As the Fed sets in place the road map to withdrawing monetary stimulus, I wonder how it is that so many believed the Fed’s implementation of unconventional monetary policy would lead to surging high inflation. Examples include House Budget Committee Chair Paul Ryan, who stated in November 2008 2010:

I think it’s going to give us a big inflation problem down the road.

The source for the above statement, Reuters, also quotes Sarah Palin and Ron Paul.

Time to look back. Here are some graphs depicting inflation and inflation expectations as they evolved.

Figure 1: Annualized three month inflation for CPI (blue), personal consumption expenditure (red), core CPI (bold dark blue), and core PCE (bold dark red), in percent. Source: BLS, BEA via FRED, and author’s calculations.

Figure 2:Expected inflation calculated from difference between 10 year constant maturity Treasuries and TIPS (dark blue), from 5 year (purple), and mean expected 10 year CPI inflation from Survey of Professional Forecasters (green +), in percent. Source: BLS, BEA via FRED, and SPF from Philadelphia Fed, and author’s calculations.

The obvious point is that there has been little evidence of inflation “getting out of control”, even as several bouts of quantitative easing were undertaken. In fact, inflation and inflation expectations have been remarkably quiescent. Why were these people so mistaken? There are at least two competing explanations, consistent with the statements that were made, and the observations we have:

- The observers were ignorant of economics.

- The observers wished to whip up hysteria in order to prevent the Fed from undertaking expansionary policies.

Both are plausible. The second possibility is more interesting to me (the first possibility is examined here). Why would these people wish interest rates to remain high? Perhaps they hoped that high interest rates would force a reduced level of government spending –- i.e., it would have “starved the beast”. In other words, instead of just cutting food stamps (SNAP) as the House is trying to do now (although not ag production subsidies [0]), even more swaths of the government could’ve been cut had monetary policy been less accommodative. Of course, the “starve the beast” hypothesis has had little empirical basis, as Jeff Frankel has pointed out (as well as Bruce Bartlett). But empirical evidence has not usually been marshalled on that side of the argument anyway.

A third argument, that Fed unconventional monetary policies were ineffective, and hence should not been undertaken, seems to run counter to recent empirical evidence indicating that the imminent cessation of QE has led to higher real interest rates (after all, if QE couldn’t push rates down, why should the mention of ending it pull rates up?). The increase in real rates since the Chairman’s June speech is depicted below in Figure 3:

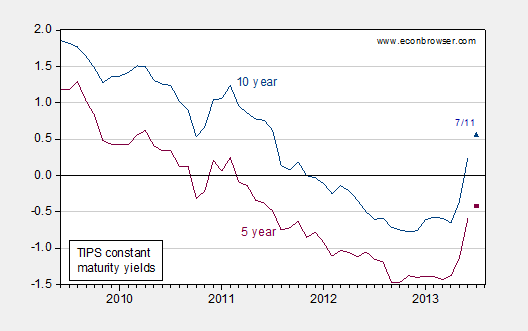

Figure 3: Ten year TIPS yields (dark blue), and five year TIPS yields (dark red), in percent. Source: FRED.

As Brad Delong observes, this is not good news, given that 2013Q2 GDP growth seems pretty poor. [1] Macroeconomic Advisers puts second quarter growth at 0.6% (SAAR).

A final graph depicts money base and gold prices, for those who believe gold prices are a summary statistic for all things under heaven.

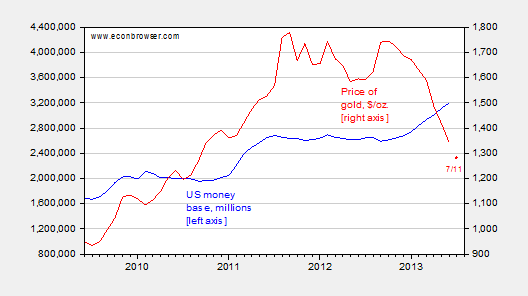

Figure 4: US money base, in millions of dollars (blue, left scale), and price of gold in London, 10:30AM, dollars per Troy ounce. Source: FRED.

Statements surrounding this graph I do think are more akin to the pure “tin-foil cap” sort (money base increase equals debasement; see this post).

My view is a 3rd reason, though one could argue it is related to the 2nd. It takes away the ill will motives and replaces them with belief, as in these people genuinely believe, for a variety of reasons, that for some reason this is wrong. I call this the “inchoate” factor: take an argument and marshall facts for it and I overcome your facts not merely because I want to assert my power but because I have inchoate reasons. These inchoate reasons may be religious belief, ideology or some general moral sense of what is right. They express as distortion and rejection of evidence, along with the repetitive manufacture of false evidence, and the imaginings of causal links that don’t exist.

In other words, we tend to assume people act rationally. The rational conclusion is that people – like so many of your commenters – spout economic nonsense because they want an outcome. I doubt that. I think people are more generally irrational than we normally credit – and more in line with the findings of behavioral science than economic models. It may be political or cultural disbelief or simply a tendency to leap to develop and adhere to irrational beliefs and conclusions. I don’t know. But if you were to model it, you’d add a factor – the inchoate factor – and you could characterize it if you wanted to do the research by how it manifests as evasion or denial when confronted in a study setting with facts that conflict with belief.

