Consumption rises as personal income ex-transfers fall in August, and monthly GDP rebounds somewhat. Consumption remains 2.8% above 2020M02 levels (the latest NBER peak). Here’s the picture of the macroeconomy (for some key indicators followed by the NBER’s BCDC).

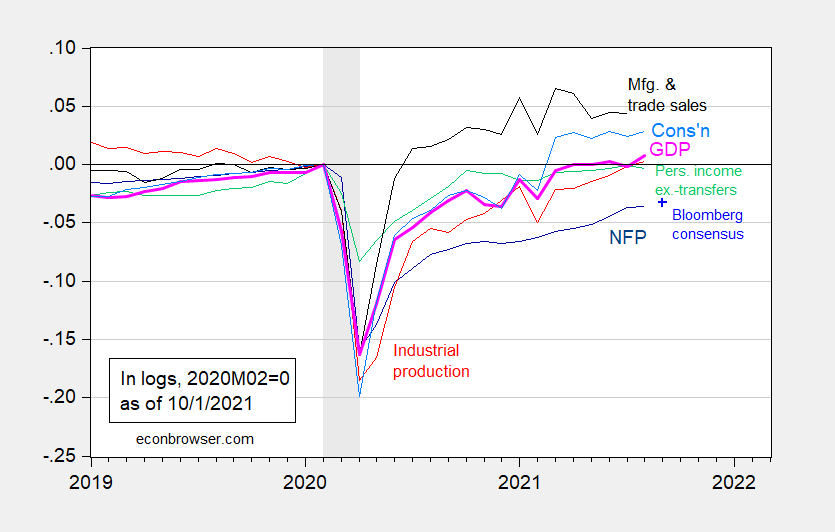

Figure 1: Nonfarm payroll employment from August release (dark blue), industrial production (red), personal income excluding transfers in Ch.2012$ (green), manufacturing and trade sales in Ch.2012$ (black), consumption in Ch.2012$ (light blue), and monthly GDP in Ch.2012$ (pink), all log normalized to 2020M02=0. NBER defined recession dates shaded gray. Source: BLS, Federal Reserve, BEA, via FRED, IHS Markit (nee Macroeconomic Advisers) (10/1/2021 release), NBER, and author’s calculations.

Combined with the consensus for September nonfarm payroll employment, recovery continues, but at a halting pace.

As of today, Q3 Nowcasts are 2.2% (IHS-MarkIt), 2.3% (Atlanta Fed), and 4.25% (Goldman Sachs).

https://cepr.net/was-the-gi-bill-of-rights-a-safety-net-bill-talking-about-the-democrats-big-bill/

October 1, 2021

Was the G.I. Bill of Rights a Safety Net Bill? Talking About the Democrats’ Big Bill

By DEAN BAKER

Many of us have been giving reporters grief about the constant reference to a $3.5 trillion spending bill (pre-Manchin), without pointing out that this is over ten years and would be just over 1.2 percent of projected GDP over this period. Also, the intention is to have the bill offset by tax increases and cuts in Medicare drug spending, so the net impact on the deficit would be close to zero. (That’s not my concern, just saying.)

We also need to give them grief on the other side of the picture. I doubt anyone likes generic government spending. On the other hand, most of the specific areas where the government does spend money, like Social Security, Medicare, and education, are very popular. So, describing the bill as simply “spending” is virtually certain to reduce support for it.

In recent days, reporters have taken to calling it a “safety net” bill. It’s not clear that is very much better. Most of us probably think of safety net programs as items like Temporary Assistance for Needy Families or food stamps, programs designed to help people who have fallen on hard times. Most of the proposed spending in the bill really does not have this character.

Much of it is quite explicitly designed to give people more skills and improve their prospects in the workforce. That is certainly the case with making community college free, universal pre-K, and the child care provisions. We know that quality child care leads to better outcomes for the children (as does pre-K), but it also makes it easier for parents of young children to work. The same is the case for the paid family leave provisions.

The child tax credit also fits in this category. By lifting millions of children out of poverty, it will also lead to better labor market and life outcomes when these kids get older. And, at least pre-Manchin, the benefit will be received by people in the upper middle-class. That makes it no more a safety net program than the dependent deduction on personal income taxes.

There are also provisions in the bill designed to increase the availability of housing. And, very importantly, the bill includes funding for moving away from fossil fuels and reducing greenhouse gas emissions.

