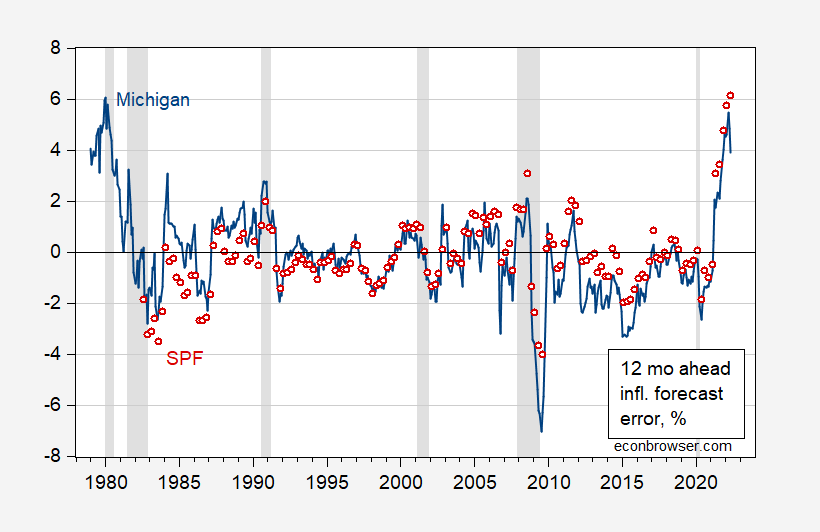

From the Michigan consumer survey and the Survey of Professional Forecasters:

Figure 1: Michigan 12 month ahead forecast error (blue), and Survey of Professional Forecasters median forecast error (red), in percentage points. NBER defined peak-to-trough recession dates shaded gray. Source: BLS via FRED, University of Michigan via FRED and Philadelphia Fed, NBER, and author’s calculations.

Since these are 12 month ahead forecasts sampled at a higher frequency than the horizon — monthly (for MIchigan) or quarterly (for SPF) — these errors are based on overlapping forecasts.

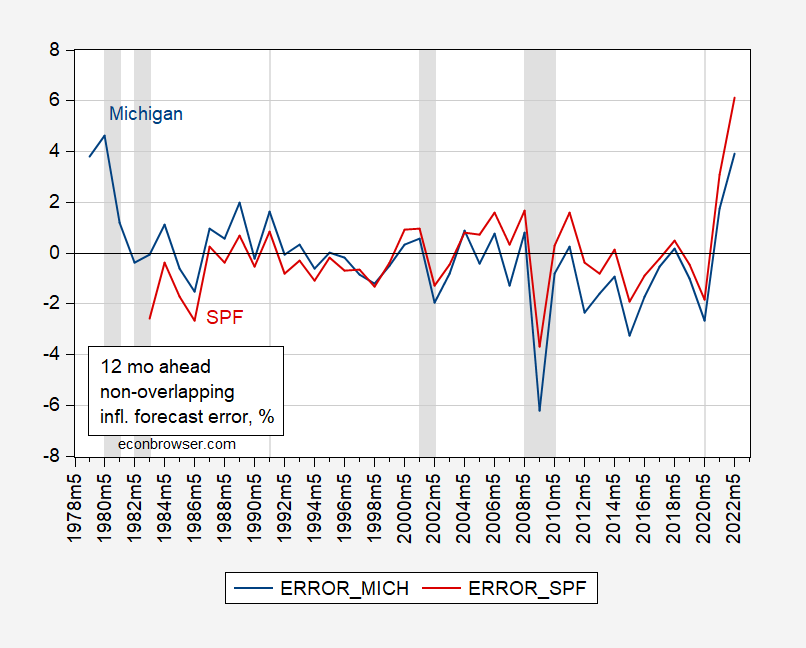

To see nonoverlapping forecasts, I sampled at May of each year:

Figure 2: Michigan 12 month ahead forecast error (blue), and Survey of Professional Forecasters median forecast error (red), in percentage points, in May. NBER defined peak-to-trough recession dates shaded gray. Source: BLS via FRED, University of Michigan via FRED and Philadelphia Fed SPF, NBER, and author’s calculations.

From 1986M05-2019M05, SPF forecasts exhibited smaller error than Michigan (18 bps vs 43 bps), and smaller root mean squared error (12 bps vs. 15 bps). (See more discussion of different characteristics of professional economists’ views vs. households, see this post.) Obviously, since the pandemic’s onset, this pattern has reversed – although there are only 3 nonoverlapping observations, so it’s hard to judge statistical significance.

To summarize, during the Great Moderation, professional forecasters did better (and exhibited less upward bias) than consumers/households. That relationship might have been upset during the pandemic. However, in both cases, forecast errors were highly correlated (adjusted R2 at 0.68).

That’s actually pretty amazing. The graph surprises me.