I remember in college – Ivy school – we had in my Soviet history course an unreconstructed Stalinist from India. He parroted the party line – remember, India’s communist party was Stalinist for a long time after Kruschev, etc. There was no famine, only the kulaks were eliminated, the 5 year plans were successful except when intentionally “wrecked”, etc. The professor confided he didn’t know how to grade him because he wrote his papers and exams the same way. It was absolute, incredible nonsense but he was unshakeable. His conclusions had no factual basis at all, except he was taught them and he believed them.

If you read the nonsense coming out many countries – hateful crap coming out of Arab nations, etc. – you understand the depth to which irrationality, not ignorance is the real underlying issue. One can understand an uneducated person spouts nonsense, but I can give example after example of educated people saying irrational things. You can say they are trying to manipulate people but I think the actual truth is they mean it, that they are irrational.

A third argument, that Fed unconventional monetary policies were ineffective, and hence should not been undertaken, seems to run counter to recent empirical evidence indicating that the imminent cessation of QE has led to higher real interest rates.

The “markets” are a mob of frenzied loons. If Ben Bernanke had been buying grains of sand on the shores of Pacific by throwing money into the waves and invoking Poseidon, the markets would have a psychotic break if he hinted he might stop. The loud obsessions of the blogospheric and financial press punditry with the quackery of QE has created a classic case of the madness of crowds. It’s very dangerous for our economy that this irrational fad for relatively insignificant asset-swapping placebos has taken hold.

While they are justifiably mocking the hyper-inflationistas, I think it is now also time for the pro-QE crowd to make some admissions as well. Because they said all along that part of the purpose of QE was to cause higher inflation – not hyperinflation of course, but just some regular 2.5%, 3%, or 4% inflation; something higher than the usual 2% target.

But that has not materialized, even after three hefty rounds of QE. And that stands to reason for those who have argued all along that QE is just a financial asset swap. QE swaps in non-maturing, non-interest bearing dollars for maturing, interest-bearing financial assets of roughly equivalent value. As a result, the cash flows attached to the financial assets that are sold to the Fed are re-diverted to the Fed and out of the private sector. So while QE injects dollars, it also removes dollars. Indeed, given the fact that the Fed’s net earnings have been so high since QE began, it is reasonable to believe that QE is actually extracting more dollar income than it is injecting.

Some of the pro-QE crowd have now retreated to the idea that QE was always about long-term interest rates all along, especially mortgage rates. Fair enough. But back in 2010 and 2011 when the QE enthusiasts were unfurling their flags, the story we were repeatedly told was that QE was aimed at increasing inflation and NGDP by virtue of some sort of mysterious “easy money” phenomenon working independently of the interest rate channel.

Professor Chin,

Your bias shows through each and every time you write. When I began reading I had no idea whether this post was the work of you or of Professor Hamilton. However, when I got to “starve the beast”I knew that you were the likely author and scrolled to the end that the very partisan half of the writing duo which produces this blog had indeed authored this piece. Of course you would love the starve the beast hypothesis as it neatly fits the prism through which you view the world.

I think that the preponderance of politicians have a very poor economics IQ and I think that it a real problem on each side of the political spectrum.

john jansen: I am thankful you have stopped counting four months as years, as you did in your previous comment. I’m happy to take the “ignorance” interpretation of Representative Ryan et al. However, as social scientists, I would like to be able to distinguish between the competing arguments. I do not find anywhere in your comment a means by which to do this; all I find is invective.

Further, if you would be so kind, I would like to know what specific bias you are pointing to — is there an error in data presentation or error in fact? In fact, I don’t believe I came to a conclusion; rather I laid out several hypotheses. When merely doing that constitutes “bias”, well…

Dan Kervick: Perhaps you are right about most of the pro-QE crowd’s views, but when I was teaching my classes about QE, I argued that QE had the intent of both increasing expected inflation and driving down interest rates along margins (term, credit) that the Fed could typically not affect. I agree that it has been more successful in the latter than the former. Certainly forward guidance was aimed more at the term dimension.

Menzie,

I guess I read the tripling of the base and no growth in M1/M2 as a failure on the part of the Fed. The biggest effect has been record bank profits. I guess this is the liquidity trap in its full bloom. Seems, though, when expectations really improve, that there should be some commensurate jump in M1/M2 too, and with it some inflation. I doubt the price level will triple anytime soon. But still, the threat is certainly there. Recent borrowings by major corporations, and refinancings and new mortgages should be putting upward pressure on M1/M2, no?

I was an inflation nutter for a long time. I think a major reason why we have not seen inflation is modern money creation is extremely complex and the Fed is only a portion of modern money creation, certainly not 100% and the deflationary pressures in the market out weighed the inflationary pressures of the fed. I’m still not sure I agree with printing money to buy assets of rich people at inflated prices, and maintaining the wealth inequality structure in place, but I’m no longer an inflation nutter.

They didn’t realize economic growth would be so stiffled that velocity of money would be near zero.

This seems somewhat related: Japan’s stagnation: demand-side or supply-side?

There’s also an urge for a segment of the commentariat to see this all as some kind of religious-like morality play. Hard working real murkins confounded at every turn by the laughing joker-faced muslim kenyan socialist community organizer, Hussein Obama, and his grasping, dull-witted wife, Moochelle, who are trying to bankrupt America and seize our 401Ks to give to lazy stoop-sitting apartment dwellers in the inner city. You can see all those allusions in comments by the trolls here and on practically any internet comment thread.

