Here are some some observations to complement Jim’s post on the GDP release .

- Final sales (i.e., excluding inventory accumulation) show a different picture than GDP.

- Gross Domestic Output and GDP follow different trajectories

- GDP follows a different path from other key indicators

- Economic activity appears to be geographically broadly based

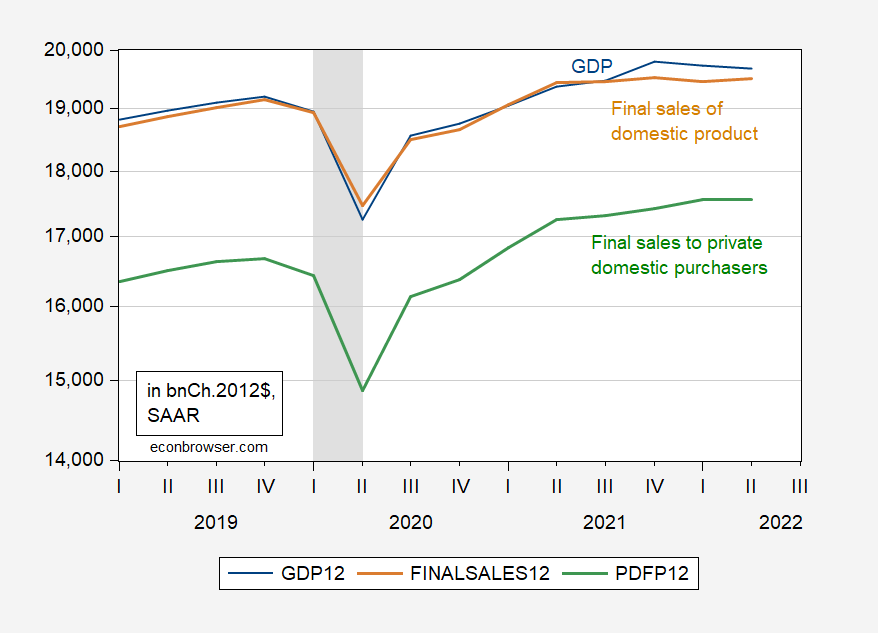

On the first point, GDP is higher than final sales of domestic product (GDP minus inventory accumulation), but has a different gradient in Q2 — increasing rather than decreasing. Final sales to private domestic purchasers, which is sometimes used to infer intrinsic domestic demand, was flat.

Figure 1: GDP (blue), final sales of domestic product (tan), and final sales to private domestic purchasers (green), all in bn. Ch.2012$ SAAR, on log scale. NBER defined peak-to-trough recession dates shaded gray. Source: BEA and NBER.

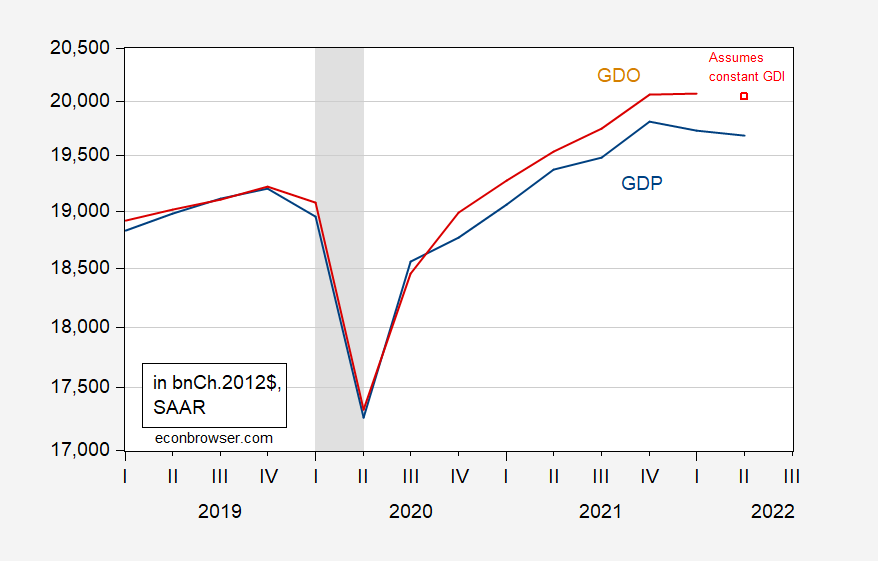

What is the actual level of economic activity, the “Y” in macro models? GDP measures it from the expenditure side, while GDI measures it from the income side, and the two should equal. The disparity in Q1 was at record levels; In Q2, we don’t yet have GDI, but if real GDI was flat (as real personal income excluding current transfers was), then, we have the following picture:

Figure 2: GDP (blue), GDO (red), and GDO assuming real GDI constant in 2022Q2 (red square), all in bn. Ch.2012$ SAAR, on log scale. NBER defined peak-to-trough recession dates shaded gray. Source: BEA, NBER, and author’s calculations.

Then GDO declines in Q2, while being essentially flat in Q1. (GDI and personal income follow each other fairly well.) Why does this matter? As Furman (2016) notes:

It turns out that an equal-weighted average of the [GDP and GDI] is close to the optimal way to combine them, since the average of GDP and GDI more closely tracks the most up-to-date estimates of GDP growth and is a better predictor of future economic growth than either GDP or GDI alone.

This observation backs the view that, in future revisions, reported GDP will likely be revised upward.

Finally, recognizing that GDP is going to be revised numerous times as additional data comes in, what do other indicators suggest is happening to economic activity?

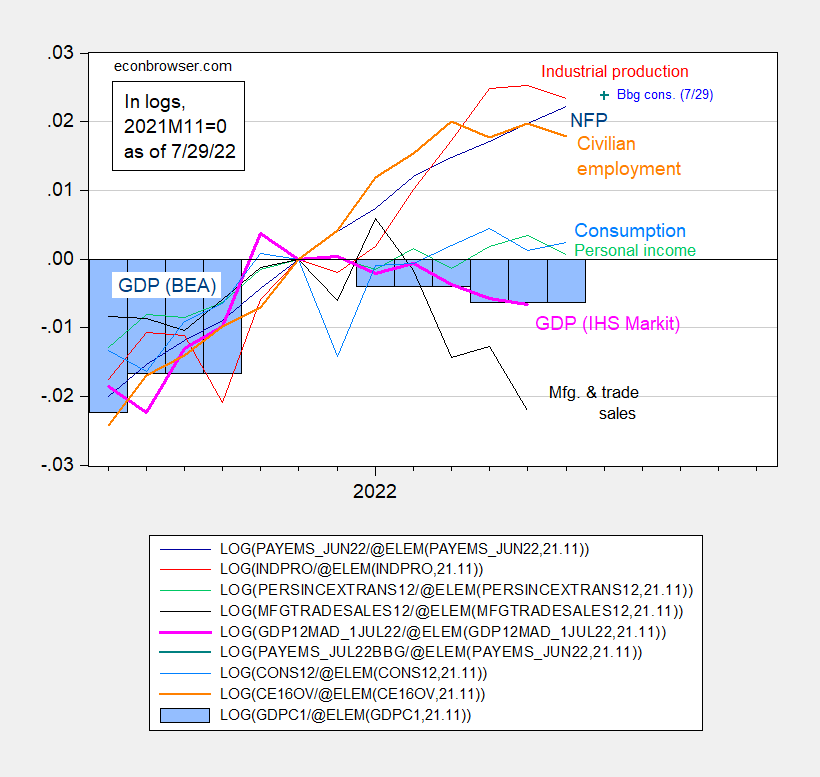

Figure 3: Nonfarm payroll employment (dark blue), Bloomberg consensus as of 7/29 (blue +), civilian employment (orange), industrial production (red), personal income excluding transfers in Ch.2012$ (green), manufacturing and trade sales in Ch.2012$ (black), consumption in Ch.2012$ (light blue), and monthly GDP in Ch.2012$ (pink), official GDP (blue bars), all log normalized to 2021M11=0. Source: BLS, Federal Reserve, BEA, via FRED, IHS Markit (nee Macroeconomic Advisers) (7/1/2022 release), NBER, and author’s calculations.

