Debt-to-GDP dynamics are described by this expression.

(2) dt-dt-1 = [(rt-gt)/(1+gt)]× dt-1 – pt

Where d is the debt to GDP ratio, r is the real (inflation adjusted) interest rate, g is the growth rate of real GDP, and p is the primary (noninterest) surplus to GDP ratio. In words, the debt to GDP ratio rises when the real interest rate-growth rate gap is sufficiently positive, or the primary deficit is sufficiently large.

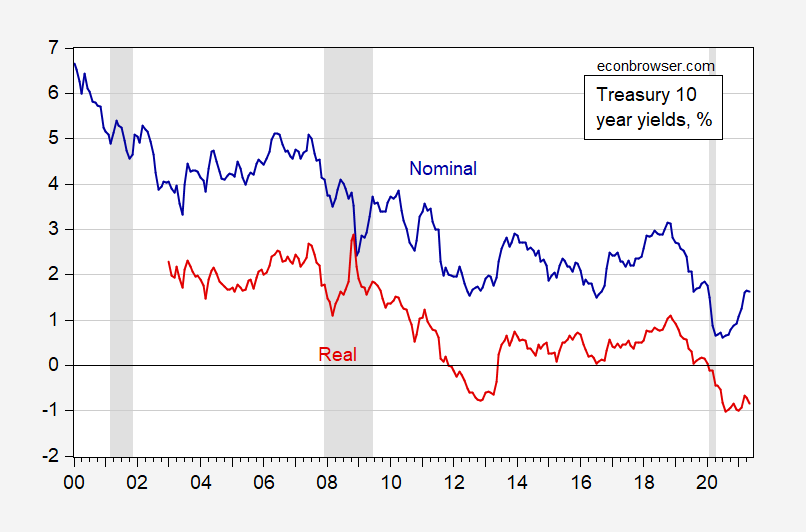

May 10 year TIPS was -0.85%. As of yesterday, that rate was -0.84%, and -0.05% for 30 year.

Figure 1: Nominal 10 year Treasury yield (blue), 10 year TIPS (red), both in %. NBER recession dates shaded gray; latest recession assumed to end 2020M04. Source: Federal Reserve via FRED, Treasury, and NBER.

Addendum (h/t Olivier Blanchard):

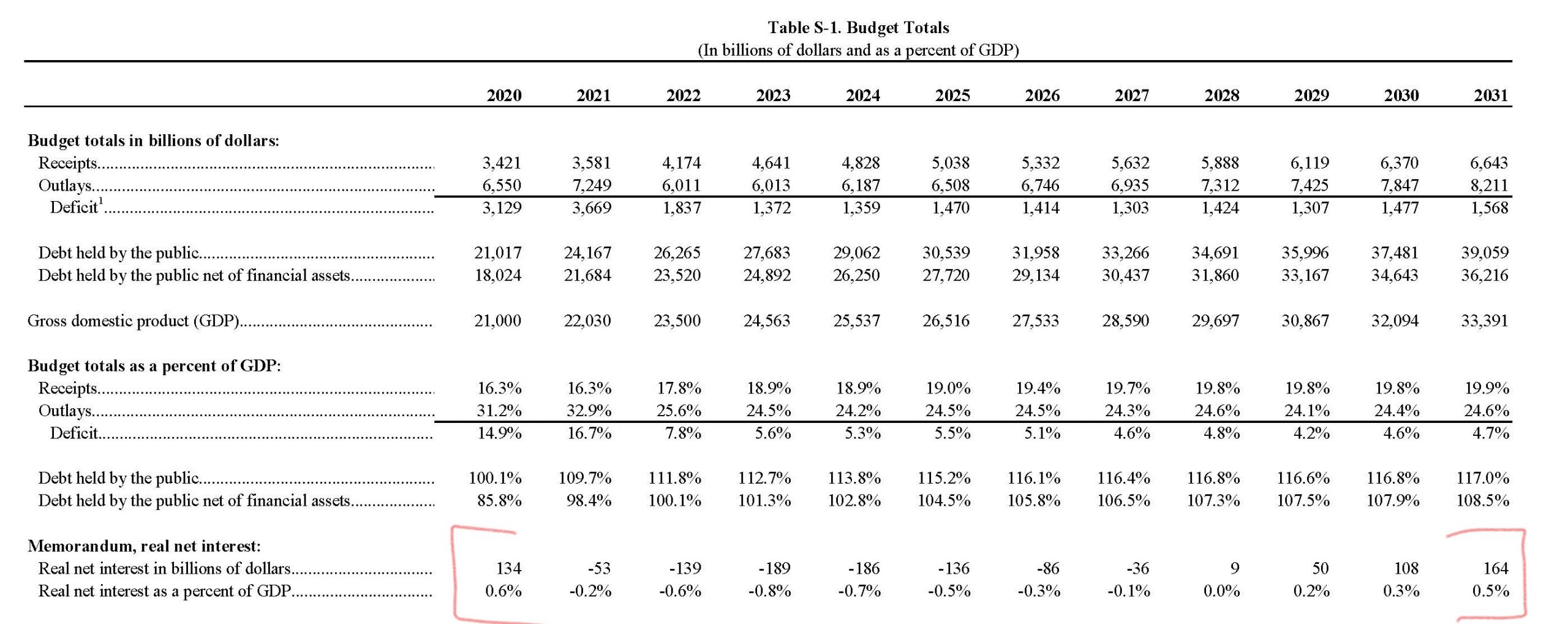

Real interest costs negative until FY2028.