On the retail end we have plenty of clients who are still huddled in their basements with their dried beans, their AR-15s, and their gold coins just waiting for hordes of looters from the big city to come try to take their stuff.

All but about 20% of this (the standard crazification factor) goes away with the election of Jeb Bush president in 2016. Hell, I will even vote for him if it makes this foolishness go away.

Regards.

I am surprised that an economist with your credentials would miss the obvious reason. They expected the Obama recovery would at some point, become a rapid recovery.

However, it turns out that Obama’s policies have caused firms to fear adding a full time employee to their payrolls. Hence, the recovery has been muted and defined by a shrinking labor force, tepid growth in full-time employment and much buffoonery surrounding the creation/implementation of Obamacare, Dodd-Frank, energy policy, etc.

There’s no better way to stifle growth than to create a HUGE shock to uncertainty. To argue that Obama’s policy mistakes have had little impact on growth is pure lunacy.

Economic policy uncertainty (EPU) has become the subject of contentious debate

since the recession of 2007-2009. Commentators have made two broad claims: first, that

policy uncertainty has increased since the onset of the recession, and second that this

increase in policy uncertainty has impeded the recovery. This paper seeks to investigate

both claims, finding strong support for the first claim and evidence in line with the

second claim as well.

http://economics.uchicago.edu/workshops/Baker%20Scott%20%20Measuring%20Economics%20Policy%20Uncertainty.pdf

Dan K,

There certainly were calls for the Fed to target NGDP and inflation at the same time that the various asset purchase programs were being implemented. That doesn’t mean most fans of asset purchases were claiming one would lead to the other. The logic of the inflation and the related NGDP targeting argument was based on Fed commitment. To the extent the Fed could make a credible commitment to raise either inflation or the sum of real growth and inflation, it could shift the value of current consumption and investment relative to future consumption and investment. That commitment could be carried out through either asset purchases or a longer period of low rates or both. Maybe some folks thought the asset purchase program was part of a pledge to target NGDP, but the Fed tells us why it does what it does, and it has not adopted NGDP targeting. There is a debate over whether the price stability goal of the Fed is satisfactorily met by a median estimate among Fed officials that inflation will return to target in the future on one side, or whether there needs to be actual evidence in the data of a faster rise of inflation. That is not the same as a pledge that asset purchases will result in higher inflation, but it is certainly an indication that some Fed officials think inflation needs to be higher and that asset purchases ought to be used to make it so.

Dear Professor Chinn,

Perhaps in addition to aaron’s comment about velocity, there are a couple of additional rational reasons, those without advanced economic degrees felt that inflation may accelerate with increases in money supply.

1. Beginning macroeconomic texts say that in the long run money is neutral. “If the Fed increases the money supply 5% a year, annual inflation will be 5 percent” (quote from a beginning macroeconomic text).

2. The Fed has not always managed money supply contraction or expansion very well. I think there is a general perception that the Fed’s contraction of the money supply in the 1930s helped to make the depression worse. Prior to Volker’s actions, we had a serious problem with inflation and I assume with money supply growth.

tj: Well, I have referenced the Baker-Bloom-Davis uncertainty several times (see e.g., here). You would be well advised to consider the main components of the index, and to look at the graph in the referenced post. There you will see where the peak uncertainty was (gee, debt limit debate — wonder who pushed that to the limit?).

I do agree that some people thought there would be a rapid recovery. Others of us had read the Reinhart-Rogoff book, as well as the other work by economists at the Fund. In fact, some of us even wrote about it! [post from January 2009]

AS: You will note that the introductory macro text refers to money supply, not money base. The distinction is important in an era of interest-on-reserves. Money supply is a mix of some liabilities of the central bank and private bank checking and/or saving deposits. Money base is liabilities of the central bank. The two differ, and are delinked as was well known when the Fed changed its operating procedures with respect to excess reserves.

Professor Chinn,

Thanks for providing the distinction between money base and money supply. I wonder if the distinction you mention and the concept of excess reserves and payment of interest on excess reserves contributed to the confusion as to the perceived risk of increased inflation. Reading the same introductory macro text as previously quoted, “Until September of 2008, banks held few excess reserves so total reserves were very close to required reserves.” Would not the complexity of the concepts and the change in the Fed’s policies regarding paying interest on excess reserves add to the confusion of those without advanced economic degrees and perhaps contribute to rational if uniformed fears of increased inflation due to manipulation by the Fed?

At first I thought expanding the Fed’s balance sheet would lead to inevitable inflation, but based on the evidence and Krugman’s rants about liquidity traps helping me recall my econ 102 AD/AS model, I realized inflation isn’t very likely. Conservatives can update their beliefs.

But rather than rubbing politicians’ (c.f. economists’) noses in their bad predictions, why don’t we come up with some ideas to get the economy moving again.

Moody’s Analytics’ high-frequency model has 2Q GDP at 0.5% right now. The economy is clearly faltering. Obama has been in office over 5 years. At this point, it IS his mess. What is he going to do about it, other than shut down coal-fired power plants and force employers to provide health care and thus raise their labor costs?

While I’m by no means on the right side of the political-economics center, its easy to imagine why Ryan and other traditionalists would have thought that hyper-inflation might result from the FED’s QE programs… Specifically: If political and economic pressure would be sufficient to maintain the nude capital reserve ratios fashionable prior to 2008, the QE injections would have increased liquidity on the order of 90 trillion in the USA.

