Robust GDP growth, employment rising on pace, perceived recession risk declining… as in this headline. The latest issue of the Economist has an article entitled Fears of recession have faded. But I’m reminded that Campbell Harvey, who wrote early papers on the subject of yield curve predictors, relies on the 5yr-3mo spread (for growth, not recession). And that implied specification signals 44% probability of recession in 2020M04.

From Bloomberg:

“My economic model is not just predicting economic recessions, it’s predicting economic growth,” Harvey said. “If you’re flat or you’re inverted it’s saying the same thing: growth will slow.”

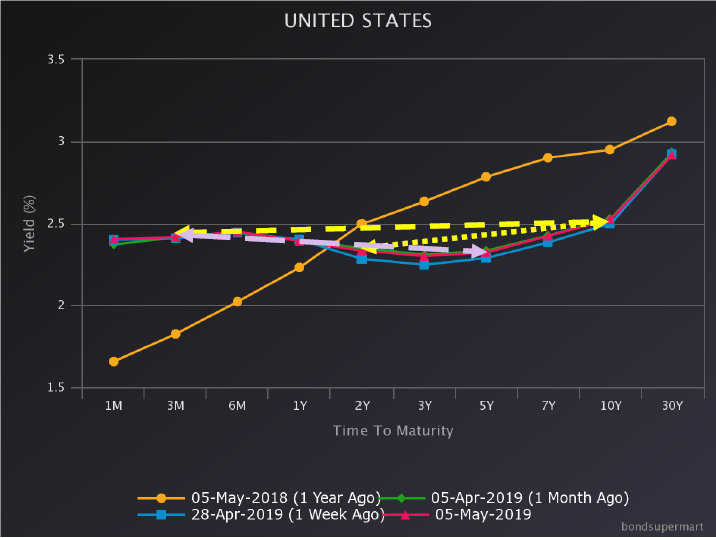

A snapshot of the yield curve Friday, a week earlier, a month earlier, and a year earlier:

Figure 1: Slope of 10yr-3mo curve (yellow dashed arrow), of 10yr-2yr curve (yellow dotted arrow), of 5yr-3mo curve (violet arrow).

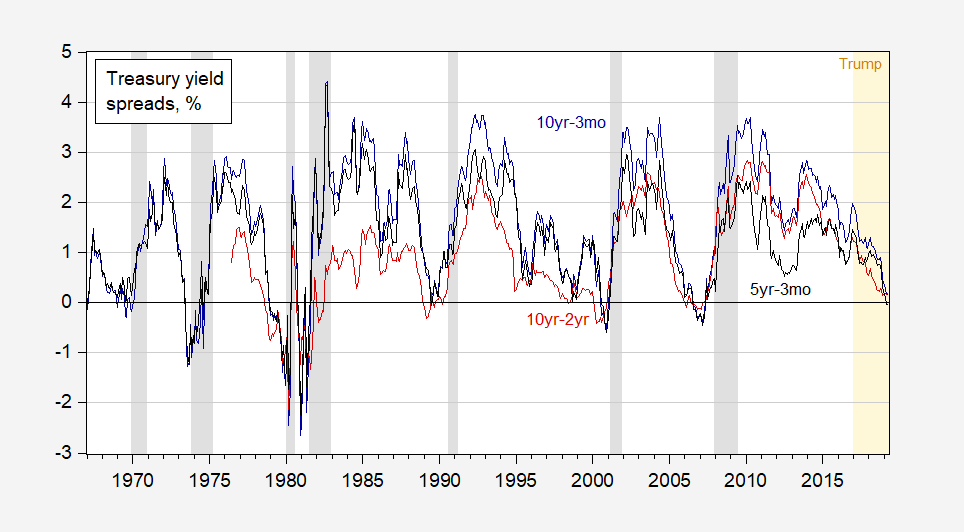

The 5yr-3mo spread, unlike other commonly used spreads, is inverted. The time series is quite informative.

Figure 1: Treasury 10 year minus 3 month spread (dark blue), 10 year minus 2 year (dark red), and 5 year minus 3 month (black). NBER defined recession dates shaded gray. Trump administration shaded orange. Source: Fed via FRED, NBER and author’s calculations.

The 5 year – 3 month spread is negative, just as it has been before each of the previous recessions. A detail is shown in Figure 2.

