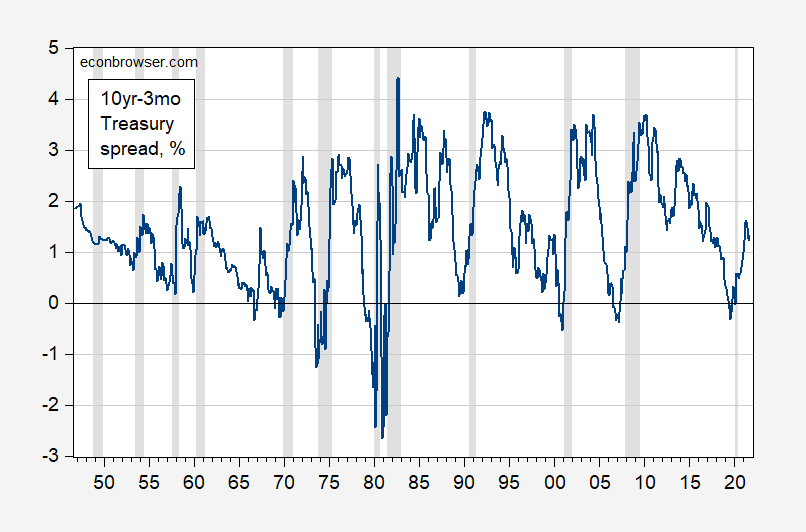

For the past 50 years, inversion has preceded recession.

Figure 1: Ten year-three month Treasury spread, % (blue). Three month is secondary market yield. NBER defined recession dates shaded gray. Source: Federal Reserve via FRED, NBER, and author’s calculations.

The 1989 near inversion is the sole exception (false negative), although the 10yr-2yr does invert then. (Updating for my undergrad course — see notes here.)

So if the US does go into a recession in the near future (as posited by this article), then this will be another case of a false negative reading from the 10yr-3mo spread.

Well, it got very close in 89, certainly took a steep dive then.

OTOH, there was a brief negative in 66 or thereabouts with no recession.

From the referenced article: “This historical correlation does not amount to a guarantee that another recession will begin within the next 12 months, needless to say. But I challenge you to study the accompanying chart and not be concerned.” This Dem administration is doing outstanding service for the University of Michigan’s Consumer Sentiment Survey (UMI) and the Conference Board’s Consumer Confidence Index (CCI).

I am not concerned. Maybe in 5 year? 8 years??? I care less about consumer surveys.

By the author’s own admission – his fluff piece is a worthless rant!

It’s essentially a “just asking questions” kind of article.

So what are the credentials of Mark Hulbert? Let’s see he got a degree in philosophy from Haverford College (think the kids of very rich people) and has been writing all sorts of investment advice BS for 40 years. Not exactly on par with Albert Ando and Franco Modigliani.

https://www.nytimes.com/2021/10/04/opinion/budget-deficits-climate-child-poverty.html

October 4, 2021

On Very Serious People, Climate and Children

By Paul Krugman

Do you remember the days of the Simpson-Bowles debt-reduction plan?

A decade ago elite opinion was obsessed with the supposed need for immediate action on budget deficits. This consensus among what I used to call Very Serious People was so strong that as Ezra Klein, now a New York Times Opinion writer, wrote, deficits somehow became an issue to which “the rules of reportorial neutrality don’t apply.”

The news media more or less openly rooted not just for deficit reduction in general, but in particular for “entitlement reform,” a.k.a. cuts in future Medicare and Social Security benefits. Such cuts, everyone who mattered seemed to argue, were essential to secure the nation’s future.

They weren’t. But here’s my question: If elite opinion cares so much about the future, why isn’t there any comparable consensus now about the need for climate action and spending on children? These are two of the main components of President Biden’s Build Back Better agenda, and the case for both is much stronger than the case for entitlement cuts ever was.

Yet whereas calling for Social Security cuts used to be treated as a sort of political badge of seriousness, calling for urgent action on climate and children isn’t. If anything, much reporting on current politics seems to suggest that the handful of Democrats trying to dismantle Build Back Better, to limit the Biden agenda to modest spending on conventional infrastructure, are being responsible, while the progressives trying to make sure that we really do invest in the nation’s future are somehow unserious.