I can credit much effort by both the German and British central banks and governments as well as the IMF in pressuring the rest of financial world to return to sanity. I’ve heard rumblings from the FED that reserve ratios greater than Basel 3 may be required in the US.

The FED’s efforts to paper over a $6 Trillion real-estate crater, as well as support a Federal Government requiring counter-cyclical funding have been Herculean. Unfortunately, there has been little progress in purging the legendary corruption in the financial and political worlds…

How hard will it really be for a future regime to cast caution to the wind and allow a new round of high finance circus performances? Is there really any long-term policy in place to prevent another round of looting?

Menzie

I know you can interpret a graph, but perhaps your political bias prevents an accurate interpretation of the BBD uncertainty index. The authors tag the debt ceiling debate, but to attribute the entire quarterly spike to it is a stretch. Obama signed the bill to raise the debt ceiling at the start of August 2011. The point is that the associated spike started from an already elevated level. If you download the monthly data (http://www.policyuncertainty.com/us_monthly.html) then you see that there are more than 20 spikes larger than the spike you refer to.

The index also misses a large component of uncertainty associated with the general trend toward placing policy creation in the hands of various agencies and boards headed by Progressives.

The consequences are only now beginning to surface. For example, companies with a few hundred workers are splittig into smaller companies, firing some workers and turning some full-time workers into part-time workers. This is just one example of flawed Progressive policy.

Others include Climate, Energy, Labor and Finance, literally wherever Progressive policy wriggles its way into U.S. Law.

Even some Progressives are starting to see the writing on the wall. The cracks are starting to form. It won’t be long before traditional Democrats demand their party back.

Dear Leader Reid and Leader Pelosi:

Right now, unless you and the Obama Administration enact an equitable fix, the ACA will shatter not only our hard-earned health benefits, but destroy the foundation of the 40 hour work week that is the backbone of the American middle class….

The unintended consequences of the ACA are severe. Perverse incentives are already creating nightmare scenarios:

the law creates an incentive for employers to keep employees’ work hours below 30 hours a week. Numerous employers have begun to cut workers’ hours to avoid this obligation, and many of them are doing so openly….

Taken together, these restrictions will make non-profit plans like ours unsustainable, and will undermine the health-care market of viable alternatives to the big health insurance companies….

we can no longer stand silent in the face of elements of the Affordable Care Act that will destroy the very health and wellbeing of our members along with millions of other hardworking Americans….

James P. Hoffa

General President

International Brotherhood of Teamsters

Joseph Hansen

International President

UFCW

D. Taylor

President

UNITE-HERE

http://blogs.wsj.com/corporate-intelligence/2013/07/12/union-letter-obamacare-will-destroy-the-very-health-and-wellbeing-of-workers/

tj: Gee, and here I thought my eviews file was monthly. Wow, it was! BBD use quarterly data because they wanted to look at the impact on GDP. If you are talking about more spikes than what I’ve got plotted, you must be referring to one of the subindices.

I’m well aware of the limitations of the BBD graph; many of these came out in a seminar they presented in Washington. That being said, I applaud their quantification of what is usually just hand-waved about — as exemplified in your comment. Sure, policy uncertainty exists, but even taking into account your pet bugaboo of PPACA, is it any higher than during the debt limit debate? Is that what you asserting? If so, I have a Phoenix Center study for you to read.

I am not sure how to view these ongoing efforts to explain the lack of inflation on Obamacare. It may in the end prove to be a mistake (although portions of it will certainly remain, such as forbidding private insurers from rejecting customers based on preexisting conditinos). But was not one of the supposed ills of the program its reputed high costss? Why are these not giving us more inflation rather than less?

Really, I think this effort is just pathetic. Get real, folks. Obamacare has its problems, but trying to blame our current creeping deflationary tendencies in the face of a large Fed balance sheet on it is simply ridiculous.

It’s a sluggish recovery, and that’s the only reason why inflation hasn’t exploded.

Or let’s say it’s about no recovery at all, as unemployment at 7,6 but above 9 if you take the employment population ratio into account, and Ben is well aware of that. But stocks are getting higher and higher, QE mission fully accomplished by Ben, great success story.

Menzie, do you really think that Ben cares about the state of the economy, are you kidding ? When will you realize that the USA is run by very wealthy criminals ?

Janet’s term will be interesting ! A great chance to make a lot of money. The people who pull the strings and let Janet dance, that’s the question …

Menzie

Gee, I didn’t realize the index only had 2 components, debt and the attrociously crafted ACA.

I’m just pointing out your bias for the wandering blog readers that happen by here and assume all your posts are unbiased.

Your welcome.

Pardon the typo.

You’re welcome.

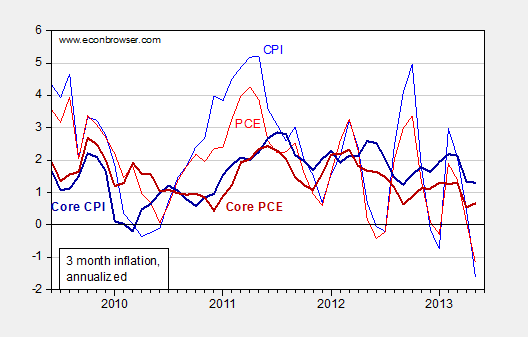

Note also that the situation looks even worse than Figure 1 suggests if you look at annualized inflation, which I believe provide a better look at medium-term inflation rather than the month-to-month noise.

