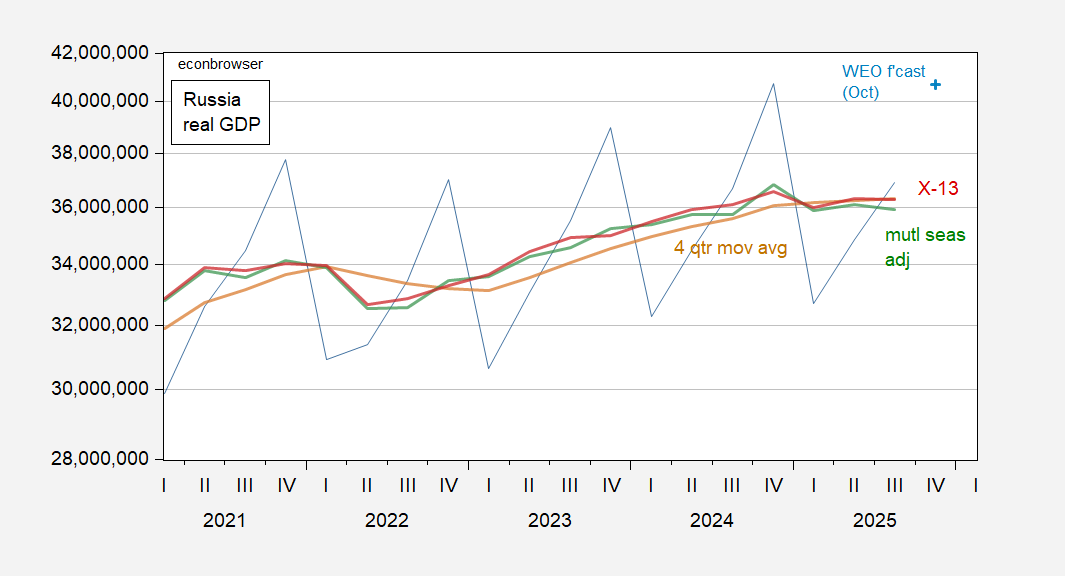

Official statistics suggest the country is below recent business cycle peak.

Figure 1: Russian real GDP, n.s.a. (blue), seasonally adjusted by author using X-13 in logs (red), using multiplicative seasonals (green), and 4 quarter moving average (tan). Source: IMF, IFS, and author’s calculations.

I’m using a loose definition, based on GDP. Since the Russian Federation does not publish a seasonally adjusted quarterly series for real GDP, I have seasonally adjusted using Census X-13 (with log transform, X-11 ARIMA) and multiplicative seasonal adjustment, applied to aggregate GDP. I also plot the 4 quarter trailing moving average. Note that while output is below recent peak, it has not declined two consecutive quarters, a typical rule of thumb measure.

In terms of forecasts, it is true that Russian output did not fall as much in 2022 in many Western forecasts. For instance, the March 2022 Bloomberg consensus was for a 9% decline q4/q4 in 2022, while the actual (as reported) was only about 2%.