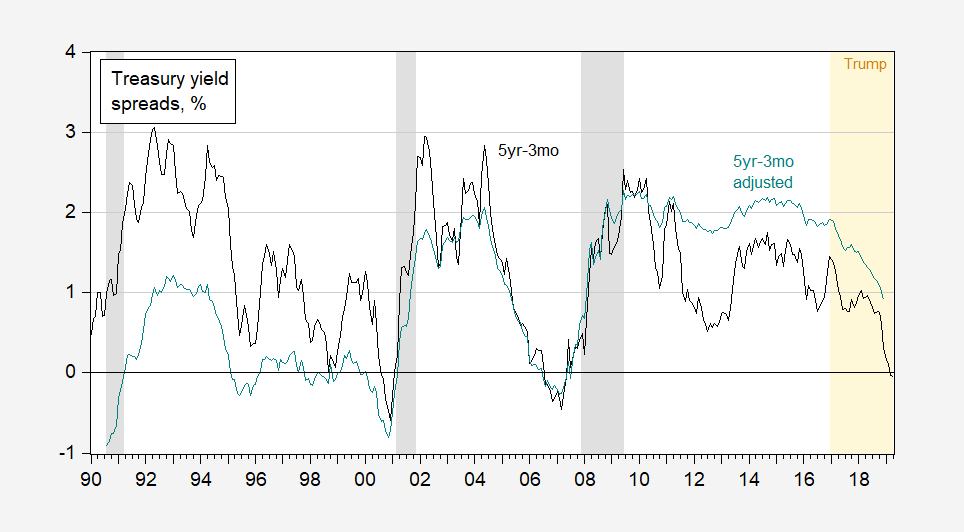

Figure 2: Treasury 5 year minus 3 month (black), and adjusted using Kim-Wright term premium on 5 year bonds. NBER defined recession dates shaded gray. Trump administration shaded orange. Source: Fed via FRED, NBER and author’s calculations.

Running a probit regression 1967M01-2019M04 yields:

Pr(recession=1) = –0.023 – 0.90x(gs5-tb3ms)

McFadden R2 = 0.31, N = 616. Bold figures denote significance at 5% msl.

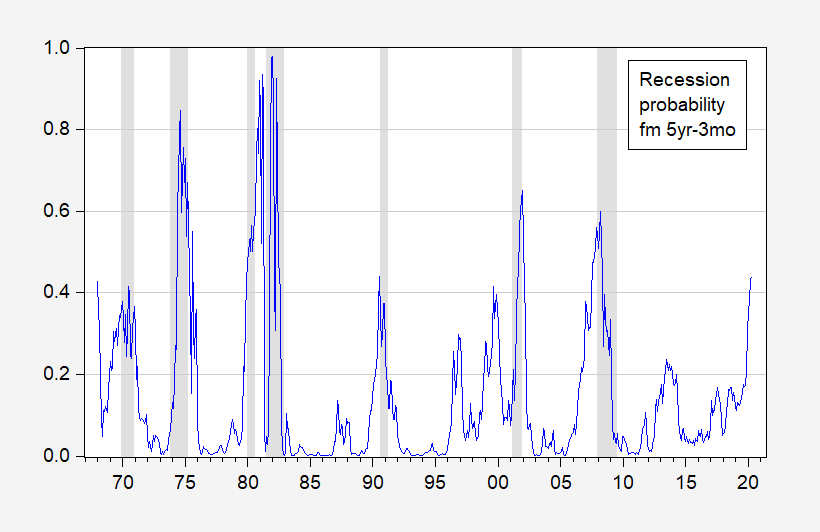

The implied regression probabilities for indicated months are shown in Figure 3 (i.e., the 2020M04 value is that predicted using 2019M04 spread):

Figure 3: Implied probability of recession using Harvey 5 year – 3 month spread lagged one year (blue). NBER defined recession dates shaded gray. Source: Author’s calculations.

While the probability as of 2019M04 is high, it’s not as high as at the outset of the 2007M12 recession (but is higher than that at the outset of the 2001M03 recession).

Some observers have argued that the distortions in long term bond market, due to large scale asset purchases, have rendered misleading the yield curve (see the discussion here). In order to address this, I adjust the spread by the term premium estimated for 5 year zero coupon bonds using the Kim-Wright method. This is shown as the teal line in Figure 2; in contrast to the 2006 period, the adjusted spread as of 2018M12 is higher than the unadjusted.