The annualized Core PCE has been below 2% since 2008.

The other big question is why Ben Bernanke and the other Ph.D. economists on the Fed never learned that when unemployment is high and inflation is low and below target you are supposed to loosen monetary policy.

Apparently, Bernanke just learned a bunch of algebra at MIT, but missed a sign somewhere in his computation…

You could add to this too — not only is unemployment high, but forecasted future unemployment is high. Looking at employment instead of unemployment, the picture looks far worse. Not only is inflation low, but future forecast inflation is low. And not only are Bernanke and every Fed member, over half of whom are now Obama appointees, save James Bullard, getting things very, very wrong, but hardly any academic Macroeconomists even notice. And approximately 1 academic economist noticed in the spring of 2009.

Dan Kervick Without particularly agreeing with much of what you said (I think kharris covered it nicely), I will tip my hat to your lively and vivid writing. It was a pleasure.

tj What’s with you and Obamacare? Is Obamacare your own personal Moby Dick? Business uncertainty was and is primarily about aggregate demand, not Obamacare. And to the extent that healthcare was contributing to business uncertainty in 2009/2010, how much of that uncertainty was deliberately engineered by Team McConnell in order to make Obama a one term President?

You conveniently forget that CBO has studied Obamacare at least twice and both times found that it saves money over the status quo ante. So do businessmen ignore CBO reports and rely upon their own, vast and deep knowledge of healthcare economics? “We don’t need no stink’n MIT economists!” And while your heart bleeds for those poor small businesses, why don’t you celebrate the fact that healthcare costs for large firms that already provide health insurance will see their rates go down? During the Obamacare debate big businesses supported it because it offered some relief from the free rider problem.

As to the Teamster’s letter to Pelosi and Reid, apparently you are the only one who didn’t know that big unions opposed Obamacare because it penalized “Cadillac” healthcare programs, which meant a cut in benefits for many big unions.

Look, healthcare inflation is falling at a pretty remarkable rate. Now it is true that healthcare increases may have moderated a year or so before Obamacare became law, and it is true that slowing healthcare inflation is a global fact, but there are plenty of reasons to believe that Obamacare has contributed to healthcare disinflation. For example, hospitals agreed to reductions because of the mandate reducing the risk of uninsured patients showing up at the emergency room. And Obamacare funded the rationalization of medical records.

There are at least two competing explanations, consistent with the statements that were made, and the observations we have:

•The observers were ignorant of economics.

•The observers wished to whip up hysteria in order to prevent the Fed from undertaking expansionary policies

The second explanation begs the question as to why those observers would want to prevent the Fed from undertaking expansionary policies. Presumably it’s because they are concerned about inflation, which immediately takes us back to the first group of observers who opposed QE out of ignorance.

Who knows why Rep. Paul Ryan thinks what he thinks? Does he even think? What’s more perplexing is why economists like Martin Feldstein opposed QE. Now he should have known better. And surely by now he should have learned from his past mistakes. But for poor ol’ Martin it’s forever 1979, as it is for many conservatives. How sad to be forever trapped in the world of gas lines, disco music, leisure suits, gold chains and Carter inflation.

Do a little dance, make a little love.

Get down tonight, get down tonight.

I agree with the commenters who point out that this post shows yet again Menzie’s deep political biases.

A partisan will attempt to discredit a person/position he doesn’t agree with by laying out 2 explanations, something like

1) Either Ryan is ignorant

2) Or Ryan is willfully trying to stop the Fed from improving the economy

In other words, Ryan is stupid or venal. We don’t get a third alternative.

Of course, a non-partisan would realize that there is a third alternative: Ryan is promoting a reasonable position that is shared by prominent economists.

If you want to be non-partisan and provide the third alternative, you have to start by getting your facts straight. Ryan did not make the statement that Reuters quoted in Nov 2008 as Menzie asserted. He made it on Fox News Sunday on Nov 7, 2010, in the context of QE2.

The next step to representing a fair third alternative interpretation of Ryan’s remarks would be to give the reader the full context by posting the entire statement rather than rely on Reuter’s one sentence summary. The entire statement is here in 23:30 and 24:00

http://archive.org/details/FOXNEWS_20101107_230000_FOX_News_Sunday_With_Chris_Wallace#start/1410/end/1440

Here Ryan is making an argument about how the Fed has gotten involved in fiscal policy and should really not be involved in discretionary policy. The inflation risk that he is pointing to results from the need for the Fed to exit its unusual monetary policies. It’s a quick argument designed for Fox News Sunday.

Ryan’s argument from Fox News is restated more completely 3 weeks later in an editorial in IBD he published with Stanford economist John Taylor, available here:

http://news.investors.com/ibd-editorials-perspective/113010-555234-refocus-the-fed-on-price-stability-instead-of-bailing-out-fiscal-policy.htm?p=full

If you look at Ryan’s Fox News Sunday interview and the Ryan-Taylor editorial, you can see that they cover the same themes.

Ryan and Taylor’s argument about inflation, which many prominent economists have also made, is that the risk comes about from the need for the Fed to reverse the various QEs. The danger is, to quote Taylor-Ryan

“On the contrary, QE2 will create more economic uncertainty, stemming mainly from reasonable doubts over whether the Fed will know exactly when and how to contract its balance sheet after such an unprecedented expansion.