Let’s talk about what securing the future really means….

Plus, it will cost $0!

Do you remember November 9, 2016, “If the question is when markets will recover, a first-pass answer is never.”?

Hey Billy Boy Bob Joe or whatever your real name is. No one knows WTF you are talking about and even less care.

Evidently, you care enough to vent your spleen.

Otherwise, I can’t help you.

” for climate action and spending on children? “……

it is appeal to unverified, unvalidated, unaccredited models……

climate is a religion no different than the covidian.

while investing in the children is a failure since the great society.

more religious zeal, with faith based measures.

zero carbon is the energy version of zero covid carzies the past 19 months.

You forgot to tell us which planet the Greys come from and when the NFL will be exposed as a front for the Illuminati. You seem to know everything, so why stopwiy just the easy stuff. Where’s Jimmy Hoffa buried?

TRUTH

It’s Springtime in Antarctica (the continent around The South Pole, Democrats) and this past winter (our summer, lefties) was the coldest on record since the previous record lows in 1976, when the all lovely people forecasted an ice age and the World running out of oil.

Quoted on Never Yet Melted blog, “How do you brainwash the poorly-scientifically-informed masses into accepting claims of imminent climate catastrophe for which we are all to blame by indulging in the various comforts and conveniences served up by modern industrial civilization?

“You do it by subjecting them to a continual barrage of entirely suppositious scare stories alluding to an endless series of untoward consequences that may, perhaps, possibly, arrive very soon if you fail to bow to the Luddite dismantle-modern-life-and-go-back-to-the-Middle-Ages agenda and surrender vastly more money and regulatory authority to International Statism.”

And, it takes a nation of productive families [not a village] to end childhood poverty, and not a trillion dollars divvied up by a bunch of failed public school teachers, K Street lobbyists, and 16,000+ politicians/bag men.

Please, productive families created by international statism. When debt liquidation occurs, those families will be bankrupt, just like the state.

T. Shaw,

TRUTH

Global average temperature still at near record highs despite the record cold in parts of Antactica. It is always the case that there is an uneven change in temperature going on, with some places cooling off even as the overall average increases.

Or did you not know that, R.S.? Apparently not.

Please, faith based what???? International capitalism can’t even exist without statism. Statism is free market ideology. Yes sir, carbon 0 burning is impossible but heavily reduced carbon burning is desirable. Reducing fossil fuel pollution raises testosterone. Which your lacking obviously.

https://www.nytimes.com/2021/10/05/business/germany-economy.html

October 5, 2021

Fears of a ‘Bottleneck Recession’: How Shortages Are Hurting Germany

Europe’s largest economy is particularly vulnerable to shortages of key parts and raw materials because of its dependence on exports.

By Jack Ewing

FRANKFURT — In Germany, where one in four jobs depends on exports, the crisis gumming up the world’s supply chains is weighing heavily on the economy, which is Europe’s largest and a linchpin to global commerce.

Recent surveys and data point to a sharp slowdown of the German manufacturing powerhouse, and economists have begun to predict a “bottleneck recession.”

Almost everything that German factories need to operate is in short supply, not just computer chips but also plywood, copper, aluminum, plastics and raw materials like cobalt, lithium, nickel and graphite, which are crucial ingredients of electric car batteries….

Apparently, market participants move funds into longer term, [perceived] risk-free assets when they expect ‘bad times.’

Considering Fed massive quantitative easing [to keep long rates low] since late 2008, consistent [except for 2017 and 2018] suppression of short rates targets at 0 – 0.25%, and COVID-19 [March 2020 the 10 year intra-day rate was 0.32%] crisis reactions, can we question whether the recent data to long term comparisons are valid?

T.S.

Probably more important most of the time has been that these changes have reflected tightening of Fed monetary policy, which tends to impact shorter term rates more than longer term ones. So these plunges reflect mostly rising short term rates due to Fed open market operatoins.

The one time we saw a negative premium but no recession, back in 1966, indeed the Fed was tightening, unhappy with the highly stimulative fiscal policy of LBJ who was fighting both a war on poverty and one in Vietnam. But his large fiscal stimulus was so great that it kept the economy from going into a recession due to the tightened monetary policy.

his large fiscal stimulus was so great that it kept the economy from going into a recession due to the tightened monetary policy.