Menzie, I have been semi-harping lately about how people like Summers and WSJ’s Greg Ip etc have been hypocritically lecturing (they remind me of Uncle Frank in “Home Alone”) Fed inflation forecasts. Is there any number we could use to compare “the average” private economist’s inflation forecasts with the Fed inflation forecasts?? Even if it’s only for 5 yrs or something?? “Ironically” I’m assuming the Fed inflation forecast would be the harder one to find, to pick the correct barometer, since you have guys like Greenspan and Blinder with sharp differences in opinion sometimes?? But there has to be a “average” or ‘quoted” number there also, yeah??

Moses Herzog: Depends what you mean by “Fed forecasts”. Do you mean the Board economists, as represented in the Greenbook? If so, then use scholar.gooogle.com and type in “greenbook” “inflation” “forecast”. If you mean FOMC members, you do the same procedure. A recent working paper: https://www2.gwu.edu/~forcpgm/2021-003.pdf

I found this, after being too lazy to search before asking you the question. But this is obviously GDP, not an isolated look at inflation forecasts.

https://www.stlouisfed.org/publications/regional-economist/third-quarter-2019/economic-forecasting-comparing-fed-private-sector

I guess I’m leaning towards whatever would be the “closest representation” to FOMC inflation forecasts, since FOMC is the one that “draws the fire” of….. folks like Summers. I will look very closely at your link after posting this comment.

I like the Yanki Kalfa paper BTW. I think it points out the variation in FOMC members’ opinions like what I mentioned on Blinder and Greenspan, and even points out differences in opinion between regional Fed banks. Just as a trivial aside when I was late teens/college age I liked the Minnesota regional bank best, but now I am a old man I think each regional bank has a “flavor” that is likable in some sense. Anyways this paper isn’t exactly when I am looking for but your key word search suggestion has certainly got me into the ballpark. Thank you Menzie, it is appreciated,

Hmm, so you were a fan of hardline rational expectations new classical models in your youth, eh, Moses?

Well, from about the age of 13 I was mostly into finance. So the first two books the really grabbed me was Peter Lynch’s “One Up On Wall Street” and Benjamin Graham’s “The Intelligent Investor”. Mine was a hardcopy version but it had a outside cover that was like a kelly green. And just like Buffett advised I tried to pay strong attention to chapter 8 and chapter 20. I think My Dad bought it for me, but I can’t remember now. You’d think I would remember that because it was one of the greatest gifts I ever got in my life, and I was excited beyond anything to have my own copy. I became obsessed with the Margin of Safety principle and Book value per share. Literally obsessing over the concept. And I think it also had a Buffett epilogue to it and talked about the performance of Sequoia Fund and those things. I didn’t get interested in Economics in a serious way until I took the very simple undergraduate courses. Mine was taught by, if you can believe or not a graduate of Chicago School of Economics. He had also been an AWACS navigator in the Air Force, and I took him for both my macro and my micro, because I loved his class and he wasn’t too intensive on graphs. If you knew what happened with this line shifted or that line shifted it was mostly good enough. I didn’t really have ideology back then. I knew I was Democrat, but I wasn’t terribly conscious how economics fit into my political leanings. But over time, I guess I mostly leaned to Keynes and John Hicks, and then I don’t remember the exact time, but I wanted to read anything written by Krugman. It’s kind of hazy now but I think I may have even been reading Krugman when I was in high school and that helped me a lot when I finally took the undergrad courses. But certainly before I got to college, I don’t think I was that conscious or aware of the different “schools” (in the very broad sense) of Economics. I remember even reading (before I was in college??) Milton Friedman’s son’s book “Hidden Order” and enjoying that book a lot. And I knew I didn’t like Milton Friedmon, but I liked David Friedman’s book, so it still left me confused where my thoughts fit on it~~because the book was compelling to more a right-wing style of thinking. It’s an underrated book for beginners to Economics in my opinion. That’s saying a lot coming from me because I really don’t like Milton Friedman in many ways.

https://www.amazon.com/Hidden-Order-Economics-Everyday-Life/dp/0887308856

But I’ll tell you the two books that really hit me deep deep into my heart and mind, either in high school or college, probably very late high school. This one:

https://www.amazon.com/Age-Diminished-Expectations-Third-Economic/dp/0262611341/?_encoding=UTF8&pd_rd_w=7oiDk&pf_rd_p=91202c6f-1c11-4e3d-b51a-3af958cedd30&pf_rd_r=84JWRH988XPDYHSWEBCQ&pd_rd_wg=LSWQu&pd_rd_r=0c29e5a9-6af0-4ea4-8fb1-574f236595cf&content-id=amzn1.sym.91202c6f-1c11-4e3d-b51a-3af958cedd30&ref_=aufs_ap_sc_dsk