If indeed the pure expectations hypothesis of the term structure component is the predictive part, then the estimated probability of recession would be lower (quick estimate, 6% using data 1990-2019).

Paper on yield curve/growth here: Campbell Harvey (FAJ, 1989).

Forbes (your 1st link)? Like I consider those folks a reliable source! The 2nd link was from The Economist:

‘At the end of the year a model from economists at JPMorgan Chase had put the chances of a recession within 12 months, based on the s&p 500 index and corporate-credit spreads, at 65%. But the mood has now improved. By April 29th JPMorgan’s model was putting the chances of a recession at just 15%.’

One measure of credit spreads:

https://fred.stlouisfed.org/series/BAMLC0A4CBBB

Yea – this credit spread spiked at the end of 2018 but had come back down as of late. But we are talking about May of 2019 not the fall of 2020. Financial markets can change very quickly.

Just imagine putting the twin clueless clowns – Stephen Moore and Herman Cain – on the FED. If that had happened I’d bet the ranch we would have a recession in 2020.

I used to LOVE Forbes so much in my teenage years, roughly 1986–1990 timespan. They had some questionable editorial influences, but the old man’s commentary was still pretty good overall. I was socially-awkward, relating to neither anyone in my own family or my classmates, with very few if any friends (hard to imagine, eh??) and one of the big joys of my life at that time was pulling out the Forbes magazine, subscribed in my name, out of my parent’s mailbox. Or checking it out at the public library, Sometimes I think that and David Letterman at midnight is the only thing that kept me from slitting my wrists. For me, Forbes was like God’s mana. No, I didn’t believe everything the columnists (such as Caspar Weinberger) wrote, but I always read the old man’s (Malcolm Senior’s) views, which were nearly unceasingly humorous (in the best of ways) and thought provoking. When Senior died it put deep dread in me the magazine would never be the same. I wish in this case my perceptive abilities had failed. But, it is now largely garbage.

It was similar to WSJ many many years ago, you didn’t have to like/read the cr*p editorials to enjoy really solid journalism and writing. No more my friends, no more.

Interesting new paper:

The Aggregate Effects of Budget Stimulus: Evidence From the Large Fiscal Expansions Database

https://delong.typepad.com/large_fiscal_expansions.pdf

“This paper estimates the effects of fiscal stimulus on economic activity using a novel database on large fiscal expansions for 17 OECD countries for the period 1960-2006. The database is constructed by combining the standard statistical approach to identifying large shifts in fiscal policy with narrative evidence from contemporaneous policy documents to classify them according to their motivations. Using episodes that were not motivated by a desire to respond to prospective economic conditions, the paper finds large, persistent, and positive effects of fiscal stimulus on GDP with a decrease in net exports that only partly offsets the increase in private domestic demand. The paper also finds suggestive evidence that fiscal policy is more effective in a slump than in a boom.”

Let those last two sentences sink in as they are directly on point with respect to Trump’s fiscal stimulus. Their estimates suggest a lot of net export crowding out making the fiscal stimulus less effective.

When one compares the actual 3-month rates for 2006-07, they were decreasing in the second half of 2007, but still higher than current rates. Although 3-month rates in 2018 did increase, they have flattened since December. Do the absolute rates as well as the direction of change for the 3-month rates have any bearing on the model or an interpretation of the relationship?

Bruce Hall: Yes, in the Wright model. Doesn’t add to goodness-of-fit in my study with Kucko.

If we add the yield curve tightening to the fact Trump will not be able to increase the change in the structural deficit ( which is what matters for fiscal policy) then at worst a slowing economy appears a reasonable assumption in 2020.

@ Menzie

Menzie, I am not one of those super cool people who reads entire books on plane flights, or has paradigm shifting ideas every other day in the shower or from a dream. However I had a cool thought while half-awake this morning. OK, not a grand idea like someone had while thinking of what passengers see on a train when lightning strikes, but still a cool idea. I put a lot of thought in your MMT response, and how your “beef” with MMT related more to theory than to policy. Which I thought was a solid response. However I felt some level of personal ineptitude in not being able to give a reply, as some of the equation escaped, me, and I knew it would be at least months before I could know if there is even a good reply to your statement on the weakness of MMT theory. So this morning while very groggy I was reading Bill Mitchell’s blog and it hit me. “Why not put Menzie’s thoughts on the MMT to BIll Mitchell and see if he has a “retort” or just a kind reply??” Mitchell seems like a “blog friendly” type of dude, and chances are higher than 50/50 he would answer I think. No I haven’t asked or put a comment up on Mitchell’s blog yet, but plan on doing so before midnight tonight. As I view both of you as solid “gentlemanly” types, I thought it might prove fun. Or at least it might HALF answer the quandary. Maybe not your quandary, but mine.

