Higher rates soon, long term inflation expectations anchored, and on term spread signals growth (as do real rates).

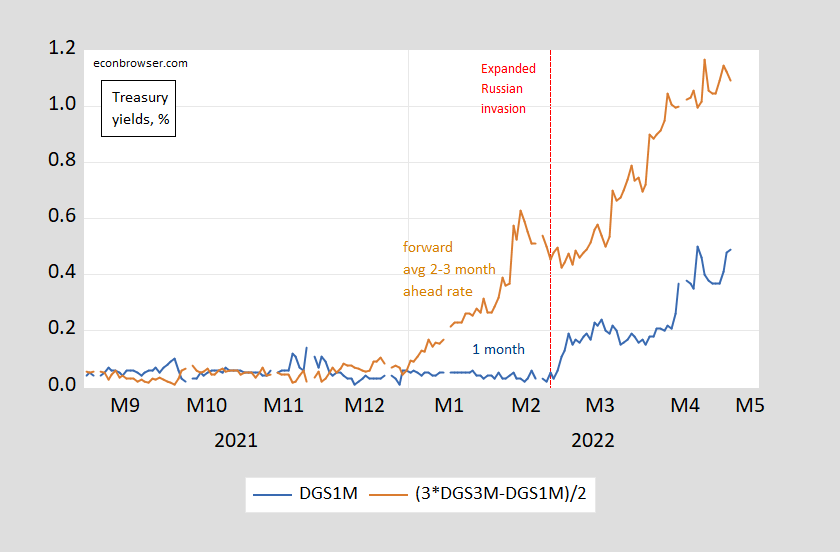

Figure 1: Treasury 1 month (blue) and one month forward 2 month (brown), in %. Source: Treasury via FRED.

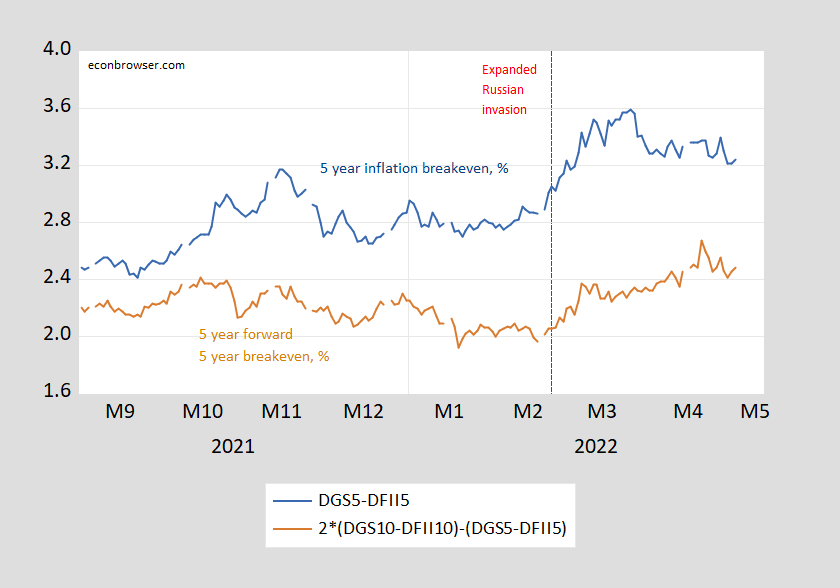

Figure 2: Five year Treasury-TIPS spread (blue) and five year forward five year Treasury-TIPS spread (brown), in %. Source: Treasury via FRED.

Figure 3: Ten year-three month Treasury spread (blue) and ten year-two year spread (brown), in %. Source: Treasury via FRED.

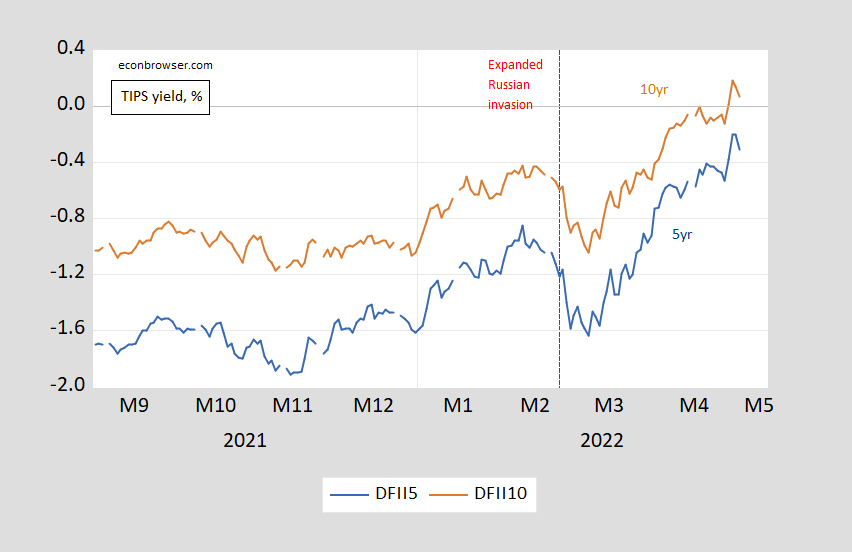

Figure 4: Five year TIPS yield (blue) and ten year TIPS yield (brown), in %. Source: Treasury via FRED.

https://news.cgtn.com/news/2022-05-05/Chinese-mainland-records-373-new-confirmed-COVID-19-cases-19MpjZi7aX6/index.html

May 5, 2022

Chinese mainland records 373 new confirmed COVID-19 cases

The Chinese mainland recorded 373 new confirmed COVID-19 cases on Wednesday, with 360 linked to local transmissions and 13 from overseas, data from the National Health Commission showed on Thursday.