Then again, LBJ did propose (and later enact) a contractionary surtax in early 1967 that somewhat offset his guns-AND-butter policies.

That quote got the history backwards. In Dec. 1965, LBJ’s CEA warned him that the triple fiscal stimulus (tax cut, Great Society, and Vietnam War) had gotten so big it would drive up inflation unless the FED raised interest rates. LBJ told them he would not cut government spending in 1966 so the only fiscal option was to raise taxes.

Of course supply side liars have been misrepresenting this era ever since so why not this half baked discussion?

“contractionary surtax in early 1967 that somewhat offset his guns-AND-butter policies.”

Yea but this temporary tax surcharge had a very modest impact on consumption for reasons that the Ando-Modigliani life cycle model would have predicted.

I thought 2slug was quoting some fluff piece but I just realized he had selected only a small slice of your comment. Now that I have read your comment in its entirety, it makes more sense. Yes – the FED was not happy with the massive late 1960’s fiscal stimulus. Neither was the CEA.

Let me also add that we did get the Nixon recession when the FED listened to Milton Friedman perhaps a little too much.

The ten-year break-even is around 2.4%, term premium on tens is still negative at around -0.6% to -0.7%. Expected funding costs are rising. So everything that can steepen the curve is steepening the curve.

Still, policy has aimed at flattening the curve, showing up in lower term premium, and now we know that policy is likely to stop flattening the curve quite so much. A policy of flattening the curve is absent for most of the 75 years in question. Signals from the curve are not being drawn from quite the same pot as in the past.

Should have said term premium is still negative but higher than earlier in the year.

In a development largely ignored by the mainstream media, Elizabeth Warren asked the SEC to investigate corruption at the Fed, specifically violation of insider trading rules. https://www.politico.com/f/?id=0000017c-4c61-d47e-ab7e-dc7179ea0000

Of course, corruption at the Fed is nothing new, as Bernie’s GAO audit of the Fed found over 10 years ago: “ The GAO also determined that the Fed lacks a comprehensive system to deal with conflicts of interest, despite the serious potential for abuse. In fact, according to the report, the Fed provided conflict of interest waivers to employees and private contractors so they could keep investments in the same financial institutions and corporations that were given emergency loans.

For example, the CEO of JP Morgan Chase served on the New York Fed’s board of directors at the same time that his bank received more than $390 billion in financial assistance from the Fed. Moreover, JP Morgan Chase served as one of the clearing banks for the Fed’s emergency lending programs.”

https://www.sanders.senate.gov/press-releases/the-fed-audit/

And establishment mavens wonder why so many have so little trust in the Fed? Naturally, economists are noticeably silent on the issue, even though the Fed is responsible for a lot of economic policy, much of it favorable to their bankster owners.

[Of course, pgl will respond by saying that far from never talking about corruption at the Fed, economists talk and write about it every day!!!!]

“pgl will respond by saying that far from never talking about corruption at the Fed, economists talk and write about it every day”

Do you have to be such an annoying little lying twit in everyone of your worthless comments or what?

Insider trading is very wrong as any SEC economist would tell you – and yes I have had colleagues who worked for the SEC in the past. In my view, all members of the Federal Reserve should be required to put their financial assets in a blind trust if insider trading is even remotely possible.

BTW the SEC is generally quite good at taking down clear insider cheats but there is a measure of due process. Like with everything else a mere accusation is not nearly enough and the investigators must be thorough before they go out and tarnish someone’s reputation. Something that a lying troll like you would never understand.

And one more BTW – I would have applauded this Politico story had it not been wrapped in your usual pointless garbage.

Yeah, Warren felt impelled to take the time to write a letter to Gensler because she was absolutely, positively certain that he would do his job (sarcasm.)

At least pgl didn’t take issue with the findings of the GAO audit of the Fed that Bernie had done…though he subsequently objected mightily to any thought of doing another one. And the revolving door between Goldman and the Fed and the Treasury? Shhhh…hear no evil, see no evil!

