Today, we are fortunate to present a guest contribution written by Laurent Ferrara (Professor of International Economics, SKEMA Business School, Paris, and Chair of the French Business Cycle Dating Committee).

After a robust second half of the year in 2021, economic activity in France stagnated in 2022q1. We review here the factors behind this sharp slowdown in economic activity and discuss the possible risks of future recession.

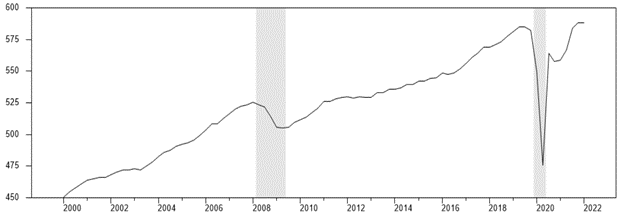

On 29 April 2022, Eurostat published preliminary flash estimate GDP data for the first quarter of 2022 for the euro area as a whole: the quarter-over-quarter growth was 0.2%, that is about 0.8% in annualized terms to be comparable with U.S. standards (see this Econbrowser post for an analysis of U.S. GDP). This figure hides large heterogeneity within the zone: +2.6% in Portugal vs -0.2% in Italy. A striking figure is the null growth rate for France, coming after a buoyant economic growth in 2021 (+1.5% in 2021q2, +3% in 2021q3 and +0.8% in 2021q4). After few months of rather flat economic activity just after the exit of the Covid recession (in 2020q2), the French economy was indeed recovering quite rapidly in 2021, displaying an annual GDP growth of 7% (see Figure 1).

Figure 1. French GDP and recessions since 2000

Source: Insee (real GDP in billions of euros) and French Economic Association (AFSE, Business Cycle Dating Committee)

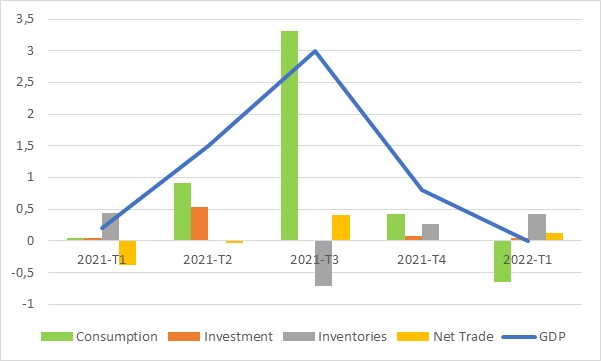

If we look at the various components of French GDP (Figure 2), it turns out that the drop in 2022q1 is due to a decline in household consumption of -1.3% compared to the previous quarter. The negative contribution of consumption to GDP growth is of -0.6 percentage points. Investment and net trade still show a positive contribution to GDP growth. In fact, since last year, the bulk of the GDP growth variance is due to changes in household consumption.

Figure 2. Contributions to GDP growth since 2021q1

Source: Insee, GDP in quarterly growth rate and contributions of consumption, investment, changes in inventories and net trade

What are the possible explanations of this negative evolution in household consumption for 2022q1? A first explanation is obviously the sharp increase in commodity prices, in particular oil and gas, leading in turn to an increase in consumer prices. A strong global demand associated with supply constraints initially generated a sharp increase in inflation starting with the exit of the Covid recession. On top of that, Russia’s invasion of Ukraine starting from 24 February 2022 added another layer of upward pressures on consumer prices, making inflation in France was 4.8% in April 2022. So the loss of household purchasing power related to increasing consumption prices can be viewed as a first explanation. However, we cannot rule out the fact that we are currently seeing a normalization in the consumption behavior of households after months of sustained expenses, especially in services such as restaurants, hotels or transportation. It turns out that after the Covid recession, French households had an excess saving of about 166 billion euros (12% of annual income) which was likely used to boost consumption in 2021.

Last, increasing uncertainties during the first months of 2022 also led to a wait-and-see attitude for consumers, in particular for big tickets items, and to precautionary savings. I refer here to at least two types of uncertainty: (i) the uncertainty driven by the war in Ukraine, perceived as a shock by public opinion, and (ii) the political uncertainty that prevailed before the French Presidential election that took place on April 24.

One question that is currently debated in France is to know whether the French economy is heading towards a recession. Recession phases are generally identified by economists using the “3Ds” rule that simultaneously assesses Duration, Depth and Diffusion of the phenomenon. So far, we have only seen one quarter of null GDP growth, meaning that the “Duration” criterion (at least two consecutive quarters) has not yet been met. The “Depth” criterion means that a recession translates into a significant decline in economic activity. It turns out that periods with slightly negative GDP growth are likely to be not considered as a full recession, but only as an economic slowdown. For example, that was the case in France for the 2002-03 period after the burst of the Internet bubble and in 2012-13 during the sovereign debt crisis in euro area (see this working paper). Last the “Diffusion” criterion means that a recession has to be visible in various economic variables at the same time (i.e. we should observe a strong co-movement). In this respect, beyond GDP, the French business cycle dating committee focuses on employment, business investment, hours worked and capacity utilization rate. So far, those variables do not show any evidence of a large drop in economic activity. Strikingly, household consumption is not part of this list, as this variable is too volatile and does not exhibit characteristics in line with the business cycle.