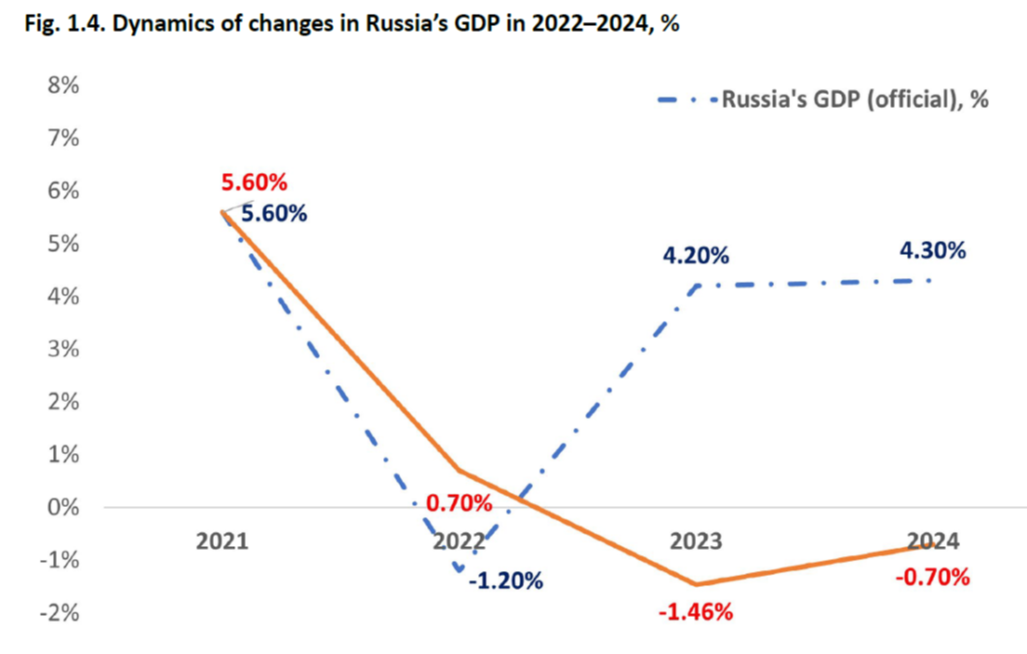

Of course, one has to believe in the deflators used in order to believe in the real GDP statistics. As noted previously, the official Russian CPI seems to have been running cooler than a private sector series, ROMIR — until that series ceased publication (i.e., was induced to cease publication). Here’s the official CPI and GDP deflator series. Vlasiuk et al. (2025) plot official series, and their estimate of inflation.

Source: Vlasiuk et al. (2025).

A higher price level for a given nominal GDP implies a smaller real GDP. Vlasiuk et al.‘s estimate is that Russian GDP has been decreasing y/y in 2023 and 2024.

Source: Vlasiuk et al. (2025).

Simple addition suggests that Russian GDP is about 1.5 percentage points below 2021 levels, rather than 7.3 percentage points above.

There’s a lot of uncertainty about the correct values for GDP deflator inflation. However, we can be pretty sure that actual GDP growth is less than that reported.

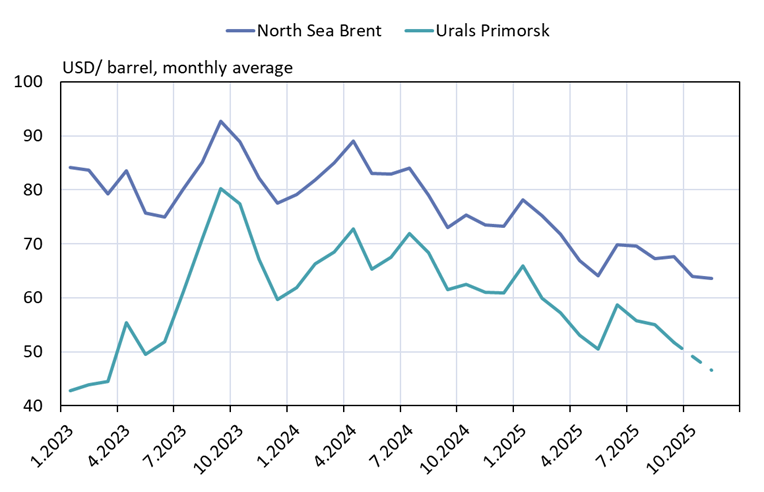

If this is true, the strain on the Russian economy servicing the war effort must surely be onerous, so much so that it’s unclear how much longer the offensive can be maintained, particularly with oil revenues decreased.

Source: BOFIT, Dec 5, 2025.

I wonder what impact losing Venezuela (helping Russia – move oil through opaque trading networks) will impact the Russian economy? Or given that this is the Trump admin – maybe it has no impact at all.

Venezuela’s regime, which hasn’t changed much at all, still has to think about its own preservation. Chinese and Iranian air defense equipment may have failed to keep U.S. aircraft at bay – we don’t know – but that doesn’t diminish China’s economic role. Chinese money may be indespensible to Venezuela’s leaders. The same maybe true of Russia’s oil trade. How much is Venezuela making by facilitating Russian oil trade.

The Wall Street brigade headed to Caracas may be intended to weaken China’s – maybe Russia’s – impotance in Venezuela, but the Wall Street brigade hasn’t landed yet.

We, meanwhile, have left the thugs in charge in Venezuela, presumably because the felon-in-chief and his minions see that as in their interest. If the Rodriguez regime sees Chinese and Russian money as essential to its short-term survival, will the felon get in the way? But maybe that was your final point – the felon may not care.

Just as with the attack on Iran, the Orange Clown in our White House, care only for the spectacle on Faux News, not for the reality on the ground. Iran’s path to nuclear weapons may only have been delayed a few weeks/months, but Trump got some manly-man showtime on Fox. The new thugs in charge of Venezuela will now be able to blame US for the failures of their economic and political idiocies.