It’s clear that many indicators have continued to grow past the putative peak of 2021Q4 that one would get based on GDP data as currently reported. The two most highly weighted series — nonfarm payroll employment and personal income excluding current transfers — have diverged from GDP, most profoundly for the former.

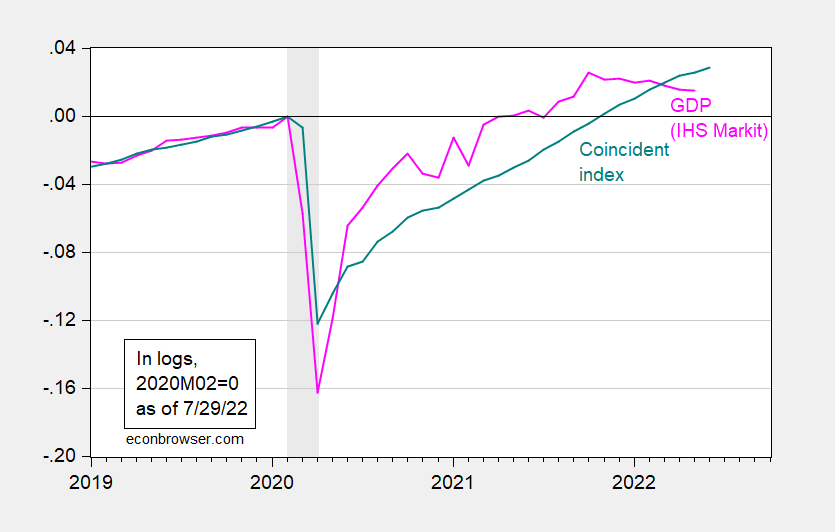

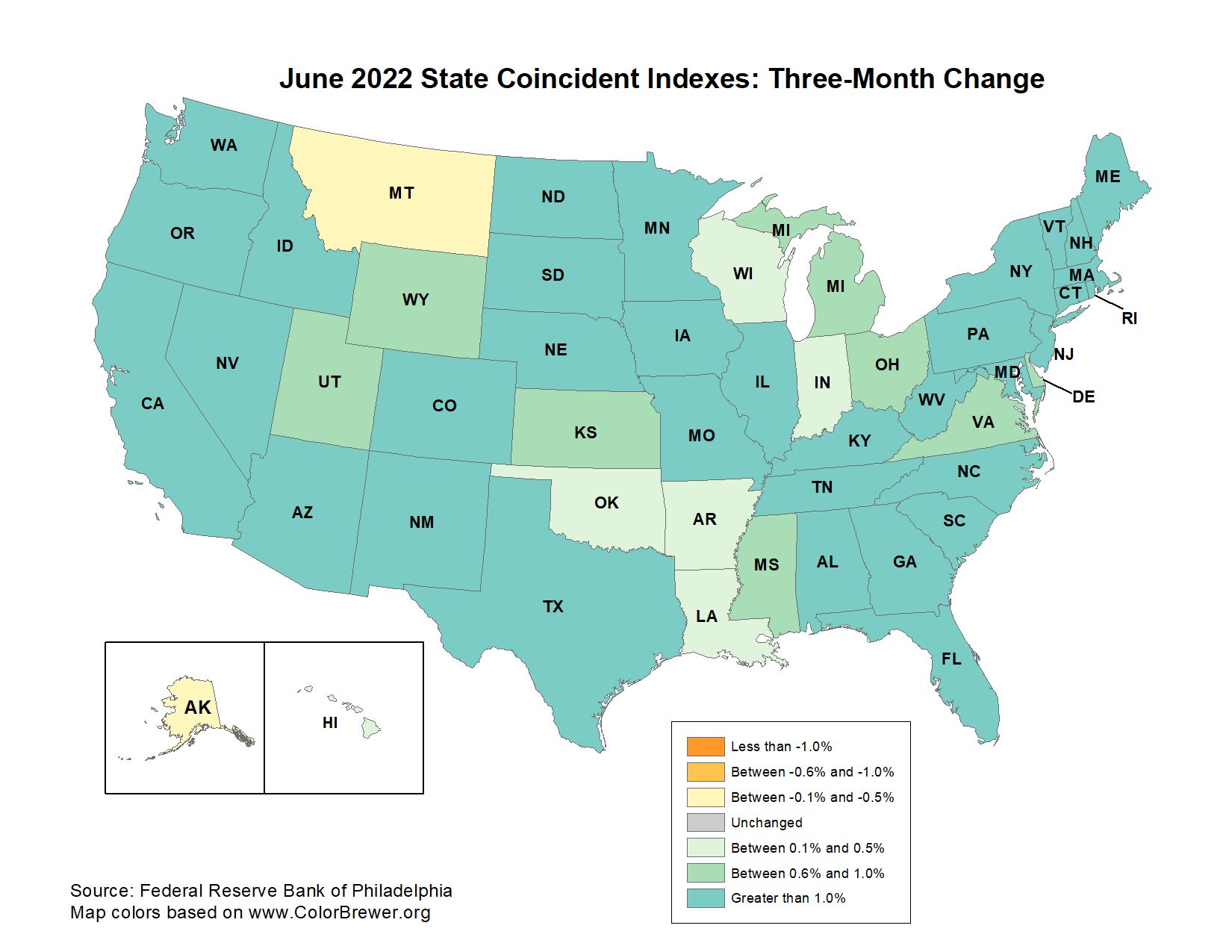

Other indices also point to a different path than GDP. Here’s the Philadelphia Fed’s coincident index compared to IHS Markit’s monthly GDP.

Figure 4: Monthly GDP in Ch.2012$ (pink), coincident index (teal), both log normalized to 2021M11=0. Source: BLS, Federal Reserve, BEA, via FRED, IHS Markit (nee Macroeconomic Advisers) (7/1/2022 release), Philadelphia Fed, NBER, and author’s calculations.

It’s of interest to note that geographically, economic activity as measured by the coincident index has been rising over the last three months (so, 2022Q2) all across the Nation, save Alaska and Montana.

Source: Philadelphia Fed, accessed 7/29/2022.

The Baumeister et al. Weekly Economic Conditions Indicators (data through 6/25) agrees on a slowdown in Alaska, but not for Montana (Utah is in the doldrums according to WECI).

All in all, reading beyond the headlines, economic activity seemed to continue to increase through Q2.

Final sales (i.e., excluding inventory accumulation) show a different picture than GDP.

Gross Domestic Output and GDP follow different trajectories

GDP follows a different path from other key indicators

Economic activity appears to be geographically broadly based

Wait – the RECESSION cheerleader trolls scored this Stevie 1 Menzie 0. No – when all indicators are taken into account, I score this Menzie 4 Stevie 1. We need better referees.

That’s the ticket. If you don’t like how the game is called, change the refs.

It’s not a contest. It’s properly trying to estimate outcomes for reasonable policy decisions. I don’t recall, Menzie, that you actually made a call on Q2 GDP one way or another. You introduced a bunch of different metrics, IHS, GS, AF, etc., but I don’t recall that you ever took a definitive position on the matter.

And again, I have no particular genius or insight beyond 1) thinking a record low cc number likely coincided with some sort of recession, 2) having some confidence in the modeling of IHS and AF, given that these are dynamic, articulated models which are a) a revenue-generating product for IHS and b) a core competency for the Atlanta Fed, and therefore both likely to be of pretty good quality. (Goldman Sachs, by the way, does not sell macro forecasts. It sells securities, which is a quite different business.)

By the way, since the -0.9% GDP number, Biden’s net approval is up nearly 3 pp and the Dem’s prospects in the Senate have solidified. The only real ‘achievement’ of all this bruhaha about it’s-not-a-recession has been to undermine the credibility of likes of Frankel and Yellen with the public.