In sum, as of today, the French economy seems to be quite far from being in recession, though it is much too early to say definitively. Indeed, identifying a recession needs more data and more time. For example, the average delay between the start of a U.S. recession and its recognition by the NBER dating committee is about 7 months.

However, it is fair to acknowledge that some downside risks are currently weighing on French economic activity. First and foremost, the Russia’s invasion of Ukraine means that today macroeconomic risks in the euro area as a whole are now three times higher than in the U.S. (see this post). The most important channel of transmission is the sharp increase in commodity prices, mainly oil and gas, leading to a loss of purchasing power for French households. In addition, the Russian government threatens to cut European countries’ access to its gas, as it did for Poland and Bulgaria, and the European Union is currently debating the possibility of an embargo on Russian oil, leading to expectations of higher energy prices and eventually consumer prices. At some point, the ECB will have to tighten its monetary policy, just as the U.S. Federal Reserve and the Bank of England did, thus jeopardizing the economic activity.

Second, political uncertainty has not been fully resolved, as we will have two rounds of legislative elections on 12 and 19 June 2022 in order to elect the 577 members of the French Parliament. If the recently elected President, Emmanuel Macron, is not able to secure a majority, he will have to nominate a Prime Minister with a different political sensitivity, thus generating uncertainty as regards the political objectives of the next presidential mandate.

Third, the global economy is losing momentum due to the combined effects of the war in Ukraine, higher commodity prices, strict lockdowns in China, increasing central bank interest rates … World GDP growth has been revised down to 3.6% in 2022 according the April IMF World Economic Outlook. This means that France cannot rely on exports to sustain economic growth.

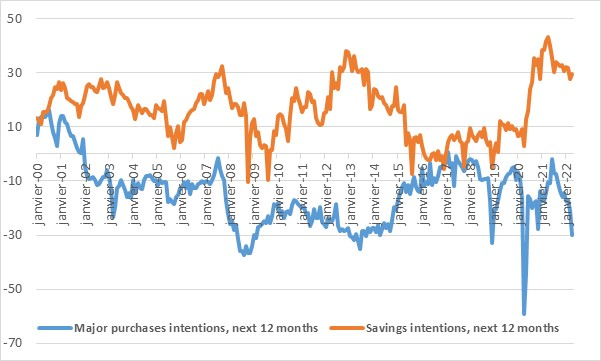

To conclude, the behavior of French households definitely has to be closely monitored in upcoming months. As a preview, we can look at the last opinion survey carried out in April by the French Statistical Institute (Insee) by households (see Figure 3). We note that saving intentions for the next 12 months stay at a high level, while major purchases intentions for the next 12 months dropped in April to levels consistent with past periods of economic stress. This increasing spread between the two components of the survey is clearly not a positive signal for future consumption. However, as I mentioned earlier, variables that would definitively help to characterize the occurrence of a recession in France, in addition to GDP, are employment, investment, hours worked and capacity utilization rate. Those variables have to be closely monitored in the upcoming months.

Figure 3. Consumer confidence indexes since 2000

Source: Insee

This post written by Laurent Ferrara.

Not only is the zero-Covid policies of China a failure to understand and properly respond to an evolving health crisis. The dictator has decided that any debate of this crisis is banned.

https://www.cnn.com/2022/05/06/china/china-xi-pbsc-zero-covid-intl-hnk/index.html

This will be an interesting case study of one of the greatest weakness of authoritarian regimes. As they ban the discussion of a realities they don’t like, they can cut themselves off from the obvious available ways out of a crisis. We often think of them as fully informed but deviously spreading lies to the public. What if they actually are not that informed, but making decisions within a bubble of ignorance – created by their own harsh rejection of unpleasant facts and inconvenient truths.

The strengths of democracy is that although you can create cultish bubbles of alternative realities (looking at you Fox), you cannot suppress availability of facts. The presence of fighting political fractions actually encourage distribution of facts that the ruling faction refuse to discuss or deal with.

https://www.worldometers.info/coronavirus/

May 5, 2022

Coronavirus

France

Cases ( 28,849,915)

Deaths ( 146,498)

Deaths per million ( 2,235)

China

Cases ( 218,571)

Deaths ( 5,141)

Deaths per million ( 4)

[ France unfortunately has recorded far more coronavirus cases than any country in Europe since 2020. Also, France, Germany and Italy are each recording high numbers of symptomatic coronavirus cases and deaths in 2022. ]

https://www.worldometers.info/coronavirus/

May 5, 2022

Coronavirus

Germany

Cases ( 25,203,564)

