reports-18-new-confirmed-COVID-19-cases-13kp2fMfFE4/img/5e6ae4d463a249cc81cd4870308eaeaf/5e6ae4d463a249cc81cd4870308eaeaf.jpeg

Chinese mainland new imported cases

https://news.cgtn.com/news/2021-09-11/Chinese-mainland-reports-25-new-confirmed-COVID-19-cases-13sGjnnefEQ/img/f8657fdd14f44cefb40a31079502a15e/f8657fdd14f44cefb40a31079502a15e.jpeg

Chinese mainland new asymptomatic cases

https://news.cgtn.com/news/2021-09-11/Chinese-mainland-reports-25-new-confirmed-COVID-19-cases-13sGjnnefEQ/img/d91bfe9738de4184b8a4edb35f598cb0/d91bfe9738de4184b8a4edb35f598cb0.jpeg

http://www.news.cn/english/2021-09/11/c_1310181856.htm

September 11, 2021

Over 2.13 bln doses of COVID-19 vaccines administered in China

BEIJING — More than 2.13 billion doses of COVID-19 vaccines had been administered in China as of Friday, data from the National Health Commission showed Saturday.

[ Chinese coronavirus vaccine yearly production capacity is more than 5 billion doses. Along with over 2.135 billion doses of Chinese vaccines administered domestically, another billion doses have been distributed to 100 countries internationally. A number of countries are now producing Chinese vaccines from delivered raw materials. ]

https://www.worldometers.info/coronavirus/

September 11, 2021

Coronavirus

United Kingdom

Cases ( 7,197,662)

Deaths ( 134,144)

Deaths per million ( 1,964)

China

Cases ( 95,128)

Deaths ( 4,636)

Deaths per million ( 3)

ltr: Could I ask you to limit your recounting of covid-19 statistics to threads that actually have to do with covid-19, please?

While the creation of the euro has not displaced the dollar, the economic rise of China could represent a larger challenge to the greenback, especially as Chinese policy makers are keen to promote the international role of the renminbi, in contrast to the more hands-off approach of the Europeans.

[ The paper is excellent, but there is no reason suggested for Chinese policy makers seemingly being “keen to promote the international role of the renminbi.” I would suggest being keen might reflect the use of the dollar or sanctions to limit the trade of a range of countries. United States economic sanctions, say, against Cuba, even during an international epidemic, have presented trade problems that another country my want to avoid. Using the dollar for sanctions, as the US has been increasingly doing might be considered a problem for a trading country.

The paper is excellent, but what dollar sanctions represent might have been considered. ]

While the creation of the euro has not displaced the dollar, the economic rise of China could represent a larger challenge to the greenback, especially as Chinese policy makers are keen to promote the international role of the renminbi, in contrast to the more hands-off approach of the Europeans.

[ Also, I know that in Chinese policy circles the effects on Japanese growth of the 1985 Plaza Accords that dramatically increased the value of the Yen are remembered, and the Asian currency crises of the later 1990s are remembered. Countries most effected by the Asian currency crises, such as Indonesia or Thailand, did not recover the growth momentum they had before the currency value swings. China will be protective of currency value. ]

Georgia is running over UAB and Alabama is trouncing Mercer. Why were these games even scheduled? Like they could not find a decent high school team to play? Now Oregon v. Ohio State was a good game.

“Now Oregon v. Ohio State was a good game.”

no. it was not a good game.

I guess it wasn’t if you are an Ohio State fan. But cheer up as Ohio State was not as bad as FSU.

They gave up over 30 points two weeks in a row. It was a bad game(s).

Maybe they’ve just been using the wrong coombs on their hair.

Scoring points, and the quarterback has a million dollar contract. Seems to me they need better pay for the defense to perform equally well. This nil issue is gonna get expensive. I see a college salary cap when union negotiations begin.

Bad defensive coaching has no relation to NIL. And the sins of the NCAA administration have nothing to do with NIL. The NCAA doesn’t like NIL because it gives players a slice of the pie that the NCAA administrative staff has been stealing from the players (mostly African American athletes) for decades. That’s like a thief (the NCAA) saying your wallet (NIL) is creating problems for society. The thief shouldn’t be making the rules.

Chinese policy makers are keen to promote the international role of the renminbi…

[ The issue is not a manner of national vanity. China was after all banned in 2011 from participation in supposedly international space exploration programs with NASA. So, China has been independently building space exploration programs. Chinese policy makers need to be intent on protecting the Yuan against direct or indirect use of economic sanctions by the United States.

Then too, the Yuan needs to be protected against the sort of purposeful international speculator who undermined the Pound in 1992 and who has been “threatening” China these past days:

https://www.wsj.com/articles/blackrock-larry-fink-china-hkex-sse-authoritarianism-xi-jinping-term-limits-human-rights-ant-didi-global-national-security-11630938728 . ]

i wonder if independent nations such as taiwan will continue to accept the foreign renminbi as currency going forward. if i were taiwan, i would tell china that no invoices in renminbi are accepted, as taiwan does not accept that foreign currency as legal tender.

Taiwan uses its New Taiwan dollar which I think is worth 3 cents. Hong Kong’s currency is also called dollar with a HK$ worth about 12 cents.

Taiwan is also the formal headquarters of multinationals with very significant Chinese manufacturing operations. It might make sense for the two nations to have the same currency but I bet Taiwan would prefer China adopts its currency.

If you were Taiwan, bffling, you would realize very quickly that your (Taiwan’s) economy is far, far more dependent on China than China is dependent on you.

Do you think that had anything to do with China stealing ICBM technology from other nations?? Possibly?? If China quit stealing other nations’ technology all the time they might be happy to work with you.

Well, the 9/11 ceremonies were not about donald trump, so why attend??

https://www.nytimes.com/2021/09/11/us/where-was-trump-9-11-anniversary.html

Why don’t you tell the Propaganda Minister of —– (your father-in-law I assume??)

[ This person has repeatedly sought to intimidate me. I have never addressed this person and never will, but I think the horrid attempts at intimidation should stop. ]

In 2011 after Congress stopped NASA from working on space exploration with China, the Chinese went on independently to develop and launch an advanced international satellite network including a global positioning system, a Mars exploration program, a Moon exploration and surface mineral retrieval program, an “international” space station, ground and ocean based space observatories-including the most powerful radio telescope ever built. There is much more here, and of course this is the work of China.

Then china should stop interfering with independent nations such as taiwan.