The bill does include funding that increases access to Medicaid, as well as funding for increased subsidies for middle income people in the Obamacare exchanges, and improvements in Medicare. We can argue over the extent to which these are safety net programs, but most of this money will be going to people who are middle class.

In any case, the bulk of the bill really does not fit into the category of “safety net” spending. The GI Bill of Rights, passed during World War II, is probably a good comparison in this respect. The bill paid for World War II veterans’ college education, it also gave them low interest loans to buy houses (a benefit that largely excluded Black veterans because of discrimination in the lending and housing markets), and unemployment insurance.

That bill helped to give millions of veterans a path to the middle class, in addition to including the safety net provision of unemployment insurance. It is unlikely that many reporters at the time described the GI Bill of Rights as a “safety net” plan. They shouldn’t describe the Democrats’ package this way either.

https://www.nytimes.com/2021/10/01/business/stock-bond-real-estate-prices.html

October 1, 2021

Stock, Bond and Real Estate Prices Are All Uncomfortably High

An economist says the three major U.S. markets all show signs of severe overpricing.

By Robert J. Shiller

The prices of stocks, bonds and real estate, the three major asset classes in the United States, are all extremely high. In fact, the three have never been this overpriced simultaneously in modern history.

What we are experiencing isn’t caused by any single objective factor. It may be best explained as a result of a confluence of popular narratives that have together led to higher prices. Whether these markets will continue to rise over the short run is impossible to say.

Clearly, this is a time for investors to be cautious. Beyond that, it is largely beyond our powers to predict.

Consider this trifecta of high prices:

Stocks. Prices in the American market have been elevated for years, yet despite periodic interruptions, they have kept rising. A valuation measure that I helped create — the cyclically adjusted price earnings (CAPE) ratio — today is 37.1, the second highest it has been since my data begin in 1881. The average CAPE since 1881 is only 17.2. The ratio (defined as the real share price divided by the 10-year average of real earnings per share) peaked at 44.2 in December 1999, just before the collapse of the millennium stock market boom.

Bonds. The 10-year Treasury yield has been on a downtrend for 40 years, hitting a low of 0.52 percent in August 2020. Because bond prices and yields move in opposite directions, that implies a record high for bond prices as well. The yield is still low, and prices, on a historical basis, remain quite high.

Real estate. The S&P/CoreLogic/Case-Shiller National Home Price Index, which I helped develop, rose 17.7 percent, after correcting for inflation, in the year that ended in July. That’s the highest 12-month increase since these data begin in 1975. By this measure, real home prices nationally have gone up 71 percent since February 2012. Prices this high provide a strong incentive to build more houses — which could be expected eventually to bring prices down. The price-to-construction cost ratio (using the Engineering News Record Building Cost Index) is only slightly below the high reached at the peak of the housing bubble, just before the Great Recession of 2007-9.

There are many popular explanations for these prices, but none, in itself, is adequate….

Robert J. Shiller is Sterling Professor of Economics at Yale.

ltr,

Needless to say, at least real estate prices in PRC are also uncomfottably high, with a recent sale in Guaungzhou having only half the lots sold. Obviously a major adjustment is now in progress with the workout from whatever is going to happen with the failing Evergrande.

But the Chinese people get to have a distraction in the form of multiple days in a row massive air incursions by PRC militaty planes into Taiewanese air space. But we know that is just fine with you. That pesky Taiwan needs to be put in its place and brought down to the level people are in PRC by a nice rip-roaring conquest, tight? since they just do not seem willing to accept rule from Beijing, those naughty Taiwanese, tsk tsk.

“The State Department said on Sunday that the U.S. is “very concerned” about China’s “provocative military activity near Taiwan” following Beijing’s most recent show of air power near the self-governing island.

On Friday, China flew 38 military aircraft into Taiwan’s Air Defense Identification Zone, believed to be Beijing’s largest military provocation seen yet.

On Saturday, it sent 30 warplanes toward Taiwan.”

Is Xi getting ready to roll the dice? Increasingly looks like it.

https://thehill.com/policy/defense/575054-us-very-concerned-about-chinas-provocative-military

https://www.nytimes.com/2021/10/01/opinion/puerto-rico-jones-act.html

October 1, 2021

How the U.S. Dictates What Puerto Rico Eats

By Israel Meléndez Ayala and Alicia Kennedy

Photographs by Damon Winter

SAN JUAN, P.R. — In 1953, the Visitors Bureau of the Commonwealth of Puerto Rico released a promotional film to entice visitors called “Fiesta Island.” The island and its people are presented as exotic oddities, reflecting the colonialist attitudes of the era, and one gets the impression that Puerto Ricans desire nothing more than to serve American tourists.

