A tautology:

MV ≡ PQ

Where M is money, V is velocity, P is price level, Q is economic activity.

Assume V’ is constant; then:

MV’ = PQ

Take logs (where lowercase letters denote log values):

m + v’ = p + q

Take difference with respect to a fixed date, and call that Δ :

Δm + Δv’ = Δp + Δq

Since V’ is constant, we can rearrange to obtain:

Δp = Δm – Δq

Let’s plot the change in the price level and the change in M2 to real GDP, relative to 2020Q1, the onset of the pandemic in the US.

Figure 1: PCE deflator (blue), M2/real GDP (tan), both in logs relative to 2020Q1 values. M2 values are end-of-quarter. NBER defined peak-to-trough recession dates shaded gray. Source: BEA, Federal Reserve Board via FRED, NBER, and author’s calculations.

It’s been about 2 years since the Fed increased high powered money and allowed that to manifest in an increase in broad money. Yet, the price level has only risen by about 7.9%, while the ratio of broad money to real GDP has risen 27% (in log terms).

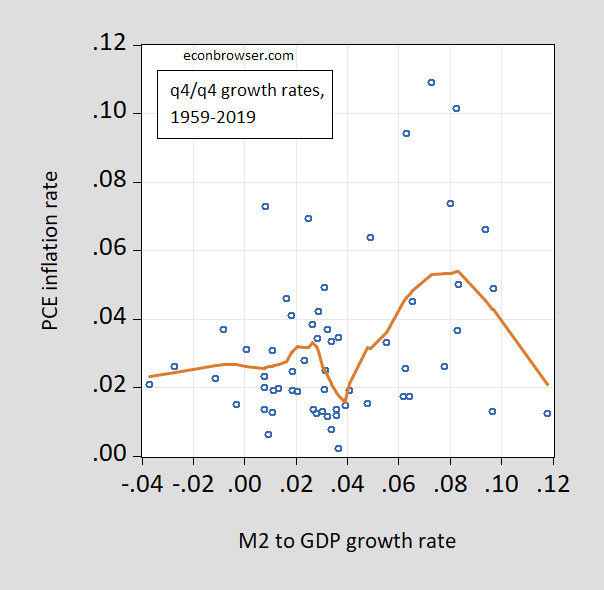

This lack of correlation between broad money and the price level is not an artefact of the covid era. Here is a scatterplot of inflation against growth of M2/GDP.

Figure 2: Q4/Q4 PCE inflation vs M2/real GDP growth rate (calculated in log terms), and nearest neighbor fitted line (tan). M2 values are end-of-quarter. Source: BEA, Federal Reserve Board via FRED and author’s calculations.

A more sophisticated version of the quantity theory would allow trends in velocity, and/or interest sensitivity. I do not think this would be sufficient to make the quantity theory empirically more valid than alternative approaches (see comparison empirically ad hoc quantity theory vs. Phillips curve).

This post inspired by Mr. Steven Kopits’s remark, as well as this comment.

A tautology. That is all it is. Princeton Steve, however, thinks it is some advanced macroeconomic theory. No this was debunked in that 1974 paper you linked to. I bet Steve has still not read it.

Steve will also hate the fact that you used logs even though the point was clear to the rest of us. And providing the actual data that he ignores? Shame on you!

One of the most brutal comments I have ever heard about some macroeconomic model that the person making the comment thought was outdated goes like this “do they still teach blood leeching in medical school?” If Princeton Steve were a doctor – he would be practicing blood leeching. Yes the QTM that he so loves is akin to teaching blood leaching.

https://www8.gsb.columbia.edu/faculty/jstiglitz/sites/jstiglitz/files/The%20Theory%20of%20Credit%20and%20Macro-economic%20Stability%20Final.pdf

November, 2016

The Theory of Credit and Macro-economic Stability

By Joseph E. Stiglitz

Towards a New Theory of Money and Credit

Standard modern monetary theory is based on the hypothesis that the T-bill rate is the central variable in controlling the economy and that the money supply, which the government controls, enables the government to regulate the T-bill rate.

Prevailing economic doctrines earlier argued that there was a simple link between the supply of money (say M2), which the government could control, and the value of nominal GDP, p (the price level) x Q (real output), described by the equation

(1) MV ≡ pQ

where V is the velocity of circulation. (1) is essentially a definition of the velocity of circulation. Monetarism translated (1) from a definition into an empirical hypothesis, arguing that V was constant. This meant that nominal income and the money supply moved in proportion.

Monetarists like Milton Friedman claimed further that (at least over the long run) Q was fixed at full employment, so that an increase in M would lead to a proportionate increase in Q. Shortly after these monetarism doctrines became fashionable, especially in central banks, the links between money supply (in virtually any measure), and the variables describing the economy (income, or even (real) interest rates) seemed to become tenuous. The velocity of circulation was evidently not a constant. Of course, there never had been a theory explaining why it should be.

Even before this, Keynesians had argued that V was a function of the interest rate. An increase in M is split in three ways, an increase in p, an increase in Q, and a decrease in velocity, with the exact division depending on the relevant elasticities (e.g. the interest elasticity of the demand for money, of investment, and of consumption.)

But beginning in the 1980’s velocity was not only not constant, it did not appear to be even a stable function of the interest rate—not a surprise, given as we have noted the large institutional changes going on in the financial sector (such as the creation of money market funds and the abolition of many regulations.) The natural response was a switch from a focus on the quantity of money to the interest rate. But while this experience should have led to a deeper rethinking of the premises of monetary theory, it did not….

” the links between money supply (in virtually any measure), and the variables describing the economy (income, or even (real) interest rates) seemed to become tenuous. The velocity of circulation was evidently not a constant. Of course, there never had been a theory explaining why it should be.”