And this one:

https://www.amazon.com/Peddling-Prosperity-Diminished-Expectations-Paperback/dp/0393312925/?_encoding=UTF8&pd_rd_w=7oiDk&content-id=amzn1.sym.91202c6f-1c11-4e3d-b51a-3af958cedd30&pf_rd_p=91202c6f-1c11-4e3d-b51a-3af958cedd30&pf_rd_r=84JWRH988XPDYHSWEBCQ&pd_rd_wg=LSWQu&pd_rd_r=0c29e5a9-6af0-4ea4-8fb1-574f236595cf&ref_=aufs_ap_sc_dsk

Those two books had a deep impact on my thinking and how I viewed the world. I haven’t read them in YEARS, but it’s basically the basis or foundation from everything there on. Lester Thurow’s books also impacted my thoughts. I got 2-3 of his books back then. As you might have guess not academic works, Economics books written for a pop culture audience:

https://www.amazon.com/Head-Coming-Economic-Battle-America/dp/0446394971/ref=sr_1_4?crid=XNX6UR22XBXM&keywords=paul+thurow&qid=1655873796&s=books&sprefix=paul+thurow%2Cstripbooks%2C65&sr=1-4

https://www.amazon.com/Zero-Sum-Society-Distribution-Possibilities-Change-ebook/dp/B00A4JNNNS/ref=sr_1_1?crid=25O1TEF521GMQ&keywords=lester+thurow+zero+sum&qid=1655873954&s=books&sprefix=lester+thurow+zero+sum%2Cstripbooks%2C66&sr=1-1

I think the short answer to your question would be, as a finance person I originally was drawn to rational expectations, and then over time started to view rational expectations as unrealistic to reality. In Graham’s words. “Mr. Market” was often wrong, or Mr. Market was “very wrong” inside of certain time frames, and so I felt a lot of the time “actors” in economics are irrational not rational. Krugman’s “written for a popular culture audience” books and columns most influenced my early economics ideas. And really still do, everything I believe now sprung out of that.

Maybe a very “simpleton” answer to you, but an honest answer to your question.

Moses,

My my, quite an answer. Thanks. So presumably somewhere along the line as you increasingly took Keynes seriously maybe you learned that the folks in Minneapolis were the ultimate purveyors of the idea that “Keyneis is passe.” These days they are less likely to say that so definitely there. although still more likely to do so than at most other regional Feds., or even at Chicago itself.

I used to get hardcopy version of “The Region” sent to me free by mail. And I would read those pretty thoroughly. I guess it became a cost/environmental issue and they stopped offering the hardcopy versions and now you can only get the digital. I read it mostly during the Gary Stern years. It seemed to me to get watered down and muddled not long after they switched to the digital, like they were intentionally trying to kill off the readership. So I gave up checking in on it, maybe like 2010 or something?? I don’t know, I’m not as good at demarcating time as I used to be.

BTW I’m not impressed with Kashkari at all. Yes, I am sure he is very intelligent, but he strikes me as a man with his head in the clouds, ZERO concern for the common man, who has no moral compass and is in fact amoral. I don’t expect you to a agree with me on this, but I have my own way of gauging people, and Kashkari scores low as a human being.

Moses,

I do not have a strong feeling about Kashkari one way or the other. Bigger issue for me has been staff people there and their links to similarly thinking U. of Minnesota gang. In what I consider to be the bad old days the most important figure was Ed Prescott, who was ideological and hardline, making people like Lucas and Sargent look like soft soap. But then he left some time ago, and the place has become more moderate and complicated.

This has also coincided with the generalization and spread of the DSGE macro models, which Minnesota was the great fountainhead of, with the original ones coming from Prescott and those around him, being pure ratex and structured with serious anti-Keynesian ideological bias. As these models spread elsewhere and became the standard they got moderated and loosened in their New Keynesian formulations.

The matter of the identities of the various regional Feds is a fascinating matter, although hard to keep track of. Many have identities tied to interests in their regional economies as well as histories based on the views of long time staffers, who generally have job security like tenured academics. So these identities tend to change slowly and do not necessarily reflect all that much who is the President of the local Fed, although when those stay in place for a long time they can put their imprimatur on a place gradually.

Another besides Minneapolis that has changed somewhat over time and partly in response to a crucial individual is indeed that fave for folks here for showing data in figures, the St. Louis Fed. It was for a long time from the 1950s forward the bastion of Chicago-style Milton Friedman-style old fashioned monetarists. In effect Minnesota was the fancy new version of Chicago influence, Lucas and ratex rather than Friedman as at St. Louis. But then the seriously brilliant Jim Bullard moved up out of the research staff where he was when I first knew him to become Research Director, and finally more recently to become President, from which position he has become one of the most important and influential of Fed policymakers on the FOMC.