A total of 4,740 new asymptomatic cases were also recorded on Wednesday, and 118,737 asymptomatic patients remain under medical observation.

Confirmed cases on the Chinese mainland now total 218,571, with the death toll at 5,141.

Chinese mainland new locally transmitted cases

https://news.cgtn.com/news/2022-05-05/Chinese-mainland-records-373-new-confirmed-COVID-19-cases-19MpjZi7aX6/img/b01d1c73d56a49c6a0a467a10c144eba/b01d1c73d56a49c6a0a467a10c144eba.jpeg

Chinese mainland new imported cases

https://news.cgtn.com/news/2022-05-05/Chinese-mainland-records-373-new-confirmed-COVID-19-cases-19MpjZi7aX6/img/f011b7d580d1497e97df665154170bcb/f011b7d580d1497e97df665154170bcb.jpeg

Chinese mainland new asymptomatic cases

https://news.cgtn.com/news/2022-05-05/Chinese-mainland-records-373-new-confirmed-COVID-19-cases-19MpjZi7aX6/img/c09aee3000d6441f91fd46d06dc3e8a9/c09aee3000d6441f91fd46d06dc3e8a9.jpeg

https://www.worldometers.info/coronavirus/

May 4, 2022

Coronavirus

United States

Cases ( 83,356,490)

Deaths ( 1,023,513)

Deaths per million ( 3,059)

China

Cases ( 218,198)

Deaths ( 5,128)

Deaths per million ( 4)

https://english.news.cn/20220505/f1768d9ff3284613aa4869098ac9e1e4/c.html

May 11, 2022

Consumption plays larger role to bolster economy

BEIJING — Despite multiple challenges, China is working all out to tap its consumption potential, as part of efforts to keep economic fundamentals stable and improve people’s lives.

Consumption is a primary engine for economic growth in China. In the first quarter, final consumption contributed 69.4 percent to the expansion in the gross domestic product, which rose 4.8 percent year on year.

Retail sales of consumer goods went up 3.3 percent year on year in the first quarter, but dropped 3.5 percent in March, the first decline since August 2020, due to resurgences of COVID-19 cases.

It is high time to let consumption play a larger role in the economic cycle and China should further highlight the importance of consumption in boosting economic growth, said Chen Lifen, a researcher with the Development Research Center of the State Council.

Chinese consumers are relatively more optimistic about the future in sharp contrast to the declining global consumer confidence, said a report * published by global consulting firm Ernst & Young (EY).

Approximately 60 percent of Chinese respondents believed their personal finances would improve in the coming year, higher than the global average of 48 percent, according to the latest EY Future Consumer Index report which tracks changing consumer sentiment and behaviors across global markets with 18,000 consumers worldwide surveyed.

China has adopted a slew of policies to counter the impact of COVID-19 and boost the recovery and growth of consumption.

The country in April unveiled guidelines to further tap its consumption potential, with detailed measures to tackle short-term bottlenecks and boost longer-term consumption vitality.

China will develop products and services that cater to the needs of the elderly and infants while encouraging innovations in cultural consumption, the guidelines said.

The country will also tap the consumption potential in the country’s vast rural areas, promoting the sales of automobiles and home appliances in these regions….

* https://news.cgtn.com/news/2022-05-04/Chinese-consumers-more-optimistic-about-future-EY-report-19L7HSdHwY0/index.html

ltr, why do you keep posting propaganda from the chinese communist party website? especially when it is irrelevant to the post?

Investment question. Say you have $100k in cash making nothing today. You want a treasury of some duration, year or less. Knowing the fed raised rates 0.5% yesterday, and may do so again in the next couple of meetings. What duration treasuries do you buy for the best investment over say the next 18 month time horizon? One or three month now and year later when rates are up another percent? Or dive into a 6 or 12 month now? Again this is for a total of say less than 18 months, but safe investment? I bonds dont count here.

markets should be arbitrage-free, so in some respects, it doesn’t matter. if you want your money back in 18 months, you should be indifferent between buying a 6 month tbill now + a 6 month tbill 6 months from now + a 6 month tbill 12 months from now, vs a 12 month tbill now and a 6 month tbill in 12 months. in fact, you should also be indifferent between those options and buying a 10 year tnote that you would then sell in 18 months.

investing is about understanding and taking risk. in the case of the options above, if you were to choose one over the other, you’re making a bet that interest rates will not evolve as currently priced by the market. if you were to buy the series of three 6 month tbills, you’re making the bet that 6 month rates will be higher in 6 and 12 months from now than currently priced by the market.