What economic behavior does velocity depict? None. It is nothing more than the definition of a useless concept – velocity = GDP/M. No microfoundations model would even bother with this useless definition unless velocity were a constant. It is not. So no economist would ever call this a theory.

But to Princeton Steve – it is THE advanced theory. Yes – he is that clueless.

And then your inflation forecast is….what?

And if that’s the case, d you support the Fed’s dramatic interest rate increases?

Is this all got? Asking annoying questions. Tell you what Mr. Loud Mouth Know Nothing. Why don’t you answer your own questions.

That’s not an answer.

You do not deserve an answer. You are a know nothing pest bloviating BS all day without any recognition of: (a) what others are saying; or (b) basic reality.

You don’t have an answer.

Here’s my take.

The Pandemic and US Fiscal and Monetary Policy Errors

https://www.princetonpolicy.com/ppa-blog/2022/6/21/the-pandemic-and-us-fiscal-and-monetary-policy-errors

I welcome specific forecasts of inflation, especially from the guy who wrote this:

Does this mean we have no need to worry [about inflation]. If one believes that we will be way below potential GDP for a while, then no. Using the WSJ’s December survey mean forecast, and the CBO’s estimate of potential GDP, end-2022 is when one might start worrying about inflation, using this criterion; later still if using my estimate of maximal output (which depends on the actual evolution of output).

https://econbrowser.com/archives/2020/12/inflation-looming-phillips-curve-vs-quantity-theory

Sorry dude – NO ONE is reading your pathetic blog.

Steven,

Forecasting inflation is just plain hard when the exogenous situation is in flux on mutliple fronts, which it is.

There is a newsletter out of SF Fed about to be an Economics Letters article by Adam Haile Shapiro. I have not dug into his methodology, but he claims that of the increased rate of inflation, about half is due to supply side causes, about a third to demand side causes, with the remainder impossible to separate out, ptobably a combination.

Barkley –

That’s always your line. “Oh, it’s just too hard. I can’t figure it out. But I know you’re wrong, because, well, I don’t know why.”

Okay, you have nothing substantive to add to the discussion. I get it.

What a disgusting comment. You are one small little man with an overinflated ego. Go away. DAMN!

Barkley, “… but he claims that of the increased rate of inflation, about half is due to supply side causes, about a third to demand side causes, with the remainder impossible to separate out, ptobably a combination.” We have a Prez with policies that affect both supply and demand pf eneergy, which have resulted in inflation, maybe even stagflation.

I’m starting to see descriptors of: the worst of the worst for Biden. Dunno, we’ll; see in Nov.

As utterly stupid as the rants from Princeton Steve are – at least they are not as juvenile as your pathetic little comment.

CoRev,

What “descriptors of the worst of the worst”? While Steven accuses me of saying nothing of substance because I note that it is hard to forecast inflation even as I report on a study saying it is half supply side stuff and a third demand side stuff, I have elsewhere here argued that Steven is likely to be wrong about his inflation forecast because it looks that a number of the forces on both sides behind the inflation may be starting to ease.

Just to remind you what they are: 1) tightened fiscal policy Steven himself has been pointing out in his claims the US is going into recession, b) tightned monetary policy with noticeably higher interest rates among other things, 3) apparent end of lockdowns in major Chinese cities, 4) reports of improving situations at US ports, and 5) falling crude oil prices and now in the last week even gasoline prices by 10 cents per gallon.

Does not look lie a situation of worsening doom and gloom with higher inflation rates, even if the rate of inflation ls likely to be slow to decline now that it has become somewhat entrenched as Steven noted Janet Yellen has noted. But you and Steve can dismiss these observations because I am not making precise forecasts of exactly what the inflation rate will be at particular dates. I note that there are quite a few things out there that could push this either way that we cannot forecast, including the war, the pandemic, the food issue, as well as other hard to foresee developments in the energy sector, where Steven seems to be standing by Goldman Sachs forecast of $140 per barrel crude, even as those prices have been declining recently.

Got anything substantial on any of that to say yourself, aside from your usual rants about Biden’s essentially meaningless cancellation of the Keystone pipeline?

VMT says US entered recession in the Jan-Apr time frame.

Michigan Consumer Sentiment posted a new all time low for June, 50.0. That also suggests we’re in recession.

I would not read too much into falling crude prices at present. Crude will tend to track other capital markets in the short term. But if we’re in a recession, yes, at some point crude should fall.

My analysis suggests that the US could see both inflation and and recession at the same time.

CoRev We have a Prez with policies that affect both supply and demand pf eneergy

So you believe Biden and the rest of NATO should have abandoned Ukraine and allowed Putin to have his way? Is that your view?

2slugs, the Ukraine policy is too limited to define Biden’s energy policies.

CoRev Outside of supporting Ukraine, Biden hasn’t done anything that would reduce current energy to the market. In fact, he’s been releasing oil out of the SPR at a pretty good clip. He’s even going to embarrass himself by visiting a murderer in Saudi Arabia. And if you’ll look at BEA industry data you’ll see that gross output of domestic oil and gas extraction has been steadily increasing since Biden took office. And gross output from utiilities is also up. Remember, energy includes more than gas and oil. Has Biden pushed for policies that would reduce future fossil fuel production? Yes, although not nearly as much as I’d like to see. But all that’s for the future. As I said, outside of supporting Ukraine, Biden hasn’t done anything that would restrict current energy output on the global market. Once again, you just spout BS based on your gut without ever consulting actual data. BTW, I take it by your obvious attempt to duck my question that you are in fact a closet Putin supporter. Maybe we should start calling you Comrade CoRev.