Steven Kopits: First, Frankel did not hang his hat on a positive reading. In fact his entire post was about how negative Q2 reading was not directly material to whether NBER called a recession (you have the 1947 episode, and the 2001 episode, to verify this is not an empty assertion). Janet Yellen did not assert Q2 would be positive either.

In fact, if you recall, I wrote (since you could not figure out how to incorporate the mean error vs. RMSFE numbers):

So, GDPNow adjusted was -0.8%, vs -0.9% advance. I didn’t say GDPNow adjusted was worse or better than St. Louis Fed. I indicated that both had RMSFEs sufficiently large that conventional prediction intervals encompassed 0%.

I suppose I should apologize to both you and Professor Frankel. I made what was mostly intended as a self-deprecating joke on how I hate to be wrong about things, and I am afraid Kopits took what was 80% intended as a self jab, and ran with it. Anywayz….. I am sorry about the whole thing, and feel Professor Frankel was pointing out how even knowledgable people really didn’t know where it was going to go. I was the dummy that attempted to act like I knew 95% which side of positive or negative it was going to go and in fact had no gauge.

The credibility of Yellen and Frankel? Is this Know Nothing Arrogant troll kidding me? And Stevie gets all frustrated when we call him on his lies and stupidity saying we should have “civilized” discussions. I guess he defines civilized means shining his little shoes.

Maybe you should try this.

Funny boy.

You just enjoy getting under people’s skin, don’t you Don?? pointing to a pedophile cult hardly registers on my gaug. Shows effort on your part though. It really kinda makes me laugh as I’m listening to Mastodon here;.

“That’s the ticket. If you don’t like how the game is called, change the refs.”

No you changed the refs by saying only metric needs to be considered. Then again I have never accused you of being honest.

“Goldman Sachs, by the way, does not sell macro forecasts. It sells securities, which is a quite different business.”

But its forecasting record is part of its marketing strategy. Since you are trying to market your consulting “services” by claiming you are a great forecaster, then you should get this. But wait – no one can track your forecasting record because you do not keep a database of your forecasting record. Smart move on your part as I bet your forecasting record is horrific.

I don’t sell macro forecasts. But I have worked at an investment bank, and I have a very clear notion of the pressures on analysts in those institutions.

Stevie…? You have evidence that the public has lost faith in Frankel and Yellen? I kinda think you made that up, but please let me know if you have evidence.

I relied to Moses meaning to reply to your comment. Sorry about the confusion. Look it is clear that Frankel and Yellen are both honest and smart whereas Stevie lies a lot to cover up the fact that he is dumber than a rock. Yea he might whine I’m not being civilized but we all he is the MOST DISGUSTING TROLL EVER.

We’ll, they may not have changed the refs, but they are sure hoping that the call will be delayed until after the midterm elections, barely more than three months away!

Saved by NBER’s not making preliminary calls. And obviously this group of partisans think that it’s unthinkable that the common shorthand for a recession—-2 quarters decline in GDP—qualifies at all as a preliminary call!

JohnH,

I remind you that Robert Hall does not think “the common shorthand” qualifies as meaning one has a recession. He is a Republican who served on Reagan’s economic transition team in 1980 and is at the conservative Hoover Institution. He has also served as the Chair of the official NBER Business Cycle Dating Committee, yes, the people who actually determine when we have recessions and when we do not, the people who have decided that the two quarters in 1947 when GDP declined while emploiyment rose, like what we have just seen for the first two quarters of 2022, was not a recession.

This has already been noted here by me, but you either do not read what is posted here or are engaged in third rate stupid lying like usual.

Did Martin Feldstein ask this group to move the date of calling recessions for St. Reagan? Oh wait – you have no clue who Feldstein even is – do you?

As I pointed out earlier, the discrepancy between economists’ view of the economy and people’s view can be easily explained. While liberal economists are emphasizing that “the economy” is technically not in a recession, other data indicates clearly that the average worker is clearly experiencing a recession. After years of positive growth, media usual weekly real earnings are now down to only 1.7% above where they were at the end of the Obama administration.

https://fred.stlouisfed.org/series/LES1252881600Q

Yet economists largely ignore the situation of the average worker and prefer to emphasize “the economy.” Why is that?

“ All the hand-wringing this week over whether or not the U.S. economy has fallen into recession lacked an important consideration: What if the measure of GDP we’re all focused on is itself massively flawed?

It’s a heretical question, because there’s a ‘GDP complex’ at work here.

There’s an entire apparatus — economists, bankers, government officials, and prognosticators — of folks whose livelihoods are predicated on measuring GDP, maintained as the be-all and end-all method for measuring a country’s economic, or even societal, health.” Yet again the plight of the average American gets short shrift.

https://finance.yahoo.com/news/gdp-complex-economic-growth-morning-brief-110032965.html

Mohammed El-Elian:

“[GDP] is a shortcut, it’s not comprehensive enough,” economist Mohamed El-Erian told me recently. “It’s a cognitive trap. We’ve all gotten used to measuring things by GDP, and we’re having a huge problem getting out of that. Also the nature of GDP growth is important. Is it inclusive? It’s a useful measure, but it is just a tiny perspective into an economy.”

Instead of just obsessing about GDP, which mostly measures how the wealthy and affluent are doing, since they gobble up the bulk of income, economists could dedicate more of their energy to how the average American is faring.

“While liberal economists are emphasizing that “the economy” is technically not in a recession, other data indicates clearly that the average worker is clearly experiencing a recession.

Dude – smart economists realize we are not in a recession. If you had read what our host has written, you might realize this. BTW people like Martin Feldstein and Robert Hall are not exactly liberal. But they share two things in common that you totally lack – intelligence and integrity.

BTW liberal economists do get that real wages are falling of late. When you say they do not – you are lying I presume. Then again you are too stupid to read.

pgl: look at the headlines on economists’ blogs. I bet the ratio of GDP to real wages is 50:1…it’s probably the same ratio for interest rates to real wages. Yet pgl asserts with no basis whatsoever that most mainstream economists care deeply about workers and their prosperity!

“JonH

July 31, 2022 at 12:55 pm

pgl: look at the headlines on economists’ blogs. I bet the ratio of GDP to real wages is 50:1”

I guess you never get past the headlines after all. Pity. Labor compensation/GDP is only 2%? You lost that bet big time. Now if I bet your IQ is in the single digits – I would win.

China Johnny,

You just keep saying this stuff, but saying it doesn’t make it true. GDP is not a totem at which economists worship. Economists study all the things you keep wishing they studied, and lots of other things about which you have no conception. Notice it is our host, the economist,, who regularly posts about real income and consumption and about employment. It is non-ecinomist MAGA cheerleaders who have been cheering for a decline in – come on, China Johnny, you’ve got this one – a decline in GDP.

El Erian thinks GDP is a cognitive trap? So does the NBER. So, apparently, does our host. So do those of us who have been pointing out other measures.

Yet who do you howl at? Not the Trump puppets who have been cheering for a decline in the economy, however described. You howl at the very people who actually think the way you, in your own misguided way, want them to think.

And this new favorite mistake of yours, insisting that individual people have individual recessions? That’s hyperbolic claptrap. The underlying point of the whole debate over recession is about definitions. Discussion becomes meaningless if we don’t all mean pretty much the same thing with the words we use. Now here you are, making up your own meaning, so you now at economists.

So no, China Johnny, people don’t have personal recessions. Economies have recessions – people suffer from them.

MacroDuck: still can’t wrap your head around the fact that your multitude of indicators show growth, but that Median usual weekly real earnings are in the toilet, can you? Can’t admit that for the average American worker, it is a recession, since real earnings are fast declining into Obama times, can you?

Typical limousine liberal…

Steven,

Talk about snatching defeat from the jaws of victory!