If the money created to finance these asset purchases is not withdrawn in an expedient and predictable manner, the Fed risks higher inflation and a depreciated currency. On the other hand, exiting these programs too abruptly would also disrupt the economy.”

We are not yet at the stage in which the Fed is reversing QE, so we can’t test whether Ryan’s inflationary fears will be realized. But the fact that inflation hasn’t accelerated yet is irrelevant to Ryan’s argument.

At any rate, a non-partisan would have stated Ryan’s position fairly.

2slugbaits,

I think you are confusing KC and the Sunshine Band with the Bee Gees. “Do a little dance…” was done in 1975 when Ford was President, not 1979.

Rick Stryker: As Zhou En-Lai said about the French Revolution, it’s too early to tell…

Well, there is some empirical evidence on QE and exits. Like the hideously traumatic hyper-inflationary experience in Japan during the mid-2000’s. As recounted here. Oops. Mebbe not. Or maybe America will be the exception that proves the rule — that would give a different cast to the phrase “American exceptionalism”.

Welcome back — I’ve been in need of a laugh!

Conservatives like Paul Ryan have become seduced by Irving Fisher and Milton Friedman. They have come to view, like most Keynesians, money as some entity that drives an economy.

The problem with all these views from Conservatives to Progressives, monetarists to Keynesians is that they have lost sight of the fact that money is a tool to facilitate production. In this thinking they engage in all kinds of fiscal error by erecting massive wedges to production as they confiscate the value of capital through taxation, regulation, and government spending.

In a productive economy massive increases in the money supply to produce inflation, but in an economy that is contracting because of government fiscal errors no amount of monetary manipulation will overcome the waste and destruction.

Think about it.

2slugs

“You conveniently forget that CBO has studied Obamacare at least twice and both times found that it saves money over the status quo ante.”

The CBO is never right. The CBO is never even close. The CBO study on Obamacare said it saved money over 10 years, but cost money over longer intervals. It is a wealth transfer from the young diverse poor to the rich old white people, and is therefore racist.

2slugs

Wrong on nearly every claim you make.

Business uncertainty was and is primarily about aggregate demand, not Obamacare.

AD uncertainty always exists. The incremental uncertainty that drives hiring rests squarely on Obama’s flawed policies.

So do businessmen ignore CBO reports and rely upon their own, vast and deep knowledge of healthcare economics?

Probably. They certainly realize that every few weeks Obama announces some key part of the law that will be changed, unenforced or delayed. (Did the CBO include these changes and those yet to come in their calculations?) Hmmm, that sounds like it might create uncertainty, no? “In 2013, so far, we’ve added 4 new part-time workers for every full-time worker entering the labor force, whereas last year the ratio was nearly 6 full-time workers for every part-time worker. In June, we lost 240,000 full-time jobs even as we gained 360,000 part-time jobs. ” http://www.forbes.com/sites/theapothecary/2013/07/17/the-devastating-obamacare-tax-on-low-income-workers-at-large-firms/

why don’t you celebrate the fact that healthcare costs for large firms that already provide health insurance will see their rates go down?

There are a number of studies on both sides. Rates may be higher than the no-ACA case. The ACA will fall apart if it can’t attract the young and healthy who have no incentive to join an exchange. (Adverse selection, the healthy will pay a tax of a few hundred dollars rather than a several thousand dollar premium, while the sick will pay the premium). Rates cannot do down in this case and/or will have to be offset by tax increases. So your claim is tenuous at best, with much uncertainty regarding the final outcome. There’s that word again.

As to the Teamster’s letter to Pelosi and Reid, apparently you are the only one who didn’t know that big unions opposed Obamacare because it penalized “Cadillac” healthcare programs, which meant a cut in benefits for many big unions.

By “opposed” you mean that unions were so upset with the ACA that they put forth a herculean effort to get Obama re-elected? The ACA solves the unfunded union health care liability by dumping union members into the exchange.

Look, healthcare inflation is falling at a pretty remarkable rate.

Now we’ve come full circle. Healthcare inflation is falling because Obama’s flawed policies have more people leaving the labor force than entering the pool of employed. Further, more jobs are part-time without benefits relative to the past. Therefore, Obama’s flawed policies are reducing the growth rate in the number of people demanding health insurance and the rate of price increase falls.

What’s with you and Obamacare?

I tend to think that when the federal government enacts the largest piece of social engineering in decades, that it should have bi-partisan support. It should also have the support of a majority of Americans. Obamacare has neither. How and Why did we end up with Obamacare if only one party was in favor of it, and the majority of Americans oppose it?

The physical economy has been hijacked by monetary policy and financial engineering

QE doesn’t produce any capital. It merely exchanges financial titles into new liquidity freshly created by central banks. As a result the cost of the existing debt positions are reduced, because interest rates are forced down. That’s all. All this new liquidity is chasing returns and overflows the capital markets, causing unsustainable bubbles in these markets.

The QE-policy shows that a final solvency problem cannot be solved by providing liquidity. Product markets do not benefit. We therefore do not see any significant economic growth and inflation in the real markets in Japan, Europe and the US. We only see speculation and asset inflation in capital markets.

This is, and remains, a debt-based monetary fiat system. It has finally reached the end of it’s super-debt-cycle. From now on it will turn from an inflationary momentum into a deflationary endphase, while growth disappears due to debt saturation. It is the monetary system itself stupid.

http://www.economie-macht-maatschappij.com/financiele-markten.html

Rick Stryker I see you’re back. Work release program for good behavior?