2slugs if you are going to make claims it’s always best to show data to support them. https://www.eia.gov/dnav/pet/pet_crd_crpdn_adc_mbblpd_a.htm

2016 2017 2018 2019 2020 2021

8,844 9,357 10,941 12,289 11,283 11,188

Your claim: “And if you’ll look at BEA industry data you’ll see that gross output of domestic oil and gas extraction has been steadily increasing since Biden took office. ” Maybe 2022 will be the year when he surpasses Trump’s 2020 recession year.

This is a lie and weasel wording: “CoRev Outside of supporting Ukraine, Biden hasn’t done anything that would reduce current energy to the market.” The list is long of his energy policy Executive Orders restricting access. Maybe 2022 will be the year when he surpasses Trump’s 2020 recession year.

You’re getting your fondest climate change policy wish: “Has Biden pushed for policies that would reduce future fossil fuel production? Yes, although not nearly as much as I’d like to see.” Except for you ideologues, the world is starting to recognize the folly of these fossil fuel policies.

Biden net approval 6/26, day 521 of the administration:

Trump: -9.3

Carter: +0.2

Biden: -16.6 (all-time low for any president for this day in his administration, since Truman)

Biden could wish to be as popular as Jimmy Carter. Just one mistake after another.

https://projects.fivethirtyeight.com/biden-approval-rating/?ex_cid=rrpromo

Me thinks Stevie is getting angry at people correcting his pathetic understanding of basic macroeconomics. Of course it is not your fault or mine that he cannot take the time to take a principles course. Oh well – maybe someday he will be invited back on Fox and Friends to pretend he is their chief economist.

Yea I decided to torture myself and read one of your patented dumb posts. I should have stopped here:

The critical mistake appears to have been conflating a suppression with a depression. Other mistakes followed from this fundamental misconception. When the pandemic hit, policymakers adopted the 2008 experience as the template and decided to ‘go big or go home’.

How utterly wrong. How utterly pathetic. But no – I decided to read on.

Therefore, the Fed and the Biden administration deemed a much larger stimulus and fully accommodative monetary policy to be appropriate. Unfortunately, this involved an error of construction, the mistaking of a suppression for a depression.

Any sane person would have thrown away his computer after this garbage but no me.

We define a depression as an economic downturn linked to a large decline in house values.

Oh Lord – you are the dumbest moron ever. But yet I read on.

The term ‘suppression’ is not commonly used in economics. Indeed, the profession does not distinguish among recessions, depressions or suppressions.

As used here, a suppression means a reversible outage, an exogenous restriction on economic activity. In this case, the suppression arose from pandemic-related lockdowns and spontaneously from the public’s fear of infection were they to leave their homes. None of this had to do with the business cycle.

To illustrate, consider a hypothetical teenager, Bobby. Imagine Bobby had the flu, and we gave him stimulants and medicine to feel better. After a while, he would recover and gradually rejoin society. This describes a typical recession. Now imagine instead that Bobby’s parents had grounded him and confined him to his room. At the same time, those same parents gave him $50 and some amphetamines to stimulate his activity. Bobby, when released from his captivity, would come out amped up and ready to spend. That is the difference between suppression and a recession, much less a depression.

Christ All Mighty! Even Bobby refused to read the rest of the dumbest post ever written.

I did try to wade through the rest of your intellectual garbage which you must think as technical analysis. The Quantity Theory of Money? And made up numbers that would even embarrass Lawrence Kudlow. I presume you worked hard on that post. Congratulations – you have managed to write the dumbest thing ever devised by man.

I have uploaded the associated spreadsheet file. Knock yourselves out.

I am interested in what is likely to happen and why. I am happy to take anyone’s forecast of actual inflation, not mumbo-jumbo about on-the-one-hand-on-the-other-hand. My forecast is inflation of 8-12% per annum for the next 6-8 quarters. If you’ve got a better number, let’s see it and explain your reasoning.

It’s important for a lot of the work I do to have some sense of the likely path of inflation, interest rates and GDP, to the extent possible. I am not particularly interested in winning or losing the argument. I am interested in understanding plausible paths of inflation over the next twelve months or so. For example, Secretary Yellen, after having advocated for ‘transitory inflation’, has now stated that inflation may remain ‘locked in’ for the balance of the year.

Specifically:

“We’ve had high inflation so far this year, and that locks in higher inflation for the rest of the year,” [Yellen] said Sunday on ABC’s “This Week.”

That’s quite a change of heart. Is she now using a different model than she did a few months ago? Why? Does her reasoning now accord with Menzie’s rather breezy view on the matter? Or has Yellen become a QTM convert? How should we think about the likely path of inflation going forward?

https://www.princetonpolicy.com/ppa-blog/2022/6/21/the-pandemic-and-us-fiscal-and-monetary-policy-errors

“I am interested in what is likely to happen and why.”

Really? It strikes me that your only interest is blovating BS so you can appear on Fox and Friends.

It matters. If you think the inflationary impulse comes principally from the stimulus and supply side effects, then the Fed raising rates willy-nilly is going to be a disaster.

On the other hand, if you think monetary policy is driving inflation, then raising rates is the right thing to do. But then you may be compounding a technical recession from the roll off of stimulus with a cyclical recession arising from increased interest rates. That may be the price you have to pay.

I am personally not sure which factor matters more. Yesterday at Stop ‘n Shop my bellwether avocadoes were back at the pre-pandemic $1.66 / avocado, and navel oranges, now of out season, were down 20% in price. Is this purely a seasonal issue, or does it mean that inflation was principally associated with the stimulus and supply-side effects?

In event, this is far from an academic debate. If Powell has got it wrong, the Fed will crater, well, it’s already cratering, the economy.