“he subsequently objected mightily to any thought of doing another one.”

I did no such thing. Another one of your pointless and incredibly STUPID lies.

“In a development largely ignored by the mainstream media, Elizabeth Warren asked the SEC to investigate corruption at the Fed, specifically violation of insider trading rules.”

this is false. in fact, i linked to an article on this issue a week ago. this has been reported by the mainstream media. the problem is not the media, but the public seems not to care.

Yes, it turns out that many outlets did pick up on some aspect of this issue. But finding the story depended heavily on search terms used. Many chose to overlook Warren’s most explosive charge—a culture of corruption at the Fed.

You can enjoy her speech here: https://twitter.com/SenWarren/status/1445458867073257474

I expect that many, like pgl, will just yawn and say that it’s time to move on and proceed to his default mode of attacking anyone who criticizes the Fed. Warren makes a compelling case why allowing the Fed to continue it’s ‘old boy network’,’ business as usual approach would be folly.

“I expect that many, like pgl, will just yawn and say that it’s time to move on and proceed to his default mode of attacking anyone who criticizes the Fed.”

You are a pathetic little liar. This is an important story which the press have covered. Why ruin with your usual stupid garbage? Oh wait – that is all you know how to do. Never mind.

“Yes, it turns out that many outlets did pick up on some aspect of this issue. But finding the story depended heavily on search terms used.”

Typical JohnH BS. It took 2 seconds on Google to find lots of press stories. Now if the village idiot known as JohnH used Facebook the other day – no wonder this troll found nothing.

Come on folks – tell the troll to stop with these pointless lies.

JohnH,

This is a serious matter, and it is being investigated and reported on.

Where I have a problem with your discussion of this is that you have in the past claimed that this is how it always has been at the Fed and that this sort of thing drives what the Fed does and has done. That does not seem to be the case. It looks like this is a fairly recent development, a bad one, with this sort of thing needing to be squelched now and hard. The fairly sudden resignations of Fisher at the Dallas Fed and Rosengren at the Boson one look like there is action being taken on this.

I am aware that there was one previous case, but beyond that, I am unaware of any of this going on other than these recent bad cases in the history of the Fed going back to 1913. So, no, this is not the SOP of the Fed, even if you think that saying so amounts to “say it’s time to move on” and “alllowing the Fed to continue its old boy network.” Thar does not seem to be either what has gone on in general in the past or what is going on in general now. There have now been some cases, but it looks like the bad apples are being found and tossed out.

I could be wrong, JohnH, but I would suggest that if you wish to push this line that this is how the Fed has always operated, then you should provide some evidence beyond the one case of a Morgan in the past that I am aware of. Maybe it was going on and nobody knew about it, but indeed this is the sort of thing that would always have been newsworthy, so I doubt that there was a lot of it that simply never got reported.

I can’t say that the Fed has always operated this way. But The GAO did reveal some highly disturbing facts…particularly that the Fed has no system for dealing with conflicts of interest. That fact alone suggests that the Fed has turned a blind eye to corruption for a long, long time.

If you bothered to watch Warren’s brief takedown of The Fed, she makes very compelling case.

What strikes me more is that there is so little outrage among economists about the integrity a institution that is responsible for monetary policy and its implementation. Of course, we already know that the Fed has been captured by the industry it is supposed to regulate—it is owned by the big banks. It doesn’t get any more corrupt than that. Many industries have largely captured their regulators, but not to that extent. The Fed’s corruption is structural. It manifests itself in myriad ways revealed by the GAO audit and by the revolving door between the managers of big banks—Goldman in particular—and the Fed.

pgl, as a particularly egregious example of what I regard as economists’ general indifference to Fed corruption, offers us a daily dose of Trump or Republican hatred, but has never to my knowledge criticized the structural corruption of the Fed.

Given this, can anyone really trust the Fed to operate in the best interests of the American people and of the economy rather than in those of a handful of money Center banks? The GAO report that Bernie had done is not very reassuring.

Shouldn’t economists be deeply concerned that the Fed’s policies may be perverted in favour of its its owners?