This isn’t a contest? It is a contest to Menzie and the other commenters. If the 2Q GDP number had been positive, Menzie would have put up a post ridiculing you by name. Worse, you let him off the hook by saying “I don’t recall you making a definitive call” when he wrote a bazillion posts challenging your view, but carefully avoided saying anything too directly so that he’d have deniability in case you turned out to be right.

Then, you undermine your own forecasting skill, saying you have no particular genius or insight. I suppose you thought that if you don’t take a victory lap, he’ll respond in kind. But he responded with another insult.

Of course he did. That’s always going to be true. Menzie doesn’t respect you at all and thinks you have nothing useful to say. He believes that only people with PhDs and publications know anything about the economy or markets. He thinks consultants are charlatans and resents that they get paid anything, He wants to knock you down publicly and is happy to hurt your business. He will never take you seriously.

But Menzie lives in an academic bubble. In the real world, consultants with actual (not academic) experience can make multiples of an academic salary, as you well know. I have direct experience here, having paid quite a lot of money over the years hiring consulting firms for various projects. In general however, academic consultants are pretty useless. You generally need to hire people at the top of their fields and even in that case many aren’t worth the money. I’ve had some very good experiences hiring academic consultants and some bad ones too.

This blog has very few commenters left. It should have one fewer.

“you undermine your own forecasting skill, saying you have no particular genius or insight.

You are one funny dude. Tell us Rick – where do we get a list of his forecasts so we can measure how reliable they are? Oh wait – there is no such list as Stevie does not bother. It is a good thing as his forecasting skills are even more of a joke than your stupid comments.

“I have direct experience here, having paid quite a lot of money over the years hiring consulting firms for various projects.”

I see you decided not to tell us what these projects were. Oh that’s right – you paid big bucks for climate change denial reports. Or how tax cuts for the rich lead to faster long-term growth. Got it!

Why would I tell you what the projects were?

Rick,

Steven certainly turned it into a contest when he challenged people like me to definitely make a forecast, which I refused to do based on what looked to me like major uncertainties about crucial variables, especially those notorious inventory changes, which Steven avoided saying much about, but which in the end, as I did forecast, drove the result on GDP, although some of my discussion of them was itself confused. Indeed, most people here avoided talking about them, a supposed tail on all this, but one that seems to have wagged the dog in recent quarters. I note Macroduck, and AS a little bit being the only people here besides me to discuss them much prior to this recent data release.

I am an academic, but I have also done some consulting as well, although have not made lots of money doing so. Sure, one can make more doing it than being an academic and probably also hiring consultants as you claim to have done. But I do find some of your comments on this highly disingenuous. You dumped on me for “moving goal posts” when I noted that Steven was right for some wrong reasons. My experience with consulting is that clients not only want right answers, but they want reasonable analysis supporting what one says. On that Steven delivered a mixed bag.

So, one item not mentioned much at all that he was right about was the ending of the fiscal stimulus. I do not know how much of a role it played, but it may be part of why we saw a decline in local government spending during Q2, one of the other negative items besides the decelaration of inventory changres. So, points on that one. Of course he has bragged about being right about inflation not being transitory and assigned blame for that at least partly on the now defunct ARP. Hmmm.

Where ha was most egregiously wrong was on consumption, especially on his claim put forth art one point that we were clearly in a recession now because of a super low reading of the Michigan consumer sentiment index. This was just rank nonsense, and many here called him on that one, including Menzie. It is indeed among the odd things going on that we continue to see consumption still holding up, even as that index is so low. I have no explanation for that.

I note that Steven tends to avoid making probabilistic statements, which is probably wise for consultants who want to make money. This may be why he avoided the topic of inventory changes in his forecasting, given how totally squirrely and weird they have been behaving. It also led him to make a wrong forecast, since people are keeping score, last year on crude oil prices. He said they would top $100 barrel, and he got lambasted by pgl and Moses that they did not get much above $80 by the end. I was lambasted also, especially by Moses, because I allowed that Steven might be proven right, although I was emphasizing the wide range of possible outcomes, including that the price might go below $40. The EIA right now has a 95% confidence interval for the next six months of from below 40 to above 200, but paying clients do not want to hear about that sort of thing much.

BTW, I agree that there have been various parties on both sides of this debate who seem to have taken their positions based on their political biases, although some of them avoided making specific forecasts rather than simply pushing one forecast or argument or another. Regarding Menzie, while he indeed criticized a lot of Steven’s arguments, usually pretty competently, he presented a range of forecasts that he did not choose among, and with those increasingly trending to a negative Q2 GDP outcome as the date of the announcement approached, which he noted.

Barkley,

My main point is that there is a fundamental clash of cultures here. Economists and market analysts who work for financial institutions just make point forecasts. They don’t talk about confidence intervals or engage in on-the-one-hand, on-the-other-hand analysis. The point forecasts don’t have to be on-the-money accurate, but they do need to get the basic story correct ($100 vs $80 may not matter practically) to have investable implications. SK is often frustrated with Menzie because no one in the real world of finance and investing can use the type of analysis Menzie does. That’s why SK said that if you don’t like his forecast, then what’s yours? It’s not that he’s starting a contest. It’s rather a refection of how someone who is focused on the markets thinks. Conversely, Menzie thinks that anyone who doesn’t take an academic point of view when analyzing the economy is an ignorant charlatan. SK has become the econbrowser pinata as a result. That’s not going to change.

It’s not forecasting skill, Rick, it’s judgment about sources of data. I know something is up whenever I have to re-scale a graph, which typically involves new highs or lows. A record low Mich cc number strongly suggested a recessionary impulse in the economy. That’s where this whole topic started in late June.

My interest is in good policy, not in winning or losing. I have castigated the staff of the Fed for having signed off on a gargantuan M2 increase by without so much as a peep. Let me apply that rule to myself. For me, the principal mission of an economist is to call the balls and strikes as he sees them: truth to power. When people like Frankel fail to do that, that is, to apply a standard without declaring their allegiances, then the public’s confidence in the profession as a whole will be undermined. When the powerful feel besieged and powerless, believe that they can enjoy the unchecked rhetoric of a clerk at grocery store, then bad things start to happen.

Then, science and analysis will itself be called into question, for those disciplines will be seen not as expertise to be deployed in the service of society, but as a cynical veneer, weapons in class warfare to be wielded by the rich, the sophisticated and the educated against the middle class. That’s the motivating impulse behind the burning of the books during the Nazi regime, because those works were perceived to be the tools of oppression, not the path of enlightenment.

Nevertheless, those books do contain knowledge and the experts, in many cases, are expert. If society rejects both its experts and its books, well, it is headed towards a dark place. History shows the world can remain dark for a long, long time. Perhaps that is the default setting. The experts themselves must determine whether they stand for impartiality and expertise, or merely as the sword and shield of political combat. This is not to say that one cannot be partisan. If I watch MSNBC, I expect a certain spin, as I do on Fox. But CNN? The New York Times? These claim to be above the fray, and yet are partisan to their core. All that does is erode credibility, and CNN has been absolutely hammered as a result of it.

The economics profession is now in the situation of CNN. It is not credible on the whole, certainly not from the talking heads. Here’s the thing: By the most commonly accepted standard, H1 2022 was a recession, and 65% of the public believes the country is in recession. And yet how much ink has been spilled to demonstrate that a recession is not a recession? Goodness, Menzie must have twenty posts by himself, the gists of which are 1) to deny that a recession by the most common standard is a recession and 2) to highlight that those 65% of the public who think we are in recession are stupid and unable to judge matters for themselves. Is this a winning hand, or does it merely hammer home to two-thirds of Americans that economists do not have their best interests at heart? I think it is the latter, and I think it fits a pattern we’ve seen before, chronically during the Biden administration, with the out-sized stimulus, with the uncontested surge of M2, with non-transitory transitory inflation, a non-recession recession, and most recently with the Russian oil price cap, which is moronic to its core and cynical in its pursuit. To many in the public, that is what the economics profession, with Larry Summers the material exception, means right now. It means serial, egregious incompetence and dissimulation. I think that’s a bad thing, and I think economists either need to declare their colors or hold their allegiance with the profession rather than ideology or party.