Nicely put. I tried to answer macroduck’s question to which he claimed I added nothing to the conversation. I tried to note the literature on this from 40 years ago including Unpleasant Monetarist Arithmetic by Sargent and Wallace (1981) and he just got mad. Folks like Robert Barro, James Tobin, Willem Buiter, and Michael Darby accepts the basic analysis which actually dates back to Domar almost 80 years ago.

I hope he accepts this succinct answer with a wee bit of patience this time.

pgl,

Maybe. But recently he seems to take having somebody disagreeing with his economic analysis as a reason to turn into Moses Herzog Junior and have major fit. Once upon a time he was a pretty reasonable commentator here, but lately seems to have lost it. Too bad.

How dishonest of you. You and Barkley. You treat his comments section as if it is your own little sandbox. Shaw and Twain boy warned against dealing with pigs, and for some months I have ignored the two of you based on that good advice. You seem driven to defend your little sandbox. Childish.

In no way am I being dishonest. Barkley is right. You really need to take a chill pill.

macroduck,

Oh gag, you are totally destroying whatever credibility you might have once had. Oh, you have worked so hard to ignore me and pgl. But Moses Herzog Senior is far worse than either of us is. How hard have you had to work to ignore his disgusting and lying rantings? That is right, we know: you agree with them. If yo hang with someone like him, you end up with feces all over your face. Ugh.

So, sorry, you have no credibility. Might want to go to the nearest bathroom and wash your face off. It is kind of disgusting.

@ macroduck

I’ve always viewed dumb-and-dumber of Virginia and NYC as mostly a source of humor. Yeah, the making up of things, and then taking down of their own misrepresentations is annoying because some people won’t scroll up and therfore assume that what they said you said is actually what you said. But bottom line, people of intelligence will see through Barkley Junior’s and pgl’s desperate need to be recognized for anything. Some people even enjoy negative attention.

Next time Barkley or pgl take to manufacturing your prior comments, or making up from the ether formulations of questions you didn’t ask, just think of Hyacinth Bucket shoving Richard back from answering the phone, and how utterly sad she must be internally for continually creating an imaginary world in which she has higher status than everyone she interacts with:

https://www.youtube.com/watch?v=sjkFKY2pddc

https://www.youtube.com/watch?v=-pzRqc022tA

BTW that CBO analysis that Princeton Steve mocked laid out their estimates of the key parameters here. We asked Steve to actually read the analysis which made it assumptions crystal clear but I suspect Steve refused to do so.

Free Budweiser for getting vaccinated:

https://nypost.com/2021/06/02/biden-anheuser-busch-team-up-for-covid-vaccine-giveaway/

Now I got mine a while back and am not a Budweiser person. A good microbrew for me. But hey it is the MAGA hat wearers who are not getting vaccinated and this crew really loves its Budweiser. So maybe this will work!

Menzie, on the chance his this post is in response to my question in an earlier post, I will clarify my question to make sure it is the one you are answering.

You used the expression “lock in”. Treasury is often urged to refinance debt in order to “lock in” today’s borrowing cost. Treasury, of course, refinances some of its debt at all or nearly all of its auctions, so the point of this urging is to be Treasury to extend the average maturity of its borrowing. Yellen recently addressed the issue, saying no extension of average maturity is planned: http://www.reuters.com/article/us-usa-economy-yellen-bonds/yellen-says-no-plans-to-lengthen-maturity-of-u-s-treasury-issuance-idUSKBN2BF2LP

In fact, the average maturity of outstanding marketable Treasury debt was 69.2 months (very near the record high) as of the May 4 presentation to the TBAC, compared to an historical average of 60.1 months.

So, were you urging maturity extension, in disagreement with Yellen? You seemed to base you urging on expected continuation of low inflation. If inflation remains low, how does “locking in” help?

Oh, and how would debt-to-GDP dynamics inform a to lock in at longer maturities, where borrowing costs are higher?

macroduck: See previous comment.

md,

Yes, we get it. You doe not seem to understand the concept of real interest rates, having made it clear that nominal ones are all hat matter.

Mostly you actually are fairly reasonable and intelligent here, when you are not trying to channel you know who. But on this matter you have uncharacteristcally been making quite a fool of yourself, even though I agree that with multiple inflation measures out there there is no definitive measure of real intetest rates. But TIPS do reflect at least some fairly sophisticated market expectations on the matter.

As I read your opening there, the term money illusion came to mind. A term I have not thought of in so long I had to go here to remind myself how some define this illogical thinking:

https://www.investopedia.com/terms/m/money_illusion.asp

macroduck: I’m arguing for expanding amount of debt issued as TIPS, which locks in the real rate. Now whether it makes sense to move to issue more long term debt in nominal Treasurys is a separate issue. I would say it would’ve been a better idea to issue whatever debt issued last year as long term as possible. Whether the Trump Treasury did so, I don’t know.

You were clear. Macroduck has moved the goal posts. But hey – when I cited the literature on this topic, he says I’m being dishonest. Really?

The average maturity issue is a different issue from the nominal v. real issue. In fact, the average maturity issue needs to be thought of in terms of the Expectations Hypothesis. We could lock in a TIPS return = negative 1.8% on 5-year bonds or we could go 30-years but have to accept negative 0.05%. Of course the former risks the very real possibility that real rates five years from now will be higher. Which is the entire point behind the Expectations Hypothesis.

None of that changes macroduck’s confusion on nominal v. real which in a way is old fashion Money Illusion.

Interesting comments by Dr. Yellen. But she never said here or any where else that we should be focused on nominal interest rates v. real interest rates. That was your original challenge to our host but now we see you have moved the goal posts. And you accuse others of being dishonest? PLEASE!