But he also transformed the research operation at St. Louis. He did not end its monetarist connection, but updated it as the older monetarists retired, and indeed it is now the fountainhead of the so-called New Monetarists, not to be confused with the MMT people. with people like Stephen Wlliamson a leader there now of this group, who have a different approach from the old Friedman crowd. But Bullard has also diversified the staff so that people there are now producing a much wider variety of work following various approaches, and with Bullard himself an old hand at nonlinear dynamics models based on chaos theory and the like, which is how he and I first intersected. But he is also the main supporter of their data operation as well. So, that is an example of how a regional Fed can move on even as it maintains links with its past identity.

Oh, just as Minneapolis Fed research shop has people overlapping with U. of Minnesota econ dept., so one has that going on at St. Louis, where some of the research staff also overlap with the econ dept at Washington University there, with Williamson one of those.

I think you were the one who first drew out attention to the insanity coming from Texas GOP convention. It seems even John Kasich agrees with you:

https://www.msn.com/en-us/news/politics/kasich-says-even-clowns-were-embarrassed-by-texas-gop-convention-that-included-declaration-that-biden-was-not-legitimately-elected-and-called-homosexuality-an-abnormal-lifestyle-choice/ar-AAYHFGh?ocid=msedgntp&cvid=281ad4e4f37e4904b3f405ff55db07da

I always said (although he had some negatives) that if there was one Republican who I would have considered voting for back in 2016, it would have been John Kasich. I don’t regret stating that. If he had gone head-to-head vs Hillary for example, Kasich would have been a very easy choice for me. No wavering on that decision at all.

Stephen Colbert explains what really happened to his team during their lawful visit to the Capitol:

https://www.msn.com/en-us/news/us/stephen-colbert-explains-arrests-of-staff-members-near-u-s-capitol/ar-AAYHSQG?ocid=msedgntp&cvid=4d2456f13dee4de39fccb4f9372088b8

And yea he closed with a shot across Tucker Carlson’s lying brow:

Colbert did take issue with how some television personalities framed the incident. Fox News’ Tucker Carlson called the incident an “insurrection” at the Capitol building – despite it not happening in the actual building. “I’m shocked I have to explain the difference, but an insurrection involves disrupting the lawful actions of Congress and howling for the blood of elected leaders, all to prevent the peaceful transfer of power,” he said. “This was first-degree puppetry. This was high jinks with intent to goof.”

Gee – that Nobel Prize winning “economist” who gave us suppression theory and is revising the Quantity Theory of Money has told us that the average Joe knows much more about inflation that actual economists! I guess the evidence once again pulls the rug out from Princeton Steve!

I guess there must be inflation numbers in the green book (or plural green books)?? Then compare the green book numbers to WSJ private forecaster numbers over, say 10 years or something??

It should be noted, of course, that these are not independent estimates, so their close correlation shouldn’t be surprising. The household sentiment is going to be influenced by the media pundits and the media pundits are going to be influenced by the professional forecasters.

I keep saying “using WSJ private economist forecast numbers”. Though I don’t guess that would be a “bad representation” of private forecasters I am guessing you would tell me (correctly) that Philly Fed’s “SPF” number would be better, and probably easier since they “already did the hard work”.

About climate change and climate shocks, nationally and region to region, infrastructure development in China, from transportation, to energy provision and transmission to water conservancy, is undertaken regionally but with a national focus always in view. From a planning perspective the work of Filippo Natoli is excellent as a development template:

https://econbrowser.com/archives/2022/06/guest-contribution-does-monetary-policy-respond-to-temperature-shocks

https://www.globaltimes.cn/page/202206/1268673.shtml

June 21, 2022

China’s electricity demand sets new records amid heat wave, work resumption

By Qi Xijia

Demand for electricity in many Chinese localities has set new records amid searing heat and robust factory activity due to an accelerating economic recovery from recent COVID-19 outbreaks….

[ The point is to couple regional energy production with national transportation and transmission. The nature of infrastructure logistics development in China is to account for regional climate shocks beyond places of energy production. ]

https://www.nytimes.com/2022/06/21/opinion/inflation-interest-rates-fed.html

June 21, 2022

Is the era of cheap money over?

By Paul Krugman

Interest rates are up. Stocks, especially glamour stocks, like Tesla, are down. And the crypto crash has been truly epic. What’s going on?

Well, many people I read have been offering an overarching narrative that runs something like this: For the past 10 or maybe even 20 years the Federal Reserve has kept interest rates artificially low. These low rates inflated bubbles everywhere, as investors desperately looked for something that would yield a decent rate of return. And now the era of cheap money is over, and nothing will be the same.

You can see this narrative’s appeal; it ties everything up into a single story. Yet to paraphrase H.L. Mencken, there is always a well-known explanation for every economic problem — neat, plausible and wrong. No, interest rates weren’t artificially low; no, they didn’t cause the bubbles; no, the era of cheap money probably isn’t over.

