Today, we’re fortunate to have Willem Thorbecke, Senior Fellow at Japan’s Research Institute of Economy, Trade and Industry (RIETI) as a guest contributor. The views expressed represent those of the author himself, and do not necessarily represent those of RIETI, or any other institutions the author is affiliated with.

On March 8th President Trump announced 10 percent tariffs on aluminum imports and 25 percent tariffs on steel imports. On April 2nd China retaliated by announcing tariffs of up to 25 percent on imports of pork, soybeans, and other products. The European Union is also considering retaliatory tariffs. This tit-for-tat conflict spawns uncertainty, raises prices of key inputs for downstream industries, forces companies to engage in time-consuming appeals to the government, and risks making American products toxic to hundreds of millions of nationalistic Chinese consumers. It is no wonder that Deardorff and Stern (1997) said that using tariffs to correct distortions is like performing acupuncture with a fork.

This is not to deny that the U.S. aluminum and iron & steel industries have suffered. Iron & steel employment dropped 71 percent between January 1992 and December 2016 and aluminum employment dropped 52 percent. Iron & steel stocks lost more than half of their value between the onset of the Global Financial Crisis and the end of 2016. Aluminum stocks lost more than three-quarters of their value over this period.

Investigating Trade Elasticities for Manufactured Goods

I recently investigated (Thorbecke, 2018) how exchange rates affect U.S. manufacturing sectors such as aluminum and iron & steel. Demand for the safety of U.S. Treasury securities and other dollar assets has strengthened the dollar and increased the U.S. current account deficit (see Caballero, Farhi, and Gourinchas, 2016). Currency manipulation may also have raised the dollar’s value and worsened the current account (see Bergsten and Gagnon, 2017). While these capital inflows allow Americans to consume more than they produce, the accompanying deficits cause dislocation for U.S. workers and industries.

Since safe asset demand and other factors keep the dollar stronger over time, I used a long run model called dynamic ordinary least squares (DOLS) to investigate how exchange rates and other factors affect U.S. manufacturing exports and imports over the 1992 to 2017 period. The goal was to obtain good estimates where possible rather than a large number of questionable estimates. Mead (2014) showed that the trade prices that the Bureau of Labor Statistics (BLS) collects from companies are superior to producer price indices or unit values for deflating trade statistics. The study thus examined those Harmonized System (HS) 2- and 4-digit categories of manufacturing imports and exports for which the BLS provides import and export price data. I tested for long run (cointegrating) relations between exports or imports and the real exchange rate and real GDP using the trace statistic and the maximum eigenvalue statistic and included those HS categories of exports or imports that exhibit cointegrating relations with the real exchange rate and real income.

In previous work, Chinn (2010) used DOLS techniques to estimate trade elasticities for U.S. exports and imports over the 1975Q1-2010Q1 period. In his baseline specification, he found an exchange rate elasticity of 0.6 and an income elasticity of 1.9 for goods exports excluding agriculture. For goods imports excluding oil he found an exchange rate elasticity of -0.45 and an income elasticity of 2.6. Chinn reported that estimating import functions is challenging. I found that when U.S. imports are disaggregated into those from China and those from other countries, most of the price elasticities are of the expected signs and many are statistically significant.

The results indicate that iron & steel and aluminum trade is sensitive to the exchange rate. A 10% stronger dollar would reduce steady state U.S. exports of iron & steel by 12% and of aluminum by 11%. A 10% stronger dollar would increase U.S. imports from China of iron & steel by 8% and of aluminum by 6%. It would also increase U.S. imports from the world ex-China of aluminum by 7%. Over the 1992-2017 sample period the U.S. ran a cumulative deficit of over $100 billion in aluminum trade and $200 billion in iron and steel trade. A weaker dollar would have generated lower deficits.

Motor vehicle trade is also responsive to the exchange rate. A 10% appreciation would reduce motor vehicle exports by 19% and increase imports by 6%. The automobile industry is competitive, with many close substitutes from different countries. This increases the price elasticity of demand for these products.

Calculating a weighted average of the export elasticities for all goods, with the weights based on the value of exports in each category relative to the value of exports in all the categories, the overall export elasticity equals -0.81. Performing the same calculation for imports, the import elasticity equals 0.34. The sum of the export and import elasticities thus exceeds one, implying that the Marshall-Lerner condition holds. Thus, for the goods investigated in the paper, a depreciation of the dollar would improve the trade balance.

Product Complexity and Price Elasticities

A product’s complexity should affect its price elasticity. Complex products have fewer substitutes, and producers of complex products should have more market power (see Arbatli and Hong, 2016). The results in the paper support this relationship, as exports of sophisticated products such as pharmaceuticals and organic chemicals are not affected by exchange rates while elasticities for imports of labor-intensive goods from China such as footwear, radios, sports equipment, and lamps are close to one or higher.

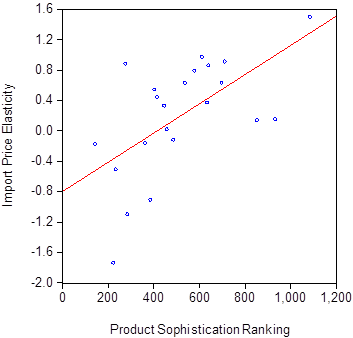

Hausmann and Hidalgo (2009) measured product complexity based on the number of countries that export a product and the economic complexity of those countries. As Figure 1 shows for U.S. imports from China, products that are more complex (i.e., have lower product sophistication rankings) according to Hausmann and Hidalgo’s measure tend to have lower exchange rate elasticities. The paper reports a similar relationship for U.S. exports.