This will not be done in “Nyaaa Nyaaa” spirit, but more like a return tennis shot from a friend, as I think that is how Bill Mitchell would take most of these things anyway. If he replies I will copy paste it and put on “Econbrowser” in the thread that seems most appropriate (which I imagine would just be whatever the most recent thread is)

Moses Herzog: Happy to have a response to my set of notes on MMT.

I just sent the comment off to Professor Mitchell, which actually I am happy about as some blogs don’t make it easy to comment, his seems similar to yours as it’s very user friendly.

Maybe you are hinting I should read your notes if I want the answer??—which is true. I need to read more on my own instead of taking the lazy way and expect people online to give me an answer—so I will plead guilty to that charge. Still, I thought it might be interesting to hear Prof Mitchell’s response or argument to something, that I have no doubt is a legit criticism—the fact that I am 100% certain you are correct and this is a legit criticism, I’m pretty certain you agree makes it all the more interesting question for an MMT disciple to answer.

I will be curious to see Mitchell’s reply. I have never visited his blog, but he is an intelligent and generally “gentlemanly” type, although he is Auatralian, vey much so, and not above calling people “shit for brains” and fuckwits” and “drognoes” and “pommies” and some other choice Ozzyisms when suitably provoked, although always with a twinkle in his eye.

“drongoes”, not “drognoes.” That one, although pretty unfamiliar to outsiders, is probably more insulting than the fits two, :-).

“than the first two” (“shit for brains” and “fuckwit”). “Pommie” is a more specialized insult neither you, Moses, nor Menzie, nor even me are going to be on the receiving end of. It refers to somebody from Great Britain, especially a pompous English person from UK who looks down their nose at Australians. It is derived from “POM,” but there is an ongoing debate over what that acronym stands for precisely, aside from that it refers to somebody out of UK. One of the theories is that is stands for “Prisoner Of Majesty,” but there are two or three other theories.

Oh, this is funny. Menzie has censored my reporting on certain Australian phrases I know Bill Mitchell likes to use I person (but probably doe not on his blog, which I have never read). I suspect Menzie is doing this out of diplomacy, although if he wants to avoid insulting Bill M., really Mrnzie, I know him very well and he would simply be amused, especially knowing it is coming from me.

However, for those of you left with this one apparently disconnected and weird post by me, I shall simply note that the colorful expressions I reported that Bill Mitchell occasionally likes use (he is Asutralian, and they are common there) include as part of them four letter Anglo-Saxon terms that used o be banned from the radio and TV, uh oh.

In any case, as I noted, in Australia,”drongoes,” is viewed as more insulting than those terms that include the naughty four letter words, but it is not easy to explain or translate to non-Australian English. But, it is plenty insulting. If an Australian calls you a “drongo,” they really have a low opinion of you, both intellectually and as a human being.

Barkley Rosser: Not censored, merely not approved yet. Now approved.

Mate not a lot us call people such names although drongo is not a swear word. A pommy is merely a person from the Old Dart i.e. the UK

NT,

I did not say “drongo” was a swear word. I said it was an insulting label. Would you be pleased as punch, mate, if someone you respected seriously called you a “drongo”?

Ah, I see now that my posts on Bill Mitchell’s pungent Australian phrases is showing up. He is an easy going guy, and as I said, when he delivers these zingers, he usually does so with a twinkle in his eyes. Really, the one where the twinkle might disappear is the much more serious “drongoes.” If you spend any time in OZ, you really do not want to have anybody deciding that you are a drongo. Not something admirable at all.