I know you are trying to make some sort of contribution but your comments are the dumbest and most pointless rants I have ever seen. You are not qualified to comment on Federal Reserve policy as you are an utter imbecile when it comes to macroeconomics. STOP wasting our time with your nonsense.

Steven,

Oh, here you are going wishy washy on whether it is supply side or demand side.

When I reported on a serious SF Fed study claiming it is half supply side and a third demand side, you denounced me for noting “it is hard to forecast inflation,” although I did forecast it is likely to decline and that your 8-10% coming up is probably going to be wrong.

And here you are now telling us about lower avocado prices and how maybe the Fed is overdoing its anti-inflation policy. Really? I am less opposed to people changing their minds on the basis of new information, but is that what you are doing here? Are you abandoning that big forecast of higher inflation you made such a production of and then sneered at people like me because i was not making some specific inflation forecast based on some specific model?

If you’re saying supply and demand, it seems to me you’re making principally a pandemic and stimulus-based forecast. If that’s the case, I would be very careful with interest rate increases, because most of the inflationary pressures should wash out by themselves. Pandemic bottlenecks will ease and over-stimulated demand will end.

If you’re making a QTM argument, then inflation will be around for a while, recession or no.

Steven Kopits No one should be making unconditional forecasts. As JDH’s recent post argued, potential GDP is lower than expected. Why? The most likely suspects are continuing productivity issues with COVID, countries locking immigration, and the war in Ukraine, which is causing a global rise in fuel and food costs. Those are all exogenous shocks. Absent those shocks we’d probably be seeing inflation in the 4% range, which you can probably attribute to fiscal and monetary policies that supported the economy during the pandemic.

Slugs –

Oil was expensive before the war. Keep in mind, Russia’s production is only down about 1.6 mbpd, best I can tell. That’s not very much in the global context of 100 mbpd.

Slugs –

You’re implying you would have signed off on a 40% increase in M2, had you been on the technical staff at the Fed, because it would have no effect on inflation. I would not have signed off on that fantastic surge in the money supply over such a short period.

That’s quite a change of heart. Is she now using a different model than she did a few months ago? Why? Does her reasoning now accord with Menzie’s rather breezy view on the matter? Or has Yellen become a QTM convert?

You are one insulting little twit. Yellen was being honest – something that you never do. She has not abandoned basic macroeconomics by adopting your stupid QTM garbage, And Dr. Chinn is a lot more articulate so to say he has a rather breezy view is disgusting. Look – I would have him ban you for your ultimate stupidity and these stupid little cheap shots. Just because Yellen is smarter than you are gives you no right to write such insulting garbage.

This sentence alone shows how utterly ignorant you really are:

We define a depression as an economic downturn linked to a large decline in house values.

The crash in real output from 1929 to 1932 aka The Great Depression was not caused by a decline in housing values or even a slump in residential investment. Try a stock market crash and a crushing decline in business investment. I guess you are worse at economic history than even your pathetic lack of understanding of macroeconomics.

In fact, house prices fell dramatically after 1929. In some places in New York City, property values did not recover their pre-Depression levels in nominal terms until the 1960s. Before the pandemic, only two times in the last century did the Fed put st interest rates to zero and leave it there for an extended period of time: after 1929 and after 2008. In fact, short term interest rates were set effectively at zero for seven years or more. The reason this did not cause a spike in home values was because collateral was impaired, ie, home equity was negative in many cases. This was emphatically not true in 2020, and putting the FFR to zero led to a spike in house and other asset values in a matter of a few months, just as we would expect in a healthy economy.

I am certainly sorry that you cannot distinguish between a recession, a depression and a suppression. But, hey, look on the bright side. Neither can the Fed.

“In fact, house prices fell dramatically after 1929.”

If they did – where is your evidence? Oh you just made that up. And even if they did – show us the analysis that this either affected investment demand or consumption demand. Oh you can’t. As usual you just make up gibberish as you go.

“Steven Kopits

June 25, 2022 at 1:10 pm

Do your own research. It’s out there. I found it.”

You are the Rudy Guliani of the economics blog. You found what? No link? No – you are lying now.

Economic historians attribute the Great Depression to a variety of things beginning with the stock market crash and a plunge in business investment. Bank failures – many of which are thoroughly discussed by Friedman and Schwartz – played a major role. Perverse fiscal policy ala Herbert Hoover played a role and perverse monetary policy driven by being on the gold standard also played a major role. And of course having a trade war during the middle of the Great Depression was a horrific policy move.

Now weak aggregate demand would certainly his housing markets but once again the dumbest troll ever (Princeton Steve) gets cause and effect backwards. Now if Stevie knew a damn thing about this period – which of course he does not – he might note the policy moves under both Hoover and FDR to shore up the housing market.

BUT NO – in another stupid attempt to justify his stupid and worthless definitions – Princeton Steve proves he knows NOTHING about our economic history or basic macroeconomics. NOTHING AT ALL.

Do your own research. It’s out there. I found it.

“The Nobel laureate economist Milton Friedman famously said that “inflation is always and everywhere a monetary phenomenon, in the sense that it is and can be produced only by a more rapid increase in the quantity of money than in output.” M2 is a widely used measure of the quantity of money, and it has increased by 39% since the start of the pandemic. If Friedman were correct, we would expect prices to rise by the increase in M2 less the increase in GDP. GDP has risen by 5% since the beginning of the pandemic, and therefore we might expect prices to rise cumulatively by 34%, all other things equal.”

I would not be surprised if the late great Dr. Friedman rose from the grave and decided to beat the troll named Princeton Steve silly for such a total misrepresentation of his work on macroeconomics. Yes Princeton Steve thinks he is citing Friedman as an authority but if Friedman were alive today, he would destroy this Economic Know Nothing.