Brian, I understand what you are saying, especially in a more static environment. but obviously there will be increases in rates. so my question is, given the current environment and most likely expected environment, would you recommend buying short term now and capture the higher rates later? or would the 18 month time frame be a little too short to be much concerned?

“you’re making a bet that interest rates will not evolve as currently priced by the market. ”

I don’t follow the bond market that closely, so my issue is that I do not have a good understanding of how well bonds are currently priced. Meaning, is the current 6 month yield of 1.35% already most likely factoring in a 0.5% increase in each of the next few fed meetings?

Brian, you seem to have a clear understanding of the bond market. thank you for the comment. with your experience, what would you do? would you say rolling over every 6 months, while perhaps not the most optimal, would capture most of the potential gains over the next 18 months, assuming a steady 0.5% rate increase for the remainder of the year?

Barkley –

You seemed unsure of where the profit from the discount on Russian oil goes. Well, the NYT can help with that:

India’s purchases of Russian crude have soared since the conflict’s start, rising from nothing in December and January to about 300,000 barrels a day in March and 700,000 a day in April. The crude now accounts for nearly 17 percent of Indian imports, up from less than 1 percent before the invasion. Last year, India imported about 33,000 barrels a day on average from Russia.

“If oil is available and at a discount, why shouldn’t I buy it? I need it for my people,” Nirmala Sitharaman, India’s finance minister, said last month.

The Brent-Urals discount is holding steady around $36 / barrel, thus on 700 kbpd, the arbitrage is worth $25 million per day to the Indians.

https://www.nytimes.com/2022/05/04/world/asia/india-russia-oil.html

https://www.neste.com/investors/market-data/urals-brent-price-difference

“You seemed unsure of where the profit from the discount on Russian oil goes/”

So Dr. Chinn is stupid and you all knowing? Look we have been noting this large discount for weeks while you just now have figured it out? OK – more downstream profits and less Russian oil rents but you have not told us who owns the Indian downstream profits. Maybe it is my little Shell affiliate story and man are they profitable for 2022QI.

Steve – the NYTimes story was just step 1 in figuring out who gets the profits. And you call yourself an oil consultant? Really?

What does Menzie have to do with this? The note is addressed to Barkley, who did indeed express uncertainty about the destination of the discount.

The irony is, of course, that Russian oil revenues are up, not down, as reduced oil sales to date have been compensated by higher selling prices, even after the discount. Further, the beneficiary of the discount is not Ukraine, but India, and soon, China!

Moreover, I would expect Turkey to become implicated in this sanctions busting.

This sanctions regime is a bad approach to dealing with Russian oil.

Is Shell’s CEO going all boo hoo because his company has recorded a one-time accounting loss of late?

https://fortune.com/2022/05/05/shell-ceo-ben-van-beurden-points-out-loopholes-in-russian-oil-sanctions/

He claims that the global network of providing oil and gasoline makes it impossible to trace who is importing Russian oil. He uses this example – a Russian affiliate exports oil to an Indian refinery affiliate that converts it to diesel fuel. So when a distributor imports the fuel from India, we have no idea where the oil came from.

I say BS. If these affiliates were part of the Shell multinational, then the CEO knows who to call within his organization to trace these flows. If he doesn’t then he is utterly incompetent CEO. Now Shell might be reluctant to share its internal information but that is a different matter.

https://markets.businessinsider.com/news/commodities/russia-oil-production-20-percent-drop-eu-embargo-china-imports-2022-5#:~:text=From%20about%2010%20million%20barrels%20a%20day%20currently%2C,said%20the%20same%20decline%20will%20happen%20by%202030.

An interesting story about two alternative forecasts of how much Russian oil demand will decline as a result of EU sanctions – both of which account for increase buying from nations such as China. It seems both sets of forecasts differ from the extremely rosy claims (rosy from the perspective of Putin) made by Princeton Steve. Who to believer – a couple of oil analysts who know what they are talking about versus an internet troll who only claims he is the expert.

The article you cite says a decline of 20%, or about 2.2 mbpd. My forecast is a decline of 2.5 mbpd over the same period.

Not materially different assuming the current regime holds; but both are essentially finger-to-the-wind guesses. We have no direct historical precedent to the best of my knowledge.

“My forecast is a decline of 2.5 mbpd over the same period.”

But there was some fellow named Steven Kopits who declared to us that the sanctions would not effective at all. Could you tell that person to stop contradicting you?

Just as I was noting how the Shell CEO was going boo hoo over some one-time loss when CNN tells us that Shell and BP are making yuuuuge profits:

https://www.cnn.com/2022/02/08/business/bp-shell-profit-windfall-tax/index.html

OK – that is more like it. This story calls for a windfall profits tax which some economists have been advocating for a long long time. Do it!