Let’s start with those interest rates. Here’s a chart of the real interest rate — the interest rate minus the expected rate of inflation — on 10-year United States government bonds since the 1960s. (I used the average rate of inflation, excluding food and energy prices, over the previous three years to proxy expected inflation; good enough for current purposes.) There was indeed a huge decline in real rates after 2000:

https://static01.nyt.com/images/2022/06/21/opinion/krugman210622_1/krugman210622_1-jumbo.png?quality=75&auto=webp

Check out our low, low rates.

But was this decline “artificial”? What would that even mean? Short-term interest rates are set by the Federal Reserve, and long-term rates reflect expected future short-term rates. There’s no such thing as an interest rate unaffected by policy. There is, however, something economists have long called the “natural rate of interest”: the interest rate consistent with price stability, neither high enough to cause depression nor low enough to cause excessive inflation.

So, is the claim that the Fed was consistently setting interest below this natural rate? If so, where was the runaway inflation? In fact, until 2021, inflation consistently came in more or less at the Fed’s target of 2 percent a year.

But why was the natural rate so low? The immediate answer is the Fed learned from experience that it had to keep rates low to keep the economy from slipping into recession. I’ll get to the deeper answers in a minute. But if you think the Fed was setting rates too low all through that period, you’re in effect saying that the Fed should have deliberately kept the economy depressed in order to avoid … something….

“You can see this narrative’s appeal; it ties everything up into a single story. Yet to paraphrase H.L. Mencken, there is always a well-known explanation for every economic problem — neat, plausible and wrong. No, interest rates weren’t artificially low; no, they didn’t cause the bubbles; no, the era of cheap money probably isn’t over.”

I guess we could say Krugman was thinking about Princeton Steve’s amateur macroeconomics here. But of course Stevie comes up with a bizarre blizzard of whatever his single story really is. Now we could wish Princeton Steve would read the rest of Krugman’s latest seriously as it is very good. But we all know Stevie can never be bothered with actual economics.

Wandrea Shaye Moss is testifying the 1/6 committee. She is a wonderful woman who was a Georgia poll worker. What the vile racist pigs known as Donald Trump and Rudy Guliani did to her and her mother was worse than an old fashion lynching. I get that our Usual Suspects feel compelled to go out of their way to praise Trump. That praise of such disgusting people only shows how utterly corrupt and racist these defenders are.

More on the testimony of Wandrea Shaye Moss:

https://www.msn.com/en-us/news/politics/georgia-election-worker-s-gut-wrenching-testimony-on-being-targeted-by-trump/ar-AAYHKRX?ocid=msedgdhp&pc=U531&cvid=58dbeb02802c4f2eab1fd9d24ce3c997

Donald Trump and Rudy Guliani are the lowest forms of racist pigs ever.

US Macroeconomists Survey

https://www.igmchicago.org/wp-content/uploads/2022/06/RESULTS-2022-06-06-Survey-05.pdf

Bruce Hall: Sorry, why did you post this? It was the subject of an entire blogpost, upon which you commented. Is there some aspect of the survey that you wish to bring our attention? I am particularly interested in knowing, since I’m one of the survey respondents.

I suspect here Bruce may be attempting a phony rhetorical move I call “a Barkley”. I named it after Barkley Rosser Jr. That is where you want credit for a prediction without actually putting your neck out on the tree stump. Bruce is probably implying he thinks PCE inflation will exceed 3% for the year 2023.

When I looked at this – the forecasts for things like the unemployment rate and economic growth are pretty strong. Oh wait – inflation might continue to be a wee bit above inflation which of course to the MAGA hat wearing moron we call Bruce Hall means the sky is falling.

Bruce did wait a long time to comment but when he saw CoRev and Princeton Steve were both Trumping the level of stupidity up to 11, he decided to surpass them with this incredibly dumb comment:

Bruce Hall

June 13, 2022 at 3:46 pm

Sorry, I forgot it was the same information. And I did notice you were one of the participants.

However, I noted in the context of this post that there was a wide difference of opinion among the participants on both inflation and if/when a recession would occur [to be expected even among professional economists]. It will be interesting to compare the median results of that survey’s responses to how consumers/UM survey responses fare to the extent that they can be compared… especially expectations about a recession and inflation.

I have no reason to doubt that we are not in a recession as normally defined contrary to what some claim, but there are some significant economic dislocations occurring which I are a combination of some actions by our government and a worldwide response to the Russian invasion of Ukraine, specifically oil/natural gas markets and coming soon… food. The US may not be impacted as much as Europe because we are still close to energy independence which means we should have sufficient supplies, but that doesn’t mean there won’t be economic pain as a result of high energy prices.

One question that wasn’t addressed in the survey of macroeconomists was a prediction about real wages. To the extent that they lag overall inflation (not just core CPI), there could be real political problems and probably some ill-advised attempts to control prices and mandate higher production (like Biden’s recent letter to the oil industry).