BTW – his little graphs of fiscal stimulus measured it by the actual deficit which is heavily influenced by the change in GDP and is not an exogenous variable. We asked the dumbest consultant ever to read E. Cary Brown AER (1954) for why his measure is wrong, wrong, wrong but Stevie is too busy bloviating to read actual economics.’

OK I have spent way too much time on such an utterly worthless post.

‘GDP has risen by 5% since the beginning of the pandemic, and therefore we might expect prices to rise cumulatively by 34%, all other things equal’

Never mind that fact that GDP/M2 has declined dramatically. Stevie actually thinks “velocity” is a constant? Dumbest troll ever!

pgl: Thanks for sacrificing brain cells so that we don’t have to.

If Moses is willing – he can send me a bottle of his wine so I can sacrifice more brain cells for the cause!

Then the onus is on you to explain the trajectory of M2 velocity, that is, why would we expect it to remain permanently depressed? What’s the theoretical basis for that assumption?

Why is it anybody’s “onus” to explain anything about what M2 does? It was linked to nominal GDP prior to 1985, but then became completely disconnected from it and essentially has been behaving quite arbitrarily since for reasons not easily explained and of little consequence for the economy, So, sorry, Steven, an exercise not worth anybody’s time.

“Then the onus is on you to explain the trajectory of M2 velocity, that is, why would we expect it to remain permanently depressed? What’s the theoretical basis for that assumption?”

You get dumber by the day. Let me repeat SLOWLY so maybe you get it. Velocity is a worthless abandoned concept with no theory behind its stupid definition. I have no onus to explain some weird tautology that even the monetarists abandoned over 40 years agp.

Do you EVER pay attention to anything beyond your own stupid bloviating? It does not appear so. Move on troll as you have become a total bore.

Steven,

Sorry, I have not read your blogposts, but based on what I see here, I think you are wrong. I am not going to provide a specific forecast, but I will say I think we have reached the peak in the rate of inflation. So, I doubt your 8-12% forecast over next several quarters will happen. Likely to be lower, although I do not know by how much.

Funny thing is that you have been providing lots of reasons why we might expect disinflation to kick in, if rather slowly. The high fiscal stimulus that happened last year that had you and Summers all jumping up and down is over, and you have even noted this as a reason why we might be in a recession. Also, monetary policy has become a whole lot tighter. So basically both fiscal and monetary policy are now pushing to reduce aggregate demand substantially.

This latest study out of SF Fed says supply side more important than demand side, but it is hard to forecast what will happen there. There are reasons to think that China may be ending its lockdowns, and there are some reports that situations at ports and some other pieces of the supply side may be improving, although there remain lots of problems there. And while oil prices went back up a bit today, it may also be that the Goldman Sachs forecast of $140 per barrel may be unlikely. Gasoline prices just dropped by 10 cents in the US this past week, not a lot, but this is in the opposite direction of your forecast.

On oil prices, there is a lot that is really unclear and messy. There is a strange thing going on regarding the Putin war. We have heard so much about how Russia making more money due to the higher crude prices, although those are now declining and supposedly they are having to sell at discounts to India and China. I am not sure I believe the numbers being reported on Russia’s oil revenues, and my connections there do not help me out on this. But it occurs to me that a reason crude prices may be trending down is that Russia is indeed getting lots of its oil out through India and China, which is undercutting those high prices they have been getting.

Even harder to predict is MbS and Saudi Arabia. I know a lot more about that place than I have ever talked about here, but my knowledge about it leaves me knowing that I do not know what they will do. The horrible MbS, who has people I personally know still locked up, has seemed to be enjoying the recent high prices and playing palsy walsy with Putin. That makes me think he might ignore Biden’s request he increase production. OTOH, it may be that he would like to stop being a “pariah” and may actually provide some increase in production beyond trivial when Biden shows up. But I do not know.

Yeah, Steven, I am not a consultant who delivers specific numbers, a matter on which you agree with Moses Herzog as being BAD. In 2021 while you inaccurately predicted crude to hit $100 I was the only person here to warn that there was a large range of possible outcomes, yeah, the worst of that “on the one hand this, but on the other that” you claim to despise. Well, tough, I look at the uncertainties out there, which are huge, and say this is where it is at.

A comment on Yellen’s comment. You look to be making too much about what she said. She accurately noted that there is now an entrenched level of inflation above the old 2%. I see her saying that it will take some time to get back to that, if we can at all. But if you read her statement carefully, I do not see her as saying inflation will remain as high as it is now, much less the higher you are forecasting, which looks to me to have lost its basis.

I thoughtful comment. I guess not reading his blog posts has allowed you to stay sane. So don’t bother with his BS as life is too short.

If the stimulus is principally responsible for inflation, I do not expect slow retracement. I expect fast retracement, if you want a date, by the end of Q3. That’s why I would go slow with the rate hikes until we have some confidence that the effect of the stimulus has cleared. If inflation is due to the stimulus, it should begin to drop the next few months. If it’s monetary policy, we’ll see the levels I have forecast.

Steven,

There are lots of factors that entrench a new level of inflation for awhile once it get there, including wages adjusting to the past inflation. We are having some of that. This is what Yellen was talking about, which I think you did not quite figure out. So, no, even with the withdrawal of the fiscal stim and the tightening of monetary policy, there is still a lot of trouble on the supply side, see entrenched inflation in the Eu and elsewhere, as well as this momentum effect. So, inflation more likely to decline somewhat slowly, even if your forecast of steady or rising proves wrong, as I think likely.