But what is most striking is how prominently the local agriculture is featured. We are treated to images of sugar cane being chopped down to be turned into molasses for rum, fields of pineapples being harvested, bananas growing in the Yunque rainforest.

Yet today, even with a tropical climate that allows farmers to grow food year-round, Puerto Rico imports over 80 percent of its food.

You can sometimes find local produce, eggs, cheese and meat at the small farmers markets that have begun to pop up; grocery stores also carry a smattering of locally grown items like cilantro, recao, ají dulce and eggplant. But these aren’t the building blocks of a well-rounded diet. They’re not even all the ingredients in sofrito, the base for many Puerto Rican dishes.

“Today we have an economic model of consumption,” said Eliezer Molina, a Maricao-based farmer who ran for governor in the last election. “The United States doesn’t want to encourage the growth of production in Puerto Rico, because what we consume is from their producers, and that gives their companies protection.” …

President Bill Clinton made a mistake in pushing Haiti to remove a tariff against Arkansas rice imports. Removing the tariff resulted in rice imports ruining small Haitian farmers and making a country that could easily feed itself quickly dependent on food imports. Mr. Clinton would apologize for the mistake. Evidently the same mistake was made in Puerto Rico, an American island that should easily be able to feed itself was made dependent on mainland food import.

https://twitter.com/OVargas52?ref_src=twsrc%5Egoogle%7Ctwcamp%5Eserp%7Ctwgr%5Eauthor

September 30, 2021

Kawsachun News @KawsachunNews

Bolivia has a chain of state-owned supermarkets. They only sell locally-made produce and at lower prices than private stores. *

https://twitter.com/i/status/1443724103127556099

* Income is used to fudn infrastructure projects.

A less rosy analysis of how the economy is doing: “ Before taking inflation into account, personal income from all sources – from wages, interest, dividends, rental income, transfer payments such as unemployment compensation, stimulus checks, and Social Security benefits, etc. – rose by 0.2% in August from July.

But after taking inflation into account, it’s uglier: Inflation-adjusted – or “real” – personal income fell by 0.2% in August from July, to an annual rate of $17.8 trillion (in 2012 dollars), according to the Bureau of Economic Analysis on Friday.”

https://www.nakedcapitalism.com/2021/10/incomes-got-chewed-up-by-inflation-americans-spent-heroically-on-goods-but-not-on-services-eviction-moratoriums-forbearance-implicated.html

Miraculously, American consumers kept on spending.

https://fred.stlouisfed.org/graph/?g=FLue

January 15, 2020

Personal Consumption Expenditures price index less food & energy, PCE services and PCE goods, 2020-2021

(Percent change)

https://fred.stlouisfed.org/graph/?g=FMwl

January 15, 2020

Real Personal Consumption Expenditures for durable goods and services, 2020-2021

(Indexed to 2020)

Yves has some nice graphs with the first one showing what has happened to personal income adjusted for inflation. Yea – this is one noisy series but his graph clearly shows real personal income is higher than it was before the pandemic.

Now will it keep rising or retreat? I’m not exactly the best forecasting but neither is JohnH. Heck – he cannot even manage to honestly present the history of this series even if those wonderful graphs from Yves do.

Even FRED agrees with that graph from Yves that JohnH could not admit to us about:

https://fred.stlouisfed.org/series/RPI

Real personal income as of Feb. 2020 – just over $17.1 billion (2012$)

Same figure as of August 2021 – just over $17.8 billion (2012$)

At some point – maybe our host will insist that JohnH actually be honest here. GEESH!

https://fred.stlouisfed.org/graph/?g=FSAy

January 30, 2020

Real personal income and consumption spending, 2020-2021

(Percent change)

https://fred.stlouisfed.org/graph/?g=FSAC

January 30, 2020

Real personal income and consumption spending, 2020-2021

(Indexed to 2020)

Real personal income is up 4.1% and consumption is up 2.9%. So if one actually gets either the Friedman permanent income hypothesis or the Ando-Modigliani life cycle model then one is not surprised that the short term noise has not deterred consumption.

Thanks for the graph there! Of course we are doing actual economics which people like JohnH abhors.

“Miraculously, American consumers kept on spending.”