Bruce,

Now now, what you really need to be ashamed of is that Moses has caught you “attempting…a Barkley,” and one named apparently for me, “Barkley Rosser, Jr.” See, it would be OK, admirable even, if it had been the sort of “Barkley” named for my late father, “Barkley Rosser, Sr.” I am sorry that I am not able to tell you what you should have done to make it clear that you were attempting the second type of “Barkley” rather than the first, tsk tsk.

https://news.cgtn.com/news/2022-06-21/-Chinese-mainland-records-37-new-confirmed-COVID-19-cases-1b2qi8zIDgQ/index.html

June 21, 2022

Chinese mainland records 37 new confirmed COVID-19 cases

The Chinese mainland recorded 37 confirmed COVID-19 cases on Monday, with 9 linked to local transmissions and 28 from overseas, data from the National Health Commission showed on Tuesday.

A total of 105 asymptomatic cases were also recorded on Monday, and 1,449 asymptomatic patients remain under medical observation.

The cumulative number of confirmed cases on the Chinese mainland is 225,318, with the death toll from COVID-19 standing at 5,226.

Chinese mainland new locally transmitted cases

https://news.cgtn.com/news/2022-06-21/-Chinese-mainland-records-37-new-confirmed-COVID-19-cases-1b2qi8zIDgQ/img/721f4558921a40b5954d53d0e859925f/721f4558921a40b5954d53d0e859925f.jpeg

Chinese mainland new imported cases

https://news.cgtn.com/news/2022-06-21/-Chinese-mainland-records-37-new-confirmed-COVID-19-cases-1b2qi8zIDgQ/img/eb93b5fb8c594a3da7065b56218142f3/eb93b5fb8c594a3da7065b56218142f3.jpeg

Chinese mainland new asymptomatic cases

https://news.cgtn.com/news/2022-06-21/-Chinese-mainland-records-37-new-confirmed-COVID-19-cases-1b2qi8zIDgQ/img/35a5c0130c0d451b81e4773b28d97149/35a5c0130c0d451b81e4773b28d97149.jpeg

https://www.worldometers.info/coronavirus/

June 20, 2022

Coronavirus

United States

Cases ( 88,054,080)

Deaths ( 1,038,385)

Deaths per million ( 3,101)

China

Cases ( 225,281)

Deaths ( 5,226)

Deaths per million ( 4)

https://fred.stlouisfed.org/graph/?g=QOkD

January 30, 2018

Life Expectancy at Birth for Euro Area, United States and China, 2000-2020

https://fred.stlouisfed.org/graph/?g=QOkE

January 30, 2018

Infant Mortality Rate for Euro Area, United States and China, 2000-2020

Ron Johnson should be in prison right now:

https://www.rollingstone.com/politics/politics-news/jan6-ron-johnson-electors-trump-coup-1371957/

Sen. Ron Johnson Wanted to Hand Deliver Fake Electors to Pence on Jan. 6

The senator from Wisconsin, who is up for reelection this year, may have a little legal exposure following Tuesday’s committee hearing

Lock him up!

Bruce did wait a long time to comment but when he saw CoRev and Princeton Steve were both Trumping the level of stupidity up to 11, he decided to surpass them with this incredibly dumb comment:

Bruce Hall

June 13, 2022 at 3:46 pm

I wonder whether the difference in error isn’t largely the result of professional forecasters taking the Fed’s ability to control inflation more seriously than the public does? When inflation is high, professionals expect it to come down to target, when low, professionals expect it to rise to target, more quickly than the public does?

macroduck: I think that’s part of it. Another part is that when consumers are asked what is *current* inflation, they over-estimate.

I guess they are focused on the price of their latest meal such as those bagels Princeton Steve is trying to find at Cape Cod.

Don’t forget avocados.

I guess I’m the last person on the blog who should poke fun of this when I quote my local gasoline and groceries here sometimes. And I do put some small weight on “anecdotal evidence”. But, I mean, I do think he gets more melodramatic than I do about it.

What is the model professional forecasters are using? Neither Menzie nor Jim has introduced one into this conversation. As we see from Menzie’s prior surveys published here, forecasters are largely clueless about future inflation at turning points (ie, they rely on past inflation to anticipate future inflation). In any event, neither Jim nor Menzie has floated a model of inflation beyond ‘inflation expectations’, which themselves are formed by historical inflation.

So, let’s see a fundamentals model. Then we can discuss why people don’t understand that.

From the St. Louis Fed:

During periods of underutilization, when the money supply is increased, there will be an increase in output; however, as those idle resources are utilized—as idle factories return to production and the labor market begins to tighten up—an increase in the money supply will be reflected in the price level. This is inflation caused by too much money chasing too few goods.