Linking wages to past inflation is a QTM argument. You’re saying there’s excess money sloshing around. If it’s stimulus and supply bottlenecks, you should get pretty quick retracement because consumers’ budget constraint should be unchanged, as will be that of businesses once the pandemic money flows through. Put another way, avocados go back to $1.66 because that’s all the consumer can afford.

If you’re talking wage/price spirals, you’re pretty strongly suggesting an issue with the money supply.

No, Steven, linking wages to past inflation is most definitely NOT a QTM argument. Those back in the 70s who emphasized the wage=-price spiral dynamics were not the monetarists. As it is, the guy you have been touting as the great hero in all this (aside from yourself, of course), Larry Summers, mentioned this last year when he warned of how inflation could accelerate and get entrenched at a higher level that would be hard to reduce without pushing the economy into a recession.

As it is, it is unclear how strong those dynamics are. I think I saw Krugman claiming they are not very entrenched, despite some clear “catchup” wage hikes going on. So, it may be that we are not too far into it, meaning that indeed there is more opportunity for inflation to move down at least somewhat more rapidly. I would like to see that, but I understand Yellen’s concern about there being some entrenchment. And, sorry, no, this has nothing to do with any measure of M.

Steven Kopits

June 25, 2022 at 1:15 pm

Linking wages to past inflation is a QTM argument.

Stevie is getting dumber by the day. No – this is a Friedman-Phelps argument which has nothing to do with QTM.

And by the way, we have two things going on here, the run-off of the stimulus and monetary policy. They’re both monsters, and it’s difficult to segregate them. Happy for thoughts on that, too.

“They’re both monsters, and it’s difficult to segregate them. Happy for thoughts on that, too.”

You do have a talent for writing the dumbest things. We have asked you to stop with this BS. Try paying attention.

“it’s difficult to segregate them”

Stevie writes that is difficult to segregate fiscal policy v. monetary policy? WTF does this sentence even mean? Trust me Stevie has no effing clue.

But there were some smart conservative economists over 40 years ago that came up with an idea called fiscal dominance. Another concept which eludes Princeton Know Nothing Steve but for those who are interested I am talking economists such as Robert Barro, Tom Sargent, and Neil Wallace. Their writings were interesting but I dare say WAY OVER THE HEAD of Princeton Know Nothing Steve.

They were concerned that the massive Reagan fiscal stimulus during 1981/82 would force the FED to monetize the ensuing deficits at least eventually. Got what? Volcker proves them wrong as he kept monetary policy tight long enough to lower inflation. Yea it helped that Reagan got around to firing his supply side morons and listened to folks like Martin Feldstein and William Poole. Of course Princeton Know Nothing Steve has no clue who they are either.

Monetarism focuses about monetary shocks but not other kinds of shocks. Friedman’s monetarism took a dim view of Keynesian economics, even though Keynes accepted that monetary policy was the tool of choice except when rates were near the zero lower bound. (There’s that connection between V and i.)

Not caring about non-monetary shocks means not testing for them, not allowing for the possibility that other shocks might be the ultimate cause of inflation or recession. (Yeah, yeah, I’m oversimplifying.) But we know hyperinflation is associated with failed governance, which is often characterized by fiscal excess on a grand scale. The Asian Crisis and the Tesebono Crises both resulted from borrowing in somebody else’s currency – inflation resulted from devaluation, not monetary excess per se. We know that inflation in the 1970s was associated with a supply shock. The policy error in the 1970s was to accommodate price adjustment with monetary expansion, but the ultimate driver of inflation was a supply shock.

Wih that knowledge of history, it makes sense to look for non-monetary shocks now, simply to assure we aren’t making the mistake of ignoring potential causes. As soon as we look,we find: Covid, war, fragile supply chains, tariffs… Should the Fed accommodate price adjustment with monetary expansion? Probably not. Will recession reduce the welfare loss associated with supply-shock-induced inflation? Probably not.

But maximizing welfare is not the goal of commenters cheering for recession, is it?

Hyper-inflation is associated with the uncontrolled growth of the money supply.

Oh yea – 8% inflation for a short period of time is now hyperinflation? Your stupidity is getting absurd.

In the US, the voters will punish 8% inflation. You bet, in the US context, 8% constitutes hyperinflation from the public’s perspective.

Stevem,

Unfortunately, you may be right that US voters will punish Dems and Biden for 8% inflation, even though we see a similar rate in most of the other high income nations, suggesting that this is not exactly due to some specifically bad policies by Biden or even the Fed, your efforts to revive an out-of-date version of the ATM to the contrary. But even if they do that in no way makes such a single digit annual rate “hyperinflation.” The World Bank defines that as 50% per month. Please, do not degrade the language further people are stupid.

As it is, I am frustrated that people are clearly not giving Biden any credit for a lot of good things going on. The pandemic is much more under control that it was and all those umpopular lockdowns and mask restrictions are gone. But is he getting any credit? Does not look like it.

The labor market is as good as we have ever seen. If unemployment rises, sure as shooting people wiill whine. But are they applauding one of the lowest unemployment rates ever seen? I am still waiting.

Then he managed to pass an infrastruture bill that looks pretty good, one that Tramp never could even propose, just hold vacuous weeks. But everyone has forgotten it, and GOP pols are taking credit for money coming to local areas from it, even when they voted against it.

Yeah, inflation is higher than it has been in 40 yrars. But in fact, as noted, those gasoline prices people supposedly obsess about are actually going down now, if not rapidly. But is that helping his standing? Why not?

I could go on about foreign policy, but I suspect that is moatly a wash. Yeah, he lost a lot of atanding with the messy exit from Afghanistan, but there are no longer US trioops dying there, and if Tramp had been in the exit probably wuold have been oworse. He wanted out on May 1.Biden got about 70,000 people out by delaying the exit, but he took a big hit in standing.