You’re right; the K.C. song was from 1975. But the BeeGee’s “Saturday Night Fever” was 1977. Neither one was from 1979. My point was (obviously) that 1979 was not only the peak (or nadir?) of disco, it also marks the far right’s dystopic view of liberalism. Conservatives only remember the oil shocks, gas lines, hostages, and stagflation. They tend to ignore those other years in the late 70s when real GDP was growing at 5%, unemployment was below the NAIRU, and budgets were almost balanced without benefit of FICA surpluses.

tj I’m wrong on almost all counts??? Time for a reality check. So your bizarre argument is that businesses are more concerned about supposed uncertainties in the ACA than they are uncertainties about their customer base? Really? You actually believe that? Second, unions supported Obama’s re-election…which was after ACA was law. So your comment is a non sequitur. Your comment about the Hoffa letter just proves that you were completely unaware of what Hoffa’s opposition was all about. You just winged it and it shows.

Healthcare inflation is falling because Obama’s flawed policies have more people leaving the labor force than entering the pool of employed.

Another non sequitur…this time followed by a factual error. Employment numbers are very slow, but employment numbers are growing faster than working age people are leaving the labor force. What’s happening in the labor market doesn’t have anything to do with Obamacare. The real story is that the recently unemployed are finding jobs at normal rates. The problem is with the long-term unemployed. And that is a problem that cannot be explained by some ridiculous appeal to Obamacare. That’s just dumb. As to the public not supporting Obamacare, this isn’t quite right either. The public supports all of the individual components of Obamacare. What they oppose is the whole package. This says more about the rationality of the American voter than it does Obamacare. It makes about as much sense as saying I like potato salad, and I like corn-on-the-cob, and I like BBQ ribs; but I don’t want the blue plate special with potato salad, corn-on-the-cob and BBQ ribs.

As a conservative you should be doing all you can to make Obamacare a success, because if it fails you’re really going to hate the alternative. The alternative will not be the world before Obamacare. The alternative to Obamacare will be a single-payer system through an expanded Medicare program. You need to set aside those reactionary fantasies you keep having.

Menzie,

That’s a mythical quote from Zhou En-lai. He was referring to 1968, not 1789.

Time will tell on the reversal of monetary policy. But I think it’s also worth mentioning that the issues that Taylor and Ryan bring up run deeper. Their concern is that the Fed has mixed monetary and fiscal policy. Another blogger that you may have heard of discussed the same concern in “Concerns About the Fed’s New Balance Sheet” in “The Road Ahead For the Fed.” In that essay, this blogger worries that the Fed risks loss of independence in its conduct of monetary policy and notes that this loss has always been a precursor to inflation problems.

2slugbaits,

I wasn’t talking about Saturday Night Fever. 1979 was the Bee Gees biggest year, with a no 1 album in both the US and UK.

What conservatives remember most about the late 1970s (besides the Carter administration’s foreign policy fiascos) was the accelerating inflation that ended in a severe double dip recession. Fortunately for us all, the Golden Age Of Conservatism that followed fixed the problems of the 1970s.

Rick Stryker: My cursory survey indicates that there is no consensus on the Zhou French Revolution quote; so it’s hardly decided. My impression is that the 1789 event is more consistent of Zhou’s sense of humor, but I will not claim to be an expert (despite having read extensively about this period).

I understand the worry that you mention. But as I say, there have been previous instances of doubling your money base, without the problems you attribute to Ryan. Indeed, the subtlety and nuance you attribute to him has been missing in almost all his other pronouncements on economic policy.

Menzie,

This FT article quotes people who were present when Zhou made the statement. They say he meant 1968. The article also mentions that Chinese archives confirm that he meant 1968.

http://www.ft.com/cms/s/0/74916db6-938d-11e0-922e-00144feab49a.html#axzz2ZMpsmDei

Maybe there wouldn’t be as much concern if we were talking about a doubling of the monetary base. But the monetary base has quadrupled.

Anonymous,

Great post!!!

2slugs

Ignoring your strawmen, your basic point is this: “What’s happening in the labor market doesn’t have anything to do with Obamacare.”

I’ll let reality speak for itself regarding Obamacare’s impact on the labor market. These cases involve local government, there are literally thousands of similar cases for business if you care to google.

Obamacare is a trainwreck. You’ve drank too much kool-aid.

http://news.investors.com/061913-660419-local-governments-cut-hours-to-avoid-obamacare-mandate.htm

Here is just a small sampling of local news reports about what local government officials are saying about ObamaCare, and the steps they’re taking to avoid or minimize its costs.

Phillipsburg, Kan.: “School administrators here say they are alarmed and confounded by the looming new costs they face with the implementation of the Affordable Care Act,” according to the Kaiser Health Institute News Service. Chris Hipp, director of a Kansas special education cooperative, warned that ObamaCare’s costs “could put us all out of business or change significantly how we do business,” adding that “we are not built to pay full health benefits for noncertified folks who work a little more than 1,000 hours a year.”

Dearborn, Mich.: “If we had to provide health care and other benefits to all of our employees, the burden on the city would be tremendous,” said Mayor John O’Reilly, explaining why the city is cutting its more than 700 part-time and seasonal workers down to 28 hours a week. “The city is like any private or public employer having to adjust to changes in the law.”