And so it is with me. I confess to a lack of sufficient team spirit. But real things actually happen to real people, and whether the Treasury or Fed blow their mandates matters to literally billions of people around the globe. For me, duty has meaning beyond victory or defeat in debate.

—————————————

https://www.msn.com/en-us/news/opinion/economist-slams-facebook-for-absolutely-orwellian-fact-check-upholding-biden-s-recession-denial/ar-AA10bzqU?ocid=msedgdhp&pc=U531&cvid=ea9e87f4135340d9a808864d4e2a29d4

https://www.politifact.com/factchecks/2022/jul/27/instagram-posts/no-white-house-didnt-change-definition-recession/

https://freebeacon.com/media/chris-lichts-republican-apology-tour/

Growth is slow and has slowed. Whether the actual GDP number is a little over or a little under 0 is of no real world consequences – and pretty much impossible to predict with any certainty. If not for inventories taking 2% of GDP in Q2 we would have had a +1% rather than a -1% number.

What you are doing is a lot more useful. Consumption and personal incomes are not looking great – and if industrial production is mostly from filling up inventories then the overall picture would be of an economy in the plus/minus 1% GDP range. Not bad given that a substantial stimulus has run out and the pandemic is still lingering. The saving grace that will keep us from any meaningful downturn is the continued shortage of labor and the beginning turn around in inflation. It looks like we soon will get back to salary increases being equal to or higher than inflation – that will prevent our consumption driven economy from turning down.

Under the competent leadership of Biden the bumps are slowly being ironed out.

Ivan, Under the incompetent leadership of Biden the small bumps are quickly converted to hills and mountains. There fixed it for ya. 😉

I guess you stopped trying to make an informed comment years ago.

You mean “politicized it for ya.” Yeah, we all wait with bait on our breath, hoping to hear you MAGA the palace up.

“It looks like we soon will get back to salary increases being equal to or higher than inflation – that will prevent our consumption driven economy from turning down.”

I certainly hope so. But here is one irony. Some are glad that nominal wage growth is low because that will keep inflation from staying high. The real trick is to get price inflation to drop below wage inflation – not the other way around.

“ It looks like we soon will get back to salary increases being equal to or higher than inflation.” Dream on. More likely that real wages will continue to decline back to the Obama years…and maybe more. We’re not that far above Obama era wages right now.

You really hate the fact that a black was once President. How does that MAGA hat look on you?

Agree, and the reasons I have hope it will happen are many.

1. We currently have a competent President who want more money to the consumer class and less monopoly pricing power to big business (not a GOP clown President who wants the opposite). Most of the things he needed to do for that, are already done – or at least cannot be blocked by a presumed obstructionist GOP congress coming to US next year

2. With unemployment being under 4% and many claiming labor shortages, it would be very hard to push wage inflation down.

3. The kinks in the supply chains have mostly been ironed out, so stores/companies have been forced to build up inventories and reduce prices (on a much improved flow of products). That will be further enhanced by all the yelling and moaning about recession (since a lot of consumers tend to reduce spending based on such words, not their own reality). Add to that the evaporation of demand in single family housing markets – and you have a perfect setting for drastic reductions in inflation (if not outright deflation – yes I said that word).

4. The Feds misguided over-reaction will reduce prices. Although most of the current inflation is caused by supply chain issues (that are being solved regardless of the Fed) – higher rates always have some calming effects on prices. Although Fed rate increases can have a huge and immediate effect on mortgage rates and inflation, it would take a long time for that policy to shut down current labor shortages (and associated wage increases).

5. Biden’s economic team seems to understand that labor shortages are a good thing that should be enhanced via Federal policies (and spending) – not suppressed and solved in Wall Street’s favor.

So yes I do have hope – and in contrast to the right wing blabber that regularly pollute this page, it is based on observable realities.

As I commented earlier, we may not be in a recession, but perhaps this is just a “pause in positive growth”.

In other news, inflation seems to be an issue that won’t quite go away and may hit consumers differently this fall in the form of significantly higher food prices. Greg Mankiw wonders about our inflation:

http://gregmankiw.blogspot.com/2022/05/an-inflation-puzzle.html

Additional info: https://www.cnbc.com/2022/07/21/bank-of-japan-raises-inflation-forecast-keeps-policy-steady.html

Waiting for pgl’s snide comment about how Mankiw is a twit and how stupid I am to reference him.

You actually read Greg Mankiw? An upgrade from your usual BS sources. OK it is interesting question which I would love to provide a comment to over at Greg’s blog. Oh wait – he cut off the comment section. I guess this Harvard economics got tired of dumb comments from you.

A little research that took me like 10 seconds and now I’m a bit disappointed at Mankiw who is an eminent macroeconomist. First of all we have seen a massive appreciation of the yen of late which tends to offset inflationary pressures. Now interest rate have not increased so I cannot say they have run tight money but everyone has known since like 25 years ago that Japan suffers from weak aggregate demand.

Now I would expect Mankiw would get this. Of course Bruce Hall could have done this research but yea – he still have no clue what any of this is about.

Recent info:

https://money.usnews.com/investing/news/articles/2022-07-29/japans-inflation-not-mainly-caused-by-weak-yen-adbs-asakawa-says

Japan’s Inflation Not Mainly Caused by Weak Yen, ADB’s Asakawa Says

By Reuters

|

July 29, 2022, at 3:21 a.m.

TOKYO (Reuters) – It goes a step too far to say a weak yen is the main reason for explaining why prices in Japan are rising, Asian Development Bank (ADB) President Masatsugu Asakawa said on Friday.

The major factors for the price rises that Japan is seeing are pandemic supply chain disruptions and surging food and energy prices due to Russia’s invasion of Ukraine, he said.

Rising consumer prices are a politically sensitive issue in Japan, because they challenge the view of the Bank of Japan (BOJ) that recent price hikes in the country will remain somewhat temporary. They can also be a cause for discontent, especially among low-income earners who worry about higher living costs.

Core inflation, which excludes volatile fresh food costs but includes those of energy, has topped the BOJ’s 2% inflation target for three months in a row, government data showed this month, coming in at 2.2% in June.

“It’s probably an overstatement to say that it (the gradual rise in prices) is due to the weak yen,” Asakawa said during a news conference at the Japan National Press Club.

While a weaker yen has contributed to Japanese inflation, only about 20% to 30% of the inflation rate could be explained by it, Asakawa said.

Asakawa, who has headed the ADB since 2020, is seen by market participants as a potential successor to BOJ Governor Haruhiko Kuroda, whose second five-year term will end in April next year.

Before retiring from the finance ministry, Asakawa served as Japan’s top financial diplomat for four years from 2015.

I know it’s two day’s old, but we’ll have to live with that. Anyway, your strong yen; his weak yen. We all yen for the truth.

Did you even remotely understand what he wrote. As I noted, Japan has seen rising prices of late. Mankiw missed that but then his blog post was back in May. I guess Bruce Hall is too stupid to get it is now late July and the BS he tried to peddle has turned out to be a lie.

BTW troll – no one ever said exchange rates were the ONLY factor. Aggregate demand has something to do with at as both Macroduck and I pointed out.

Come on dude – please stop posting your outdated and stupid comments until you learn to read what the grown ups have said.

Did you even remotely consider that 2.5% is not the equivalent of 9%? Of course not. You are busy trying to make a point about trends rather than absolutes.

https://www.statista.com/statistics/1034154/monthly-inflation-rates-developed-emerging-countries/

Note: Japan’s June inflation rate was slightly lower than May’s. So stuff that.

Come on, dude. Quit trying to appear smart with dumb, twisted comparisons.