War in Russia? He has managed standing up to Putin pretty well, but this looks to be overall a wash or even slight negative. What I think he should be criticized for, not getting back into the JCPOA with Iran, people seem not to mind. Gag.

So, frankly, Steven, I am not at all impressed with what polls say about Biden. I think he has mostly done not too badly, much better than Tramp. He is a victim of a lot of exogenous stuff happening to the whole world. I think people are just tired out by all of it going on for so long. So they blame him, even though on many parts of it, such as the pandemic and the job market, he has clearly made things better.

OK – then your “public” is almost as stupid as you are.

Barkley –

I am aware of the general definition of hyper-inflation. We have discussed it here not too long ago, and I am Argentinian by birth and Hungarian by descent. We know hyper-inflation. Notwithstanding, 8% inflation in the US is ‘out of control’ by the standards of the public, and they will vote accordingly. We’re looking at the twilight of the Democratic Party, I think, quite similar to what we’ve seen in Hungary since 2005.

As for Biden’s track record:

1. The Afghanistan pull out was a disaster. It destroyed Biden’s presidency and he will never recover from it.

2. The strength of the labor market comes from the stimulus and monetary policy, but in any event, I certainly predicted a very tight labor market in the 2020s, owing to limited growth in the labor pool and sharp growth in the number of retirees. I haven’t changed this view.

3. Infrastructure bill: What has it done for you? Nothing that I can see, where I live.

4. As for oil prices, let me quote myself from my Feb. 2021 report entitled “Sucker Punch”

The EIA believes that OPEC+ will prove sufficiently accommodative in expanding the oil supply to push oil prices back below $50 / barrel

As such a policy would be suicidal for OPEC+ revenues, we believe this now battle-hardened cartel will add supply with a lag to demand and thereby keep pushing prices up. This will continue until US shales recover, which we anticipate not sooner than H2 2022.

US administrations tend to give credence to EIA forecasts. The EIA may be providing a too rosy view of oil market dynamics to the Biden administration. The EIA continues to believe that oil prices will fall back to the high $40s and settle in the low $50s.

With demand recovering, US shales sidelined, and OPEC firmly in control, we think oil prices will remain elevated (and futures markets are materially underpricing oil). The EIA’s price forecast is potentially setting up the Biden administration for a ‘sucker punch’, with gasoline possibly cresting $3 / gallon ($4 / gallon in California) as we head toward 2022, with all the political problems that could bring for the midterm elections. In our view, the Biden administration should take a more balanced view of energy policy to hedge its political fortunes

I didn’t think gasoline prices would go so high, but I was directionally correct. So Biden gets a failing grade on oil. To go to Saudi Arabia but not Texas is just stupid, forgive me

5. Russia. Russia was a massive failure of deterrence by the Biden administration, just as I wrote in “Let Putin Buy Crimea”. Do you think Putin would have invaded if he knew things would turn out this way? I don’t think so. Biden should have made plain that the US would meet the Russians in the field, and then we wouldn’t be in this colossal mess.

6. Stimulus and monetary policy. Complete clusterf**k. Total misdiagnosis of the problem and unhinged policy as a result. Biden and the Democrats will be buried by their own supporters as a result. Very, very poor analysis by the Fed, Treasury, CEA and others. Did no one point out that a gargantuan stimulus might reverse into a technical recession heading into the midterms? Where was that analysis?

7. Too much emphasis on wokeness. This has alienated moderate whites and, in particular, Hispanics. Not a few blacks, either.

Biden has made one egregious policy error after another. That’s why he’s -16.2 this morning.

I am no more cheering for recession than your doctor would be cheering for cancer.

The vast majority of economists were willing to give corporate America a total pass on their contribution to inflation. (Quelle surprise!)

New research suggests what most Americans already knew…that market power was being opportunistically exploited to exacerbate inflation.

Mike Konczal, one of the paper’s authors, who is the Roosevelt institute’s director of macroeconomic analysis,was asked: “Is greed the sole or main reason for inflation?” He responded, “II’d say no. It’s part of the mix of explanations that should be under consideration.” The authors’ found that, after adjustments for size, companies that increased prices before 2021 were the most likely to increase prices in 2021. That indicates that they had a position in the market that made it easier for them to impose price increases and make them stick.” https://www.nytimes.com/2022/06/22/opinion/inflation-corporate-profits.html

You know we have enough of Princeton Steve’s BS and how we have to endure yours? OK, it is a comical break.

JohnH,

The problem with your post is that while indeed there looks to have been an increase in corporate market power, this has been a gradual process, although with some particular industries where it has gotten especially worse, e.g. baby formula. But in general, frankly, the amount of corporate market power is only moderately greater than it was two years ago, at which point inflation was still holding near the low levels it was for a long time. Inflation has jumped very noticeably, and around the world, not just in the US, so it does not seem to be tied at all to the fairly modest increase in corporate market power.

Your problem is the opposite of that of Steven Kopits with his efforts to revive old-fashioned monetarism. He wants to blame the increase in inflation on increases in money supply. But we have seen really huge increases in money supply, which have not been matched remotely by an increase in the rate of inflation.

I was asked to comment about some Dutch transfer pricing decision regarding fertilizer. I think I posted a really great Ag Econ paper on the recent price increases. If you get a chance to read the paper in my link, pay a lot of attention to CF Industries. Their abuse of market power is indeed part of the current problem.

I think you and I would agree that certain sectors need a little anti-trust action even if the anti-inflationary impact would be puny.