There’s a model for you.

https://www.stlouisfed.org/education/feducation-video-series/episode-1-money-and-inflation

This statement is up there with 2 + 2 = 4. Or brushing your teeth every morning. But at least it was neither your dopey suppression term or the discredited Quantity Theory.

Why would you think professionals rely on one model? Why should our hosts be responsible fot telling you about those models? Look them up yourself.

Menzie brought up the matter of inflation expectation errors.

And you’re the one posing the question:

“I wonder whether the difference in error isn’t largely the result of professional forecasters taking the Fed’s ability to control inflation more seriously than the public does? When inflation is high, professionals expect it to come down to target, when low, professionals expect it to rise to target, more quickly than the public does?”

Do we have a model of inflation? If so, what is it? I know what’s on the St. Louis Fed’s website, so I have to believe that’s kind of their model of inflation. If you’re talking about errors, you’re begging the question of models. Menzie seems to have plenty of time to dig up three year old comments from CoRev. Given that inflation is running near 9%, that it is literally gutting the Democratic Party, that it is causing enormous hardship across the economy, I don’t know, maybe Menzie would like to give us some insight into how macroeconomists think about inflation nowadays. I think it is a both a relevant topic and a non-unreasonable request.

Steven Kopits: I can assure you that the St. Louis Fed does not use the quantity theory to forecast inflation. It hasn’t for a long time, since the demise of the “St. Louis model”, essentially a reduced form equation. That webpage was a pedagogical site aimed at high school students.

Ah, as you know what model they use, enlighten us.

(And I imagine you should send them a note to take down that website.)

Leonall C. Andersen and Keith M. Carlson

International Economic Review

Vol. 15, No. 2 (Jun., 1974),

You need to thank Dr. Chinn for providing a link to this paper which I happened to read as a first year undergrad. As I have tried to tell you many times – no serious economist have taken your vaunted Quantity Theory for the last 50 years. Of course you as usual paid no attention.

Before your next boring bloviating BS – READ THIS PAPER. Damn!

“That webpage was a pedagogical site aimed at high school students.”

Dr. Chinn is right. I figured this out within a minute of reading its writing. And you thought this was some advanced macroeconomic model? Well it is advanced compared to your incessant BS. It might help if you go down to the community college near where you lived and signed up for a basic principles class.

“Why should our hosts be responsible fot telling you about those models?”

It turns out our hosts try very hard to convey the insights of various macroeconomic models. But here’s the problem. Princeton Steve is too busy bloviating his BS to read these excellent posts.

I believe that I have read more than once that Warren Buffett says predicting inflation and interest rates is a fools’ game. I hear lots of criticism from you and Larry Summers, but I’m missing the part where you and Larry tell us the exact numbers you are expecting. But then, other than for 3 Stooges humor I can’t say I’m paying attention much to what you say. You predicted $100 oil by late summer 2021. Didn’t happen. I believe not that long ago you were predicting $200 oil. So….. what is it you say that I’m going to take in a serious way?? You have to throw a few darts that don’t hit the bar waitress in the face before I start taking you seriously.

And the EIA was at $50. Pick your poison.

WTI dropped today to $105.40. Seems to be heading down.

When did they make this forecast? I’m sure they did not realize that Putin would invade Ukraine when they made this forecast. If you are trying to tell us relevant exogenous events should not matter when evaluating forecasts – then you are indeed the dumbest consultant ever.

“What is the model professional forecasters are using?”

Why don’t you email them and see if they answer. I can guarantee their models neither mention “suppression” or the Quantity Theory of Money. After all neither one of your nut ball ideas fits the definition of a fundamentals model. Then again – you are the most clueless person ever when it comes to the fundamentals of macroeconomics.

You and I both know what the situation is, Menzie. But let me explain for the readers.

If the Fed were using a QTM model, then current inflation would be easy to explain, as it would be to chart out the course of future inflation. If the Fed is using another model, then one of two things must be true:

1) the model is wrong, because it failed to anticipate current inflation, or

2) the Fed signed off on current inflation rates

So which is it?

Steven Kopits: If you took the quantity theory seriously with trend stationary velocity, you’d have a *lot* more inflation. See, e.g.: https://econbrowser.com/archives/2020/12/inflation-looming-phillips-curve-vs-quantity-theory

What is the model you are using or the Fed is using? Are you saying that the Fed staff signed off on 9% inflation or that their models sucks?

Steven Kopits: Read the post. I’m using the quantity theory as a long run cointegrating vector, and estimating the pace at which the price level (which is the inflation rate) reverts to that long run relationship.

“Are you saying that the Fed staff signed off on 9% inflation or that their models sucks?”

Name me one model that has had a history of zero forecast errors. You can’t. Especially your outdated and discredited Quantity Theory.

To appearances, the Fed has blown up the economy. This is not just a matter of ‘forecasting errors’.