Doing my night owl thing while watching a documentary. Reading stuff interspersedly. The guy just knows how to spread joy to the masses doesn’t he?? https://www.bloomberg.com/news/articles/2019-05-06/with-two-tweets-trump-shatters-historic-calm-in-global-markets?srnd=premium-asia

We’ve had lots of dumbsh*t morons on this blog (NO, I am NOT just talking our “usual suspects” crowd, but people who count themselves in the more educated crowd, HINT: think southern hemisphere country locale commenters here, and others regularly commenting on this blog) who will absolutely insist and argue that there is no middle ground between a floating exchange rate and a pegged currency. WELCOME TO THE REAL G*DDAMNED F’ING WORLD FRIENDS:

https://www.cfr.org/blog/how-did-china-manage-its-currency-over-summer

https://www.cfr.org/blog/china-never-stopped-managing-its-trade

I am lazy as hell—-no doubt, one of the laziest on planet Earth—if I figured it out when I was in my late teens, some of you sorry people should be able to comprehend it when you’re a full grown adult blathering on a blog.

Has Bill McBride said anything one way or another? If he has, I missed it, even with reading his blog as close to daily as possible.

Willie: I doubt he has said anything more than the economy is right now growing strongly. Which is correct. Personally, I think the economy is as of 2019Q2 (1) growing (2) and above potential GDP (3) partly because of TCJA and the end of spending restraints and (4) strong global growth. None of these are inconsistent with reversion to full employment which (5) could entail a slowdown within the next two years.

He officially stated that he is not making any calls. That was an hour or three ago. He must have felt the waves of curiosity.

On the other hand, productivity is a great leading indicator and it is suggesting stronger growth over the next couple of quarters.

Professor Chinn,

You state, “If indeed the pure expectations hypothesis of the term structure component is the predictive part, then the estimated probability of recession would be lower (quick estimate, 6% using data 1990-2019).” Sure seems to be a big difference between 44% and 6%. Is there some further explanation that amateurs could understand to reconcile the difference? I, for one, am not familiar with how the pure rational expectations hypothesis… changes the model.

Thanks

AS: Use the estimated term premium to identify the EHTS component of the 5 year yield, and subtract from this the 3 month interest rate. Then do the usual probit regression (fit is much less pronounced, I think 15% McFadden R2), and forecast of probability. You get 6%.

Thanks!

Interesting…… I put the MMT query on Bill Mitchell’s blog yesterday, the site has been updated since then and about 6 more comments added. In fairness I sent the comment pretty late into the night, maybe 11pm?? I forgot now. Maybe he is putting some extra thought into it before he replies or somehow he got to the other comments before he saw mine. Like most professors he’s an extraordinarily busy person, travels sometimes for seminars, and I think is semi-politically active. Or maybe Professor Mitchell is giving me the subliminal message I think Menzie does in a friendly way sometimes: “Look and find it out on your own you lazy guy”

Moses,

11 PM in which time zone? Bill is in Newcastle, NSW, Australia most of the time.

JBR

@ Barkley Rosser

USA obviously. Yeah, that could be part of it. I’m not going to get upset. It could be he’s very busy or he feels it’s a question learners should search out on their own. Of course I will be pretty excited if he answers but I’m not going to mark it against him if he doesn’t.

It’s so funny the first time I listened to him, this would have been a few years ago, I first thought he was Scottish. I guess Australia is like Britain in they have the varying accents. I mean I knew that before but I couldn’t remember an Aussie that kinda sounded Scottish.

I think one central problem I think it’s hard to cut the interest rate “in real world” into three parts and estimate and talk about each one — you have to be right about every component to talk about each of them. For me one number is one number.

Only when one can cut in 2, 3, 4, … parts, do estimation and the results from each exercise are “consistent” with each other I think one can comfortably talk about one “component” of the number.

— Totally personal reflection; don’t call me Crazy. Never!!

Professor Chinn,

I read the FAJ article as I am always interested in forecasting models. I downloaded GNP data for the period that Professor Harvey used. My attempt to duplicate his results seemed to agree, given that most likely there were data revisions since his original work. I noticed that there were autocorrelation issues with the model and that the Theil U2 from a forecast was above 1.0. I also tried to update the model and found that I had to shorten the timeframe as opposed to using the data from Harvey’s original date. I also found that if I tried to account for the residual autocorrelations, the R-square improved, but the forecast still had a Theil U2 above 1.0. Thus, I am trying to determine how good the model is to forecast GNP or GDP growth. Did forecasters and modelers consider residual autocorrelation in the 1980s? I quickly tried to find when Theil developed the U2 statistic, but did not find the date. I know that EViews only started to include the U2 statistic within the past few years. Non of my questions are criticism, just curious about historical developments related to models and forecasting.