Stiglitz has had some choice words about the Fed’s governance structure, which has been in place for decades:

“One of the world’s leading economists said Wednesday that the very structure of the Federal Reserve system is so fraught with conflicts that it’s “corrupt… ‘If we had seen a governance structure that corresponds to our Federal Reserve system, we would have been yelling and screaming and saying that country does not deserve any assistance, this is a corrupt governing structure,” Stiglitz said during a conference on financial reform in New York. “’It’s time for us to reflect on our own structure today, and to say there are parts that can be improved.”

https://www.huffpost.com/entry/stiglitz-nobel-prize-winn_n_484943

JohnH,

Everybody knows and has known about the banks owning the Fed since it was created in 1913. This is not a secret and never has been. As it was the link between the commercial banks and the Fed was probably stronger in its earlier days than it is now. Governors and chairmen were almost always actual commercial bankers for most of the life of the Fed up until just a few decades ago. It is only recently that we have had Chairs who were PhD economists who had not worked for a commercial bank, notably Ben Bernanke and Janet Yellen. Do you consider them to be corrupt pawns of commercial banks?

Of course, it is a bit of a debate just which policies “corruptly” support the commercial banks in an inappropriate way. While you seem to suggest that support the banking system is somehow inherently corrupt, I note that when banks fail bad things happen to lots of people and the economy. The extreme example was the Great Depression during which something like half the banks failed and we got to 25% unemployment rate. As a matter of fact wealth got more equally distributed as the top end lost lots of money in the low stock market, but I do not think those with no wealth and no job felt any pleasure in that development.

Of course, traditionally it was thought that the Fed was favoring the banks and the wealthy by pursuing high interest rate anti-inflationary policies, viewed as hurting poor debtors and slowing the economy, so also keeping unemployment too high. But now we see people arguing that low interest rate policies help the wealthy, in this case by stimulating the stock and other markets excessively. It has gotten sort of hard to figure all this out, frankly.

So I think you have been a bit careless here, which has quite a few people getting on your case and with reason. There is this current corruption of insider trading that is now coming to light and being investigated. And it is true that the Fed has no policies on how to deal with this sort of thing. But the reason for that is that this has basically not been a problem in the past. The past corruption was more subtle, people who worked at the Fed moving to work at commercial banks for good salaries after leaving the Fed. There was this long-existing revolving door that rarely got commented on. This is probably where we would see Fed people looking over the shoulders at the interests of the commercial banks, even more than the matter of people coming from those banks to hold high Fed positions.

Anyway, it is certainly true the the Fed has basically always been structured to favor the interests of the banks, as well as the wealthy. The new development has been this recent emergence of insider trading, something that almost never happened in the past apparently.

“Anonymous” there in the comment going on about things since 1913 was me. Not sure how my name did not appear.

Barkley Rosser

“But finding the story depended heavily on search terms used.”

again false. the story came directly to me on front news of cnn. it did not depend on search terms at all. it was easily available.

“Yes, it turns out that many outlets did pick up on some aspect of this issue.”

basically, all of your outrage seems to have been based on fake and trumped up accusations. this is why you are not taken seriously, Johnh.

Just about everything JohnH writes is false. He has amazingly consistent record I guess.

“In a development largely ignored by the mainstream media”

Another stupid lie. What did you do – use Facebook yesterday afternoon to search for news stories. Funny thing – I used Google today and LOTS of stories on this scandal popped up.

Come on – it is an important story so why do you insist on surrounding it with your usual stupid garbage?

https://www.nytimes.com/2021/10/05/opinion/low-interest-rates-monetary-policy.html

October 5, 2021

Pride and prejudice and asset prices

By Paul Krugman

The Federal Reserve and its counterparts abroad slashed interest rates in the face of the 2008 financial crisis and have kept them very low — in some cases below zero — ever since. This isn’t an arbitrary policy: Central banks believe that they need to keep rates low to avoid sliding into recession. But there has long been bitter criticism of low rates, coming from both the right and the left.

On the right, the main complaint seems to be that savers aren’t getting the returns they deserve — although it’s not clear why savers deserve high returns in a world that seems to have more savings than it knows what to do with. On the left, the complaint is that low rates push up the prices of stocks and other assets that are mainly owned by the rich. And this, the critics claim, widens inequality.