There is also the Jeffrey Frankel solution, increase imports for some of these sectors. This varies from sector to sector, but I agree we could use some more vigorous anti-trust enforcement, even if it is a fantasy on the part of the seriously delusional JohnH that this will have a big impact on inflation.

I just checked Peter Coy’s bio (the author of this shlock in JohnH’s NYTimes link):

Peter Coy is economics editor of Bloomberg Businessweek. He writes on a wide range of domestic and international issues. He contributes to the magazine’s Opening Remarks column, cover stories, news section, and online coverage. He also appears frequently on radio and television. Mr. Coy joined BusinessWeek, the predecessor to Bloomberg Businessweek, in 1989 as telecommunications editor. He became technology editor in 1992, associate economics editor in 1997, and economics editor in 2001. He came to BusinessWeek from the Associated Press, where he worked from 1980 to 1989 in Albany, Rochester, and New York. Before that, Mr. Coy was a reporter for the Waterbury (Conn.) Republican. Mr. Coy holds a B.A. in history from Cornell University.

Majored in history and has worked as a journalist. But JohnH thinks he is an economist? DUH.

I think I mentioned this once before, but way back in the beginning of time I had an econ professor who used to (jokingly…I think) bow his head and make the sign of the cross whenever he would write MV=PQ.

I’ve said for a long time my nightmare is to be mentioned in a Menzie Chinn post in a negative way. Same as a a dream to be mentioned in a positive way. I’m not “fishing” here, just putting out internal thoughts. That gained by “fishing” would be nearly as bad as the nightmare. Anyway… maybe with “R” program some day, Everyone should keep on dreaming and have goals.

Moses,

You have been fortunate not to be featured negatively in a main post by Menzie here. But he has had to correct you quite a large number of times on various items, with many of those having to do with false or exaggerated claims you have made about me. Does this happening so often not sort of send a message to you aside from you once claiming that he and I were in cahoots being fellow academics? That one was truly worth an LOL.

Princeton Steve struggles with why economists use natural logs to evaluate growing series over a long period of time. He also has this weird fascination with the discredited Quantity Theory of Money to the point of writing this nonsense:

‘That model makes absolutely no reference at all to M2, does it? You could increase the money supply tenfold and it would have no impact on inflation, as I understand the construct. Is that right? Do you believe that’s true?’

Of course one would have to realize that velocity has fallen a lot since the Great Recession. And one would realize that even under more ordinary periods, a rise in the money supply would not only increase real output if we were below full employment but lowering interest rates, which of course would tend to reduce velocity. But forget all of that as Stevie never understood basic economics. Let’s take this as a learning moment with respect to natural logs.

Over the period from 1950 to 2018, the consumer price index did rise tenfold from 25 to 250 (approximately). Now let’s imagine the inflation rate was around 2% at the beginning of this 68 year period and was 2% at the end of the period. Now Stevie insists on drawing all graphs in linear not log fashion. Just think about it – his graph shows prices rising by 0.5 in the first year of this period and by 5.0 in the last year of this period EVEN THOUGH inflation rate was 2% for both years. Now that would be one misleading graph. Even a 2 year old would understand that but to date, this has escaped Stevie’s comprehension.

It matters. If you think the inflationary impulse comes principally from the stimulus and supply side effects, then the Fed raising rates willy-nilly is going to be a disaster.

On the other hand, if you think monetary policy is driving inflation, then raising rates is the right thing to do. But then you may be compounding a technical recession from the roll off of stimulus with a cyclical recession arising from increased interest rates. That may be the price you have to pay.

I am personally not sure which factor matters more. Yesterday at Stop ‘n Shop my bellwether avocadoes were back at the pre-pandemic $1.66 / avocado, and navel oranges, now of out season, were down 20% in price. Is this purely a seasonal issue, or does it mean that inflation was principally associated with the stimulus and supply-side effects?

In event, this is far from an academic debate. If Powell has got it wrong, the Fed will crater, well, it’s already cratering, the economy.

You repeated this worthless comment? See my reply to your first version of this garbage.

Pilots in line for big raises amid global travel disruptions

https://apnews.com/article/airlines-25a0c34e9ba60dd358c680d7b1edffc9?utm_campaign=SocialFlow&utm_source=Twitter&utm_medium=AP

14% over 18 months. What inflation rate does that imply? 9%, it would seem.

Oh gee – the market increases the wages of some group of workers. I guess in your weird world, this is the advent of COMMUNISM.

“United CEO Scott Kirby called the deal an industry-leading contract that would help both the union and the airline.”

Gee – this CEO is not saying airline prices will be rising by 14%. That is because he knows that the pay for pilots is a small percentage of the cost of operating an airline.

I guess based on your comment – you think pilot pay is nearly 100% of the cost of running airlines. Which would make you the dumbest troll ever. But we already knew that.

Professor Chinn,

I wonder if you would share how to create the meandering “orange” line in figure 2.

I am trying to look at a correlation similar to figure 2, in which the growth of real GDP over the growth of potential real GDP is compared to PCE changes. I have used Q/Q(-1) for first pass. Just pondering if “excess” money supply growth when real GDP growth is above growth of potential GDP can stimulate demand and thereby cause inflation. Does that thought conflict with the tautology comment?

AS: set SMPL 59.1 2019.4 if Q4=1, then SHOW the the change in M2/GDP and inflation, then choose to show graph, scatter with Nearest Neighbor option for fitted line (instead of regression line).

Professor Chinn,

Thanks.

If I had looked at the graph options carefully and seen the “nearest neighbor” would not have needed to ask (tunnel vision).

Since I had trouble with the use of Q4 only, I went to FRED and used annual data with the end of period option and have the same chart as yours.

Need to do more thinking on how to approach the gap analysis of GDP and potential GDP.