Wait – you run some Mankiw blog from May to tell us Japan has a low inflation rate but now you cite Asakawa noting how Japan’s inflation rate has gone up. I get you are one confused moron who flip flops 24/7 but DAMN! Of course one could check the data to see Japan has recently seen an increase in the rate of increase in consumer prices:

https://fred.stlouisfed.org/series/JPNCPIALLMINMEI/

Come on Bruce – checking the data is not that hard except for someone who like you gets all of his info from Kelly Anne Alternative Facts Conway.

BTW – we need to do some simple arithmetic since Bruce Hall is incapable of doing so. In a four month period, Japan’s consumer price index has risen by over 1.4%. Annualize this and we have inflation running at 4.3% per year not 2%. Not hyperinflation but to suggest this is a “gradual” rise in prices is stupid even for Bruce Hall.

Let’s make a deal!!!

I’ll take Japan’s 2.4% inflation and invest $100K over 5 years at that rate and give the proceeds to you; you take that same $100K and invest it at 9.1% over 5 years at that rate and give the proceeds to me. Then we’ll call it even.

Already asked, by you or someone else, some weeks ago. And already answered. Japan’s economy has long been highly disinflationary. Mankiw knows that, but leaves it out of his “pondering” pose. Japan having lower inflation than the rest of the world is not a Cvid-era development. It’s dishonest to pretend otherwise.

So, since this was already addressed, why are you asking?

Here it is, deep in comments. Not Brucie:

https://econbrowser.com/archives/2022/05/cross-country-core-cpi-trends

Yea I had to go back and read that alas. We made the point that economies in recession tend to have low inflation rates and what do we get from the mad dog chasing its own tail called CoRev? Just made barking at the moon.

[ Greg Mankiw wonders about our inflation:

May 6, 2022

http://gregmankiw.blogspot.com/2022/05/an-inflation-puzzle.html ]

https://fred.stlouisfed.org/graph/?g=OyIX

January 15, 2018

Consumer Prices and Consumer Prices less food & energy for Japan, 2017-2022

(Percent change)

Japan has been growing minimally since 1992, much of the time caught in a liquidity trap and unwilling to use pronounced fiscal policy to escape. The inflation pattern in Japan however is now echoing ours only more suddued as the economy has been growing so poorly.

Bruce,

Note that Mankiw’s piece is nearly three months old. Why does he think food prices might be rising especially rapidly this fall? A deal has been cut much more recently for grain to get exported out of Ukraine. Now it is true the Russians hit Odesa, but it also seems that the deal is still moving forward, if a bit slowly. We may soon be getting Ukrainian grain out on the world market, which should help slow down that food price inflation problem somewhat, if not end it entirly.

https://fred.stlouisfed.org/series/JPNCPIALLMINMEI/

I guess Bruce was too lazy to check how inflation has been going in Japan of late. It seems to be accelerating.

Bruce Hall – laziest troll ever.

Back at you pgl.

Multiple gauges of the deeper inflation trend hit record highs in June, according to data released by the Bank of Japan on Tuesday. The trimmed mean, a measure of price growth that factors out the biggest gains and falls, rose 1.6% from a year earlier. That’s the fastest rate of increase in data back to 2001, according to the bank.

https://www.bnnbloomberg.ca/japan-s-deeper-inflation-trend-shows-price-growth-spreading-1.1796950

Let’s see… 2.5% vs. 9.1%. Hmmm. Yeah, you’re correct. Inflation in Japan is sooo bad. We’d call that runaway inflation in the US. Looks like the anonymous troll didn’t do a lot of research. “Accelerating”, yeah from nothing to, ooooo, 1.6%.

1.6% not 2.5%….

I shouldn’t overstate Japan’s inflation.

Back at you? Damn – you are a child. But inflation is closer to 4.3%. His 2.5% figure was clearly core inflation. If you want to use that – the core inflation rate for the US is much lower than 9%.

Relax Bruce – we know you are stupid. So no need to remind us of that fact.

Bruce Hall

July 31, 2022 at 11:39 am

1.6% not 2.5%….

I shouldn’t overstate Japan’s inflation.

The 1.6% is over 4 months. So you grossly understated the annualize rate. Damn – you are the dumbest troll ever!

Barkley, there may be two issues at play with regard to food (specifically wheat) prices:

1) supply – an obvious issue given the Russian/Ukraine export situation

2) cost of production/transportation – fertilizer and diesel fuel prices have gone up significantly

https://cl.usembassy.gov/u-s-assistance-to-alleviate-the-rising-global-cost-of-fertilizer/

https://gasprices.aaa.com

Other food prices will also be affected. Some relief on pork an beef (which had previously skyrocketed).

https://www.ers.usda.gov/data-products/food-price-outlook/summary-findings/

In 2022, all food prices are now predicted to increase between 8.5 and 9.5 percent, food-away-from-home prices are predicted to increase between 6.5 and 7.5 percent, and food-at-home prices are predicted to increase between 10.0 and 11.0 percent.

U.S. Government Assistance to Alleviate the Rising Global Cost of Fertilizer

Did you forget to read even the subtitle this time? Or are you advocating government subsidies to bring your food bill down? And we thought you believed any government subsidies was wasteful communism.

Come on Bruce – a little consistency for a change. Damn.

Bruce,

Does this USDA forecast account for some grain possibly getting out of Ukraine soon? I bet it does not.

https://news.cgtn.com/news/2022-07-30/Chinese-mainland-records-100-new-confirmed-COVID-19-cases-1c58C3Dqr7y/index.html

July 30, 2022

Chinese mainland records 100 new confirmed COVID-19 cases

The Chinese mainland recorded 100 confirmed COVID-19 cases on Friday, with 49 attributed to local transmissions and 51 from overseas, data from the National Health Commission showed on Saturday.

A total of 348 asymptomatic cases were also recorded on Friday, and 7,136 asymptomatic patients remain under medical observation.

The cumulative number of confirmed cases on the Chinese mainland is 229,394, with the death toll from COVID-19 standing at 5,226.

Chinese mainland new locally transmitted cases

https://news.cgtn.com/news/2022-07-30/Chinese-mainland-records-100-new-confirmed-COVID-19-cases-1c58C3Dqr7y/img/21ced242eaf247b9b421f2169f3a963a/21ced242eaf247b9b421f2169f3a963a.jpeg

Chinese mainland new imported cases

https://news.cgtn.com/news/2022-07-30/Chinese-mainland-records-100-new-confirmed-COVID-19-cases-1c58C3Dqr7y/img/fa120f75aa6d470f83f23bf88cea090e/fa120f75aa6d470f83f23bf88cea090e.jpeg

Chinese mainland new asymptomatic cases

https://news.cgtn.com/news/2022-07-30/Chinese-mainland-records-100-new-confirmed-COVID-19-cases-1c58C3Dqr7y/img/6e0367ded49b467c83b0baac22e104e5/6e0367ded49b467c83b0baac22e104e5.jpeg

https://www.worldometers.info/coronavirus/

July 29, 2022

Coronavirus

United States

Cases ( 93,054,184)

Deaths ( 1,055,020)

Deaths per million ( 3,174)

China

Cases ( 229,294)

Deaths ( 5,226)

Deaths per million ( 4)

https://fred.stlouisfed.org/graph/?g=lW12

January 4, 2018

Unemployment rate and Employment-population ratio, * 1980-2022

* Employment age 25-54

[ Growth has continued since the year began. There is of course no recession. ]

The only real ‘achievement’ of all this bruhaha about it’s-not-a-recession has been to undermine the credibility of likes of Frankel and Yellen with the public.