The sobering reality is that Fed staff signed off on a 40% increase in M2. Were there any protests? Did anyone resign? Did any Fed staff write an op-ed in WaPo or the NYT about ‘why they had to speak out’? No?

If not, why not? Was it because they did not have a model? Well, the QTM model is reasonably well established. So did they just plain screw up?

Or did Fed staff okay an inflation risk at the level of 9% p.a.?

Why should the pubic have any faith in the Fed or Treasury at this point? Indeed, why should they have any faith in the economics profession, other than in Larry Summers? No one knew, or could figure out, or at least highlight, the risks of unchecked money supply growth? I pulled it right off the graph. Summers op-eds make the risk entirely clear. When I first read that M2 was up 40%, my initial reaction was, “Well, that’s probably not going to end well.” Did no one at the Fed have this reaction? If so, why didn’t they come forward?

So you tell me: Why did the Fed just drive the US economy off the cliff? Why didn’t the economics profession speak up? Is everyone in the profession other than Summers an incompetent? Or is the economics profession and the Fed ‘the swamp’? Is it all about partisan pandering? The average American could be forgiven for thinking so, that the Fed — and its technical staff — is just another tool of the elites to use against the middle class.

At the end of the day, democracy depends upon, among other things, the confidence of the public that the bureaucracy is competent and playing a fair game on a level playing field. If democracy cannot deliver competent governance and the bureaucracy is perceived to be the tool of the elites against the middle class, why does the middle class need democracy? Could social conservatives not reasonably come to the conclusion that they would have been better off with a successful Trump coup than an incompetent Biden administration?

The elites continually bemoan the risks to democracy, but take no responsibility for the credibility necessary to sustain it.

Steven Kopits: You should take a look at ECB’s balance sheet…

I live in the US, my interest is in US policy.

OK. So let’s quote from you, December 13, 2020, that is, about 18 months ago:

Should I be worried about imminent inflation? The Economist thinks we should be on guard, even if not likely. If I believed in the Quantity Theory of Money (MV = PY), maybe I should. Let consider what it implies, given the sharp jump in money stock. At the end of November, M2 was about 22% above levels the previous November — so naively, one might expect over time a 22% increase in price level.

OK. Given that M2 is now up 39%, if you’re using a QTM model, you should be pretty much apoplectic.

What about a simple Phillips Curve specification involving the output gap (as defined by the CBO)? Here one finds a little more supportive evidence, but not overwhelming. There could be many reasons for this outcome — instability in the slope relationship, failure to account for expectations (anchored vs. accelerationist), or mismeasurement of potential GDP — but at first glance one would be hard pressed to determine the better predictor of inflation. Of course, there is a very large literature resurrecting the Phillips curve (Coibion et al. for measuring expectations correctly, Blanchard et al. for accounting for structural breaks, among others), so one rightly be more persuaded by the Phillips curve approach.

I have to tell you, Fig. 3 of that post (https://econbrowser.com/archives/2020/12/inflation-looming-phillips-curve-vs-quantity-theory) is about as obscure a graph as I have seen. Does that say that an output gap of zero is consistent with 2.2% inflation, and that the economy would have inflation of about 2.5% inflation if the economy were operating at 4% above potential output?

That model makes absolutely no reference at all to M2, does it? You could increase the money supply tenfold and it would have no impact on inflation, as I understand the construct. Is that right? Do you believe that’s true?

And finally, you write:

Does this mean we have no need to worry. If one believes that we will be way below potential GDP for a while, then no. Using the WSJ’s December survey mean forecast, and the CBO’s estimate of potential GDP, end-2022 is when one might start worrying about inflation…

Does this mean you are not worried about inflation yet?

Now you are just lying. Stop cherry picking quotes out of context and properly note the entire post which shows how utterly discredited any formulation of the Quantity Theory is.

Look – you are truly a bombastic boring baffoon which we tolerate to a point. But damn – this discussion has gone over the cliff. Stop writing garbage and start reading basic economics.

“You could increase the money supply tenfold and it would have no impact on inflation, as I understand the construct.”

I guess you did not get how fast M2 rose as a response to the Great Recession. Or maybe you are stupid to realize that GDP/M2 fell a LOT and it is not going back to 1.8 any time soon.

Which begs this simple question – HOW UTTERLY STUPID ARE YOU?

“That model makes absolutely no reference at all to M2, does it? You could increase the money supply tenfold and it would have no impact on inflation, as I understand the construct. Is that right? Do you believe that’s true?”

I guess Stevie has no effing clue how fast M2 has been growing since 2008:

https://fred.stlouisfed.org/series/M2SL

From 2008 to the end of 2019, M2 more than doubled. Did the price level double? Not nearly. Heck nominal GDP did not double either. Not even clue.

And when the pandemic first hit, M2 rose very rapidly. Now I do not remember the 2020 hyperinflation. Do you remember that?