Figure 1: The relationship between product complexity and import price elasticities for U.S. imports from China. Note: The figure shows the relationship between the product complexity ranking (PCR) for individual HS categories obtained from Hausmann et al. and the import price elasticities (IPE) for the same categories. The predicted relationship is positive. The line in the figure is from the following regression (with heteroscedasticity and autocorrelation consistent standard errors in parentheses):

IPE = -0.79 + 0.0019PCR

(0.49) (0.0008)

Adjusted R-squared = 0.336, Standard Error of Regression = 0.622

The Exchange Rate Exposure of Industry Stock Returns

Another way to examine how exchange rates affect manufacturing industries is to investigate how changes in the dollar affect stock returns for individual sectors. Theory posits that stock prices equal the expected present value of future net cash flows. Investigating how exchange rates affect sectoral stock returns can thus shed light on how industry profitability is affected.

I regressed monthly stock returns for a cross section of U.S. manufacturing industries on the Federal Reserve broad effective exchange rate and nine control variables. One of the control variables is the S&P Goldman Sachs Commodity Index. This index is a weighted average of the prices of industrial metals, precious metals, oil, and agricultural goods. This is an important variable to include because there is a strong relationship between the strength of the dollar and global commodity prices. For instance, since commodities are often priced in dollars, a depreciation of the dollar will increase the rest of the world’s ability to purchase commodities and thus raise commodity prices.

Aluminum stocks are the most exposed of any sector examined to the exchange rate. Returns on aluminum stocks fall by 1.15 percent in response to a 1 percent appreciation. Paper and forestry stocks are also exposed, with returns on paper & forestry stocks falling by 1.1 percent in response to a 1 percent appreciation. In addition, returns on nonferrous metal stocks fall by 0.78 percent and returns on iron & steel stocks fall by 0.60 percent in response to a 1 percent appreciation. Between June 2011 and the end of 2015 the dollar appreciated logarithmically by almost 30 percent. The results indicate that appreciations such as these can devastate the profitability of the aluminum, iron & steel, paper, and forestry sectors.

Motor vehicle stocks and footwear stocks are also exposed to the exchange rate, perhaps reflecting the sensitivity of exports and imports in these sectors to exchange rates. Pharmaceutical, medical equipment and biotechnology stocks are not exposed to the dollar. This could be because firms in these sophisticated, research-intensive industries possess market power.

In general, the results indicate that the manufacturing sector is harmed by a stronger dollar. Twenty-eight of the coefficients are negative and only six are positive. Of the negative coefficients, 13 are significant at at least the 10 percent level while of the positive coefficients only one is significant.

Forestalling Protectionism

U.S. manufacturing imbalances are driving protectionist pressures. In 1985, France, Germany, Japan, the U.K., and the U.S. deflected protectionist pressures by agreeing in the Plaza Accord to depreciate the dollar. If the dollar is overvalued now, the U.S. and its trading partners should consider negotiating a similar accord involving more countries. The U.S. should also agree to reduce its budget deficit, since Chinn (2017) and others have reported that fiscal policy influences current account imbalances. America’s trading partners could also lower the dollar by promoting other currencies such as the euro, the yen, and the renminbi as alternative reserve currencies (Freund, 2017). Finally, U.S. manufacturing firms can better weather foreign competition by producing technologically advanced products.

This post written by Willem Thorbecke.

Nice summary of the empirical impacts of dollar appreciation on various key sectors. He keeps talking about the impact of a 10% appreciation of the dollar so I decided to provide this link:

https://fred.stlouisfed.org/series/DTWEXM

We had a very significant appreciation of the dollar during the Clinton boom. We also saw a recent appreciation of the dollar. Of course the mother of all dollar appreciations was during the early Reagan years when the FED raised interest rates to offset the Reagan military build-up and massive tax cuts for the rich.

I raise this as Trump wants to run the same fiscal policy. And our Usual Suspects here think this is a very good thing.

As per usual, we are lucky that Menzie got such a great researcher and writer to post on “Econbrowser” and the regular readers get to benefit from Mr Thorbecke’s deep knowledge base. Menzie is good at getting the quality guests on the blog. Also I almost feel we owe you an apology for not having more responders/comments to such an insightful/educational post. I learned a lot, and that’s why I wanted to soak it in before I responded.

I tend to agree that one of the major ways America could improve the current accounts deficit situation is by getting its fiscal budget in order. But then America would have to take a hard/unpleasant look in the mirror on the fiscal budget, and it’s so much easier/funner to blame China, yes?? But I’m kinda biased ‘cuz I already held that anti-Reaganite view for many years now. A weaker dollar seems counterintuitive (in my mind) on a surface view. But maybe looking on a deeper level, maybe a weaker dollar, relative to other currencies, is at least worth a TRY, by a “Plaza Accord II” or a “Plaza Accord: Part Deux” or a “Plaza Accord: Empire Strikes Back” er, like, something.

Most Americans really have zero understanding of these issues, and the sad commenter response (i.e. the lack thereof) to this 3-star Michelin post by Mr Thorbecke is Exhibit A on why we have the VSG as the current inhabiter of the White House and the masochistic policies that we do. Maybe there’s a solution somewhere:

https://www.youtube.com/watch?v=pNxPX4qRlZ0