[ Thoroughly incorrect and intellectually mean-spirited. ]

Remember – the person who made that thoroughly incorrect statement has ZERO credibility himself.

https://www.thedailybeast.com/matt-gaetz-caught-on-hot-mic-assuring-roger-stone-of-pardon-by-donald-trump

Facing possible jail time after being charged with the obstruction of a congressional investigation, veteran Republican operative Roger Stone was assured by MAGA-loving Rep. Matt Gaetz (R-FL) that former President Donald Trump would offer him a pardon. The new revelation comes from a hot microphone moment recorded by Danish filmmakers back in 2019, which was shared with The Washington Post ahead of their film A Storm Foretold, set to be released later this year. “The boss still has a very favorable view of you,” the fervently pro-Trump congressman told Stone at a right-wing “AMPFest” gathering at one of the former president’s golf clubs, National Doral, before stating that Trump shared that information with him “directly.”

So Gaetz brings Roger Stone this corrupt little goodie. Now did Stone buy Gaetz an underage prostitute in exchange? MAGA!

The Bloomberg consensus for the change in nonfarm employment as of 7/30/2022 is at 250k, although this may be jinxed as my FWIW forecast is at a change of 251k as reported about a month ago.

So far using seventeen job forecast categories has been a great improvement over trying to forecast nonfarm employment by using FRED series, PAYEMS. From what I can tell it looks like many of the separate job categories have forecast models that differ from an overall forecast model.

These are completely off-topic but I saved these for Menzie’s next post because I thought readers may take an interest:

https://www.idahostatesman.com/news/nation-world/national/article263992351.html

https://www.predictit.org/markets/detail/7053/Who-will-win-the-2024-Republican-presidential-nomination

https://fred.stlouisfed.org/series/JPNRGDPEXP

Wait – I just suggested Japan has had weak aggregate demand but FRED tells me that real GDP is far below it was before the pandemic. Why did not Mankiw note this little fact? You will have to ask him if he ever opens that comment box.

Why cannot Bruce Hall get this important point? Easy – Bruce is not that bright!

Real personal consumption has cooled off over the past year mostly due to a drop in durables consumption, but in the first half of 2022, the slowdown has shifted to non-durables. Gasoline is a big part of that:

https://fred.stlouisfed.org/graph/?g=Skfw

We are cutting back on the most inflationary part of household budgets, with the income effect is still enough to slow other purchases.

Despite the big drop in spending on durables, we still haven’t returned to the pre-recession trend. That looks to me like a sizable risk to demand in coming quarters; we already have lots of new durables – no need to keep buying at the pace.

If the income effect remains a drag – which is to say, if energy prices don’t come down – and durables demand retuns to trend, households will likely lead the economy into recession.

A sharp rise in mortgage rates has cut into housing demand. Slower housing sales could generate a further slowing in durables demand. Changing residence often results in increased demand for household durables.

This is a point of curiosity for me. Does the rise in mortgage rates necessarily mean a persistent decline in home sales, even when the glut of unfinished housing inventory gets finished? That would be a bad thing. The U.S. is under-housed. Leaving a bunch of housing inventory unsold and unoccupied would leave a major imbalance in the economy, while at the same time wasting resources.

This is where the Fed comes in. We don’t need more distortion in housing from negative real rates, but we could certainly use low real rates to clear the market, avoid credit market disruption and get people in houses. That’s a tall order. It could work out in the normal run of things, but we have no reason to expect that it will. The Fed’s current mandate and interpretation of that mandate doesn’t involve clearing inventory in the housing market while avoiding inflation in home prices – not directly, anyhow. But it certainly looks like an issue that deserves higher priority in the post-tightening period.

Spin about noise, no?

How real earnings might soon rise from here is not clear to me:

https://fred.stlouisfed.org/graph/?g=QeCl

January 4, 2018

Average Hourly Earnings of All Private and Production & Nonsupervisory Workers, * 2017-2022

* Production and nonsupervisory workers accounting for approximately four-fifths of the total employment on private nonfarm payrolls

(Indexed to 2017)

https://fred.stlouisfed.org/graph/?g=Sii4

January 30, 2018

Nonfarm business productivity and real compensation, 2017-2022

(Indexed to 2017)

The path of real earnings till now doesn’t tell us much about the future path – and please let’s not have another sophomoric discussion of autoregressive processes. What we want to know about is the drivers of real earnings. That brings us to your second graph, comparing labor productivity to labor compensation. Using your end-point, the graph suggests workers have captured all productivity gains in compensation, and so can’t hope to make big gains. Simply by changing the end-point, one gets the impression workers have been given progressively less of their marginal product in compensation, and that different institutional arrangements could result in large gains in compensation:

https://fred.stlouisfed.org/graph/?g=Skqp

Beyond that, much of the loss in real earnings of late has come from inflation, not slack demand for labor. If inflation cools off, there is no reason we could not see a rise in real earnings in a tight labor market. The history of recent business cycles does not suggest wages need to be supressed to contain inflation.

Good point about her 2nd graph. Now if we could get JohnH to get off his soap box and look at the real data.

If inflation abates then Corporate America will likely shift from pricing ahead of inflation back to its earlier strategy of suppressing wage growth, as it did for most of this century. In fact, the current drop in real weekly earnings reflects the real wage suppression that is occurring today, even in a tight labor market.

Josh Bivens talks about this shift between profiting from wage suppression to profiting from price gouging.

https://www.epi.org/blog/corporate-profits-have-contributed-disproportionately-to-inflation-how-should-policymakers-respond/

We have recently seen other instances of very tight labor markets failing to drive real wages up much. In the UK in 2015-16, record low unemployment and record high labor failed to translate into significant real wage gains.

Corporate friendly economists simply fail to acknowledge the power that corporations have over real wages both from price gouging and from wage suppression.

“The rise in profit margins that account for a disproportionate share of price growth in the current recovery have led to speculation that increased corporate power has been a key driver of recent inflation. Corporate power is clearly playing a role, but an increase in corporate power likely has not happened recently enough to make it a root cause of the inflation of 2021–2022.”

What, what? Bivens just undermined your little soap box speech. BTW when you suggest other economists have not been talking about corporate market power you are LYING. Now we do not make fools out of ourselves with your soap box drama but this topic is taken a lot more seriously by real economists than your usual trolling.

“In the UK in 2015-16, record low unemployment and record high labor failed to translate into significant real wage gains.”

Gee – there was some fool over at EconomistView named JohnH who kept telling us real wages in the UK rose a lot even though they had declined a lot. I’m glad you corrected that lying troll.

China Johnny? Calm down. We know how emotional you get. ‘Scuse, me – how emotional you are. You’ve simply got this issue wrong. Again. As always.

“Economists” don’t disagree with Bivens. Buvens is, in fact, and economist:

Ph.D., Economics, New School for Social Research

B.A., Economics, University of Maryland at College Park

Former university economics professor

By the way, the chief economist for President Obama, whom you seem to blame for everything, has written pretty extensively about concentration of market power, and did so while working for Obama. Biden’s administration is the most aggressive in anti-trust action of any administration in a generation. If you don’t know that, then you don’t know enough to have an opinion.

I don’t think you actually care, though. It doesn’t matter who thinks what or who does what. You want attention, so you throw tantrums. I am coming around to the view that you want attention because that’s what your ideological masters ask of you, like with ltr. Same task, same masters. But whatever your reason for these text-tantrums, you’re simply wrong most of the time.

JohnH,

In the meantime, you can explain to your child how it is worse for the US to criticize Putin’s invasion of Ukraine than it is for Putin to invade Ukraine.

https://fred.stlouisfed.org/graph/?g=MN2G

January 15, 2018

Consumer Price Index for Food and Energy, 2017-2022

(Percent change)

https://fred.stlouisfed.org/graph/?g=Fn2j

January 15, 2018

Consumer Price Index for Rent and Owners’ Equivalent Rent, 2017-2022

(Percent change)

Professor Chinn???