Indiana: “What I’m seeing across the state is school districts, unfortunately, having to reduce the hours that they are having some of their folks work, primarily so they don’t have to worry about the (ObamaCare) penalties, or they don’t have to provide them health insurance, which would be very, very costly,” said Dennis Costerison, executive director of the Indiana Association of School Business Officials. Ft. Wayne Community Schools, for example, are cutting yours for nearly three-quarters of its part-time aides.

Omaha, Neb.: “The biggest problem is everyone said that ObamaCare is only going to help cut costs. Nothing could be further from the truth,” said Mike Kennedy , who serves on the board of Millard Public Schools, just outside the city, and figures ObamaCare will raise its costs by $400,000. A neighboring school district is reducing hours for up to 281 part-time employees to avoid $2.5 million in new costs, which will result in pay cuts of up to $3,300.

Long Beach, Calif.: “We are in the same boat as many employers,” said Tom Modica, Long Beach’s director of government affairs. “We need to maintain the programs and service levels we have now.” So the city is going to cut hours for 200 part-time workers so it doesn’t have to pay $2 million to provide health benefits.

Salt Lake City: “With new provisions in the Affordable Care Act, there was going to be a significant burden upon Granite School District and our taxpayers to offset the cost of benefits,” said spokesman Ben Horsley. He says covering the district’s part-time workers would cost about $14 million, and so about 1,000 will have their hours cut to 29 a week.

Cape May County, N.J.: “A number of people in the nation who read it are recognizing how detrimental (ObamaCare is) to government and private employers out there,” said Gerald Thornton, the county’s finance director who is trying to figure out how to budget for the law.

Virginia: “The Commonwealth of Virginia is grappling with the same issues that many businesses in the private sector are as they struggle to deal with the costs imposed by the Affordable Care Act,” Paul Logan, a spokesman for Gov. McDonnell, said. The state is requiring that about 7,000 part-time government workers put in no more than 29 hours a week.

Texas: “The Affordable Care Act has added so much complexity and administrative burden that there is nothing affordable about it,” said Jared Pope, who is consulting with Texas municipal governments on ObamaCare. Dallas expects its health costs to climb $2.1 million next year. Plano is cutting hours to avoid $1 million in new costs.

Kern County, Calif.: “It will affect multiple departments, a majority of departments,” said the county’s deputy administrative officer Eric Nisbett, explaining that unless the county cut worker hours for 800 employees, ObamaCare would cost it up to $8 million a year.

Allegheny County, Pa.: “There’s frustration and anger and sadness and resentment, you know, but you don’t have a voice,” said adjunct English professor Clint Benjamin in the wake of the Community College of Allegheny County’s decision to cut hours for about 400 adjunct faculty and other employees so it wouldn’t have to pay $6 million in ObamaCare-related fees next year.

Medina, Ohio: “We feel bad as a city administration and as a council in having to cut hours from 35 to 29,” Medina Mayor Dennis Hanwell said. “We have the budget to pay the people, but we do not have the budget to pay for the health care.” If they hadn’t made that cut, the city faced up to $1 million in new health costs courtesy of ObamaCare.

Birmingham, Mich. Commissioner Gordon Rinschler may have summed up best the reaction that countless businesses and governments are having to ObamaCare, saying: “We simply can’t afford the Affordable Care Act.”

I have two comments for you

1. We are always fighting the last war. If you add to this the fact that government spending and taxing strongly influences jobs and wealth and that many so-called leading economists moonlight regularly for big finance, it’s not surprising that they are often wrong. There should be no Nobel prize for Economics.

I don’t know whether Ryan is stupid, but his admiration for Ayn Rand makes him a strong ideologue. The fact that he claims to be both Christian and a Rand follower says volumes.

2. Why not limit people to a single comment on each post? I find it depressing to read the drivel that many energetic commenters keep posting. Let them say their piece, limited to a reasonable number of words, maybe 300, and then chop them off. Reply to those that seem reasonable as you now do.

anon at july 17 at 1030 am— Great post.

TJ – no amout of reality will convince a hardcore lib like 2koolaids that Obamacare isn’t a great law.

tj I read a lot of crocodile tears in those stories. A lot of fishiness too. Hint: if you need “x” number of labor hours for core operations, it is very expensive to try and cover those hours with part-time workers. No rational business person does that. The costs of health insurance are trivial when compared with the training costs, the fixed costs and the higher reservation wage that part-time employees are able to demand. No doubt that some businesses will be hurt, but businesses that already provide health insurance to their employees will see their costs reduced. At worst Obamacare is a zero sum on jobs. One of the ways Obamacare reduces health insurance costs is by getting rid of the free rider problem. Why are you such a fan of deadbeats and free riders?

Oh…the other day there was a story about the huge drop in insurance premia set for New Yorkers in 2014:

http://www.nytimes.com/2013/07/17/health/health-plan-cost-for-new-yorkers-set-to-fall-50.html?pagewanted=2&_r=2

Stryker: When Zhou made the crack about the French Revolution, as I recall, there was a lot of overwrought hysteria in the western press about him ‘questioning the underpinnings of democracy.’ My impression was that the 1968 story emerged in the wake of that to provide ambiguity for PR cover in the western press.

Your argument assumes that the CPI captures accurate inflation information. That assumption is no sure thing.