Johnny, you have again provided evidence that you aren’t qualified to have opinions about economics. People spend out of income above all else. Falling real incomes in no way discourage spending. Nobody thinks to themselves “My real income is falling, so I’m gonna starve myself.” In fact, the theory is that they spend faster in order to hold something which does not lose value as fast as money does.

Mostly, people save as their real income rises, not as it falls.

Please, please, please, stop lecturing about economics. You are just not well enough informed to avoid embarrassing yourself.

Who has March 2022 for the COVID-19 Great Depression in the office pool?

https://openknowledge.worldbank.org/bitstream/handle/10986/36295/9781464817991.pdf

October, 2021

World Bank East Asia and Pacific Economic Update

Executive Summary

The East Asia and Pacific (EAP) region is suffering a reversal of fortune. In 2020, many EAP countries successfully contained COVID-19 and economic activity swiftly revived as other regions struggled with the pandemic and economic recession. Now the region is being hit hard by the COVID-19 Delta variant while many advanced economies are on the path to economic recovery.

The disease is damaging the economy and is unlikely to disappear in the foreseeable future. In the near term, the persistence of the pandemic will prolong human and economic distress unless individuals and firms can adapt. In the longer term, COVID-19 will reduce growth and increase inequality unless the scars are remedied and the opportunities grasped. Policy action must help economic agents to adjust today and make choices that avert deceleration and disparity tomorrow.

What Is Happening Now?

The uneven recovery in the EAP region is now facing a setback. China is projected to grow at 8.5 percent in 2021, though growth momentum has eased. Overall regional growth is projected at 7.5 percent, reflecting the scale of China’s economy. The rest of the region is anticipated to grow by 2.5 percent, compared to 4.4 percent forecast in our April update, with significant heterogeneity across countries. While China, Indonesia, and Vietnam have already surpassed pre-pandemic levels of output, Cambodia, Malaysia, and Mongolia will only do so in 2022, and the Philippines, Thailand, and many Pacific Islands will remain below pre-pandemic levels of output even in 2023.

As a result, employment has declined, poverty will persist and inequality is increasing across several dimensions. Regional employment rate dropped by about 2 percentage points on average between 2019 and 2020. As many as 24 million people will not be able to escape poverty in 2021 in developing EAP, excluding China, because of COVID-19. While all households have suffered, poorer ones were more likely to lose income, sell off productive assets, suffer food insecurity, and lose schooling for children.

Why?

Restrictions to contain COVID-19 are constraining economic activity. Testing-tracing-isolation, a successful strategy in 2020, has been less effective against the more infectious Delta variant. Vaccinations, which would have helped reduce mortality and transmission, have been slow. Therefore, governments have been forced to impose restrictions to stop the spread of the virus. In general, economic disruption has been less in countries with higher vaccination. A 10 percentage point higher vaccination coverage was associated with a one-half of a percentage point higher quarterly gross domestic product (GDP) growth.

Constraints on vaccination differ for countries in the region. Availability held back vaccination rates in larger countries like Indonesia, the Philippines, and Vietnam. Smaller, poorer countries, such as some of the Pacific islands, benefited from vaccine donations, but some are constrained by limited distribution infrastructure. In several countries, as vaccination levels increase, hesitancy is likely to be a constraint.

Two factors have softened the consequences of the present outbreak. First, domestic economic activity has so far been less sensitive to infections. One additional case per one thousand reduced industrial production by an average of 5 percent in May 2020 but had a negligible effect in June 2021. Second, the buoyant external environment has helped to sustain regional exports. In August 2021, China’s merchandise exports increased by 31 percent in value terms over 2019-Q4 and those of other EAP countries by 21 percent….

real PCE for July was at 13,633.3 billion, and for August it was at 13,691.0 billion (CH12$, SAAR)…2nd quarter PCE was at 13,665.6 billion in chained 2012 dollars…hence, 3rd quarter real PCE has shrunk at a 0.10% annual rate for the two months of the 3rd quarter that we have data for….to get 3rd quarter real PCE to the +4.0% level indicated by some 3rd quarter GDP forecasts, September real PCE would need to grow 2.8% from August…

conversely, a 0.2% decrease in September’s real PCE would leave quarterly PCE slightly negative, and make for a difficult GDP report….while i can imagine inventories adding a couple percentage points (just by reversing their Q2 decrease), the rest of it may net out to zero…so while 3rd quarter GDP may print +2.0% or more, it’s conceivable that real final sales of domestic product could be negative…