Deaths ( 136,564)

Deaths per million ( 1,620)

China

Cases ( 218,571)

Deaths ( 5,141)

Deaths per million ( 4)

https://www.worldometers.info/coronavirus/

May 5, 2022

Coronavirus

Italy

Cases ( 16,682,626)

Deaths ( 164,179)

Deaths per million ( 2,723)

China

Cases ( 218,571)

Deaths ( 5,141)

Deaths per million ( 4)

https://fred.stlouisfed.org/graph/?g=OYHE

August 4, 2014

Real per capita Gross Domestic Product for United States, United Kingdom, France, Germany and Netherlands, 2000-2020

(Percent change)

https://fred.stlouisfed.org/graph/?g=OYJ2

August 4, 2014

Real per capita Gross Domestic Product for United States, United Kingdom, France, Germany and Netherlands, 2000-2020

(Indexed to 2000)

https://fred.stlouisfed.org/graph/?g=OYK0

November 1, 2014

Total Factor Productivity at Constant National Prices for United States, United Kingdom, France, Germany and Netherlands, 2000-2019

(Indexed to 2000)

https://fred.stlouisfed.org/graph/?g=O6BZ

August 4, 2014

Real per capita Gross Domestic Product for United States, United Kingdom, France, Germany, Netherlands and China, 2000-2020

(Percent change)

https://fred.stlouisfed.org/graph/?g=O6C1

August 4, 2014

Real per capita Gross Domestic Product for United States, United Kingdom, France, Germany, Netherlands and China, 2000-2020

(Indexed to 2000)

https://fred.stlouisfed.org/graph/?g=O6cD

November 1, 2014

Total Factor Productivity at Constant National Prices for United States, United Kingdom, France, Germany, Netherlands and China, 2000-2019

(Indexed to 2000)

Fox and Friends invited Sarah Yuckabee to condemn the “lies” of the left and to condemn the peaceful protests of the left towards the Supreme Court over the Alito memo proposing to overturn Roe:

https://www.msn.com/en-us/news/politics/huckabee-sanders-calls-out-mind-boggling-hypocrisy-as-psaki-defends-activists-going-to-justices-homes/ar-AAWZrCv?ocid=msedgdhp&pc=U531&cvid=8bde5ff774b048db9f5535ba603ffe4e

Is this witch with a B telling us the Trumpsters never lied? That the Trumpsters never threatened people with progressive views with outright violence? OK – she was on Fox and Friends where MAGA types go to lie for the entire show. So hey!

The good news is that the issue of whether or not abortions will happen, has been solved in favor of choice long time ago. With pills that can be used to induce an abortion up to 10 (actually 13) weeks into pregnancy – they will happen. The wast majority of those who got an abortion in the past years will be able to get one in the coming years. The past decades of culture war over this issue has always been about whether a woman can get a legal abortion.

In the old days before Roe vs Wade we had to set up unsafe back alley coat hanger operations – now we just have to set up websites and call Fed. Ex. There will almost certainly be fewer “registered/official” abortions and a lot more “at home/mail order” abortion. But if someone think they need an abortion they will get it and neither those helping them nor those getting the abortion will be deterred by any laws. However, since a woman will be pressed to make an early decision on the issue of termination or birth, a lot of those who eventually decided to keep the pregnancy will now feel pressure to take the pills before it is too late. The numbers of those early termination (would have become babies) vs the small number who get past the pill stage and cannot get on a plane are likely to fairly small and cancel each other out. As usual those hurt will mostly be poor minority – and the middle class will barely feel a small bump on the road.

Agree, but the GOP knows this and that’s why they’ll push for more draconian controls, including ones at the federal level. Because they’re all about freedom.

“Total nonfarm payroll employment increased by 428,000 in April, and the unemployment rate was unchanged at 3.6 percent, the U.S. Bureau of Labor Statistics reported today. Job growth was widespread, led by gains in leisure and hospitality, in manufacturing, and in transportation and warehousing.”

That is the headline news from BLS. But wait – the employment to population ratio fell from 60.1% to 60.0% and the labor force participation fell too.

I’ve been wondering – mainly for the US issues but this could apply to France – how much is this the continuation of the shift from consuming services to consuming goods, which was brought on by this virus. And this virus has never really gone away with peaks and valleys for new infections. This shift at the same time caused weakness in the service sectors but also incredible supply side pressures in terms of goods being consumed.

I do know one could use FRED to separately track consumption of nondurable goods, consumption of durable goods, and consumption of services for the US. Are the French national income accountants presented with the same detail?

Yes, you can play with French data on consumption, in particular by splitting between various types of goods and services, using this file from Insee (French Statistics):

https://www.insee.fr/fr/statistiques/fichier/6439786/t_conso_vol.xls

Less evidence of a shift “goods vs services”, as in the U.S.

Best