Is Edward Leamer still giving lectures and active at UCLA?? I ask because i LOVED Professor Leamer’s “dry humor” (which reminded me of my father’s dry humor) And I miss his lectures, Do you know if Professor Edward Leamer is OK?? I miss his “dry” humor very very much. THANK YOU

Moses,

Are you sure you were in the right class? Archeology 112 “Disco Songs of the 1970s and Their Miscontents” is down the hall.

https://www.msn.com/en-us/money/markets/us-recession-would-likely-impact-white-collar-workers-economist-says/ar-AA102KTr?fromMaestro=true

William Lee, chief economist at California think tank the Milken Institute, told MarketWatch that many low-skill white-collar workers risk being replaced by apps or other technology. He added that manual workers had less to fear, in contrast to previous recessions, if they have “jobs that are in high demand” such as an Amazon warehouse worker or a delivery driver.

OK – I have never heard of William Lee and I’m not one to trust anyone from the Milken Institute. Anyone else want to weigh in on this thesis? Like the idea that white collar workers are low skilled strikes me as novel.

In spite of the images and facades they carefully culture, Colleges are hard core predatory capitalist businesses. If you want to know why poor people with better grades are offered less scholarship money, read this:

https://slate.com/business/2022/07/college-financial-aid-sham.html

“As DiFeliciantonio wrote: “Wealthy families are more able and less willing to pay for college while the poorer families are more willing and less able.” In other words, parents of means who themselves have finished college are often sophisticated consumers of higher education and are able to drive a hard bargain, whereas lower-income, less-educated parents feel an enormous obligation to help their children move farther up the socioeconomic ladder and blindly trust that colleges have their best financial interests at heart.”

The educational and financial information you give on your college application is NOT being used to decide how worthy you are of admission and scholarships – it is being used to personalize how best to exploit you. The poor and unsophisticated are more likely to fall for “used car salesmanship” tricks and take on student loans way beyond what they can afford, because “this is a once in a lifetime” ticket to the higher-up classes for that child. The more sophisticated must be stroked with “achievement” scholarships (regardless of grades) to confirm that they are indeed considered “upper”. This system, off-course, being underwritten by your tax dollars – and your donations to that wonderful University that keeps calling, mailing, begging you for more money.

Economic mobility is not in the interest of those on top. Those on top control budgets in higher (and lower) education. Legacy seats at law schools, medical schools and elite universities exist as a way of creating a permanent upper class. Same with the effort to eliminate inheritance taxes.

When ranked by the Gini coefficient, the U.S. is 46th out of 162 countries in terms of income distribution. In the bottom third, missing falling into the bottom quarter by a very few steps.

If China Johnny actually cared about this issue, he’d stop howling nonsensical stuff and think about practical remedies. Better access to higher (and lower) education is a practical remedy.

Gini indices:

https://www.indexmundi.com/facts/indicators/SI.POV.GINI/rankings

Did Bill Cassidy hire Princeton Steve as his economic advisor?

https://abcnews.go.com/Politics/democrats-health-climate-deal-disinflationary-causing-recession-sen/story?id=87678074

As Senate Democrats push a major economic, health and environmental package, “much of what they’re saying about this bill is just not true,” Sen. Bill Cassidy, R-La., contended on Sunday. “It may be disinflationary by causing a recession,” Cassidy told ABC “This Week” co-anchor Jonathan Karl. “They’re interjecting an incredible amount of uncertainty into the economy.”

Oh no – it is INFLATIONARY! Wait is going to cause a RECESSION!

Maybe we should call this bill Shimmer. It is a floor wax. No – it is a desert topping!

Oh wait Republican Senator Pat Toomey does not like this bill calling it INFLATIONARY. Can these hacks please make up their damn minds?

https://www.msn.com/en-us/sports/nba/bill-russell-legendary-celtics-center-and-nba-coach-dead-at-88/ar-AA109XqI?OCID=ansmsn

The late great Bill Russell was the best defensive player ever. An NBA legend is now playing hoops in Heaven.

The Georgia Senate race involves a competent incumbant who is also a minister v. an ex football player who apparently has beaten girlfriends and deny the existence of his own kids. Trump of course supports the latter but it seems Georgia voters are not that incredibly stupid.

https://www.businessinsider.com/warnock-leads-walker-georgia-senate-kemp-abrams-governor-poll-2022-7

For better or worse, I have seen a report that Pelosi has decided not to visit Taiwan at this time. I think that is a wise move. It looked it would not add support for Taiwan, only please a local constituency of hers, while threatening to really mess things up over there. Actually, I think the greatest danger was not China invading Taiwan, but deciding not to adhere to sanctions on Russia that they have been and start supplying certain crucial inputs that would help Russia’s military machine. Of course, that would have pleased the likes of JohnH.

BTW, to pgl. Steven is not the worst troll here. That is a contest between CoRev and JohnH.

This whole Pelosi visit to Taiwan is just another fiasco, another case of the US shooting itself in the foot. On the one hand, Pelosi’s visit threatens to provoke China into a war, even though numerous DOD war games over the years have shown that the US would lose. https://www.realclearinvestigations.com/articles/2020/08/17/the_scary_war_game_over_taiwan_that_the_us_loses_again_and_again_124836.html#!

If US intelligence on China’s capabilities is as flawed as its underestimation of Russia’s, the defeat could potentially have been severe…yet another pointless and futile war…shooting yourself in the foot.

On the other hand, Pelosi’s strutting and preening creates the perception that the US is back, king of the mountain, and that China is helpless to do anything but bow to American superiority. If she now decides to back down, it will be an embarrassment…a sign of weakness, Blinken her eyes, and dropping her gaze before a powerful rival. So much for the perception of US global hegemony.

Sad that there are no adults running US foreign policy…

JohnH: Wow.

Amazingly enough, Tom Friedman agrees with my position that Pelosi’s Visit to Taiwan Is Utterly Reckless:

“Nothing good will come of it. Taiwan will not be more secure or more prosperous as a result of this purely symbolic visit, and a lot of bad things could happen. These include a Chinese military response that could result in the U.S. being plunged into indirect conflicts with a nuclear-armed Russia and a nuclear-armed China at the same time.” IOW the US could be shooting itself in the foot…

https://www.nytimes.com/2022/08/01/opinion/nancy-pelosi-taiwan-china.html

I expect the blowback, even if not military, will not be pretty.

You talking about adults? Macroduck is right – just another emotional temper tantrum.

Pelosi would not be the 1st Speaker of the House to visit Taiwan. Newt visited back in 1997. Now I do not recall Johnny boy screaming about that visit.

Then again a lot of Republicans are urging Pelosi to make this stop while the Biden White House is arguing she should skip it.

Moses,

Who is Don?

We can see a clear divergence in the data from Q3 of 2020 or 2021. That’s when GDP diverges from final sales (Fig 1) and GDO diverges from GDP (Fig 2). It is hard not to imagine this has to do with the various and massive stimulus packages. When these packages roll off — to appearances in Q1 and Q2 2022 — we might expect to top line — GDP in Fig 1 or GDO in Fig 2 — to converge back down to the lower proximate line. This is contractionary fiscal policy on a substantial scale, the sort Menzie has written about many times before. I don’t know why this would be a surprise, and it does represent in that sense a ‘technical recession’, as it originates not in the business cycle, but rather from a non-recurring blast of fiscal stimulus. This line of thinking doesn’t seem all that exotic to me.

The question then is what happens in Q3. One possibility is that the run-off of the stimulus ends and the economy returns to growth. Possible, and consistent with both Atlanta Fed and IHS Markit’s current forecast. Or perhaps there remains some residual run off. Or finally, the economy may be entering an ordinary business cycle recession associated with interest rates increases necessary to quell inflation. I would put my money on the latter, but I am not at this point convinced such a recession starts in Q3. Q4 2022 or Q1 2023 may be more likely. It’s too early to tell, at least from my perspective.

I think it is quite important to distinguish the stimulus run-off from interest rate hikes. These are, I think, separate dynamics and need to be treated as two different episodes rather than one single recessionary event.