Well, I want to take on the latter argument, which is fundamentally misguided. And one way to illustrate why is to think about an economy simpler than the one we have now — the economy of Jane Austen’s England. I’ll explain later how the sense and sensibility we gain from Austen translates in the 21st century.

So: Early-19th-century England was an extremely unequal society that was still largely dominated by landowners, who lived off the rent paid by their tenants. This rent, as David Ricardo explained in 1817, was determined by the interaction of the population with the supply of fertile land. And the income from land was stable enough that it provided a quick measure of a man’s status. The marriageable Mr. Bingley had 4,000 pounds a year; the estimable Mr. Darcy, 10,000. Tellingly, “Pride and Prejudice” doesn’t tell us the value of either man’s estate; the income was the thing.

But England was also in the early stages of the Industrial Revolution, with a rising bourgeoisie deriving its income from industry and trade. This new elite differed in some important ways from the old elite, but the lines were never sharp. Industrialists could buy their way into the gentry by acquiring country estates. Landowners like the Duke of Bridgewater, who built a pioneering canal from his coal mines to the budding industrial center of Manchester, could invest in commerce. And both landowners and capitalists bought government debt, which, I can’t help mentioning, was much higher relative to G.D.P. at the end of the Napoleonic Wars than it is today:

https://static01.nyt.com/images/2021/10/05/opinion/krugman051021_1/krugman051021_1-articleLarge.png

Big borrowers, old school.

So what determined the interest rate on British bonds and the price of British land? The answer has to be that both depended on the returns from capital investment. There may have been some prestige associated with owning land and (maybe) some patriotism involved in buying public debt, but canny businessmen surely compared the rents or interest they could get by buying land or bonds with the profits they could expect to earn by building factories….

https://fred.stlouisfed.org/graph/?g=iTFT

January 30, 2018

Public Sector Debt Outstanding in the United Kingdom as a share of Gross Domestic Product, 1700-2016

Krugman writes well, but he’s no Jane Austen.

The Hulbert/Stack analysis appears only to ask whether the difference between one index and another index fell between recessions. How long before the recession, whether it was rising or falling just prior to the recession, how far it had fallen from the peak, whether it had fallen below some specific level – none of that receives notice.

So, I have considered the chart and I it doesn’t cause me concern. Next.

These market newsletter guys and all their cousins live and die by drawing attention to themselves. “Look at this scary chart!” is their stock in trade.

Their more sophisticated cousins look for pricing anomalies and can make serious money doing it. The “Look at that scary chart!” guys are doing a bad pantomime.

“I got the idea of focusing on the spread between those two indices from James Stack, editor of the InvesTech Research newsletter. He points out that the University of Michigan survey more heavily emphasizes consumers’ attitudes towards their immediate personal circumstances, whereas the Conference Board index more heavily reflects consumers’ attitudes towards the overall economy generally. So large negative readings, as is the case currently, means that consumers are more pessimistic personally than they are about the economy in general. (Full disclosure: Stack’s newsletter is not one of those that pay a flat fee to my auditing firm to calculate its track record.)”

Where was the editor of Market Watch? If he read this admission, he should have banned this fluff piece as a complete waste of space.

I just read something on Uber’s transfer pricing that made me go WTF? It was some allegedly learned European journal article on how we should use a profit split approach for ride sharing multinationals. Now this would sound like a grand idea if companies like Uber made profits.

Maybe the author could have checked its 10-K filings and noted Uber’s expenses represent about 150% of its net revenues. Splitting profits when losses are running $5 billion a year is a nice trick!

Can I add a caveat from an old yield curve junkie. A recession will occur IF in your case short raters rise because of the FED. It will not if bond yields fall.

Pretty clear the 10/30 year yield is driven whether a covid bottlenecks form. With the last one receeding, money is being pulled out and steepening is reoccurring. Caped expenditures are increasing in NG/Oil extraction and in the latter’s case, commodity speculation is not healthy. You never raise the price when actual on the ground extraction is increasing. Dummies.

Your auto-correct did you a disservice.

Bottlenecks driving bull flattening means long rates are less sensitive to inflation concerns than to growth. That has been the case for some time. It’s a low-inflation-regime feature.