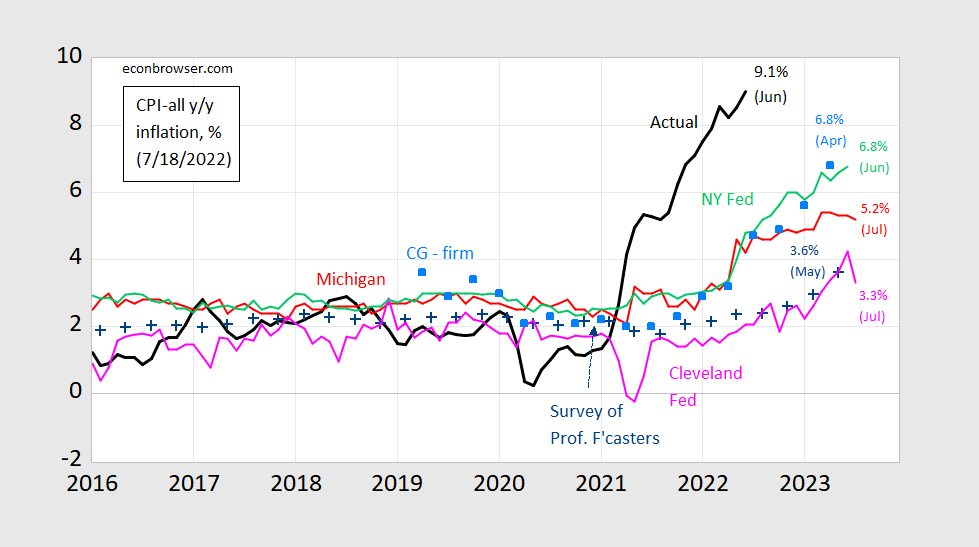

NY Fed consumer expectations up in June, Michigan down in July. WSJ July survey mean says y/y inflation will be 3.9% in June 2023.

Figure 1: CPI inflation year-on-year (black), median expected from Survey of Professional Forecasters (blue +), median expected (preliminary) from Michigan Survey of Consumers (red), median from NY Fed Survey of Consumer Expectations (light green), forecast from Cleveland Fed (pink), mean from Coibion-Gorodnichenko firm expectations survey [light blue squares]. Michigan July observation is preliminary. Source: BLS, University of Michigan via FRED and Investing.com, Reuters, Philadelphia Fed Survey of Professional Forecasters, NY Fed, Cleveland Fed and Coibion and Gorodnichenko.

While the NY Fed one year inflation expectations ticked up in July, from 6.6% to 6.8%, the median three year expectations fell from 4.76% to 4.60% (and is down from 4.88% in March).

I keep hearing people express negative GDP for 2nd quarter. I don’t see it. What in the heck do they think is going to hit the numbers so badly?? I will admit the Fed hikes aren’t helping and in my opinion are dumb, but even if we take the Fed hikes as a given negative, it takes time for those negative ripples to feed through. You sure as hell aren’t seeing it in recent equities markets, and I think that would be there if we were going to have negative 2nd Quarter GDP. I’m not willing to put an exact number out there, that being said, I think anything predicting below +0.1% GDP borders on the asinine.

Moses,

I may be one of the misguided, but it also may be that the only positive influence on real GDP for 2022Q2 could be real personal consumption expenditures. FRED monthly series PCEC96 for April was 13,950.3 bn and May 13,895.5. Using RRSFS to forecast June PCEC96 I get 13,806.4. Averaging the three data points to find the quarterly average amount, I get 13,903.1. 2022Q1 FRED quarterly series PCECC96 was 13,881.1. Comparing the 2022Q1 reported amount to the 2022Q2 forecast shows a Q/Q % change of about 0.16% or about 0.6 compound annualized. Multiply 0.6 by 68% the approximate share of GDP represented by personal consumption expenditures equals about 0.4% annualized contribution to real GDP. The negative forecast seems to be caused by forecasts of negative impact of personal investment, exports, imports and government expenditures.

See section one of BEA: Table 1.1.10. Percentage Shares of Gross Domestic Product

https://apps.bea.gov/iTable/iTable.cfm?reqid=19&step=2#reqid=19&step=2&isuri=1&1921=survey

https://fred.stlouisfed.org/series/PCECC96

AS,

Inventory changs are likely to be positive for Q@, a mqjor change from Q1, a point I have made repeatedly here, although might not be enough to pull total GDP up. It was a major factor in pushing it negative in Q1.

The Princeton Steve and Bruce Hall types are saying this for partisan reasons of course. And their “logic” is their usual babble. Your counteranalysis makes a lot more sense to me.

pgi,

Thanks for the comment. I try to present an objective analysis. I may be wrong in my analysis, but not due to political reasons.

Inventories.

https://fred.stlouisfed.org/graph/?g=RVxD

In order for inventories to add to the change in GDP in a quarter, they have to rise more than in the prior quarter. You see how large the inventory gain was in Q1? Second biggest gain on record, but it counted as a drag on GDP because it followed the biggest gain on record. In order for inventories to add to GDP growth, we have to have a bigger than than in Q1. That would require the three biggest gains in history, all in a row. Doesn’t seem likely, despite the headlines about unwanted inventories. Unwanted inventories are a problem for Q3, right enough, but being unwanted doesn’t make them big enough to add to GDP growth.

Mostly, though, we don’t have the data to know. We’ve got some May data, unrevised.

Better new on the trade balance, but again, too little data to be certain. The rest of the world is sucking sooner than us, which is bad for net exports.

https://fred.stlouisfed.org/graph/?g=RVyS

I agree with everything you said, but doesn’t the Atlanta Beige Book imply some more recent data, that although slowing, still leans positive??

I found this outfit in a WSJ article about two months back, and thought bookmarking the page might be useful. It seems if WSJ is willing to quote them they would be at least semi-reliable:

https://www.earnestresearch.com/data-bites/june-2022-earnest-research-spend-index/

https://www.earnestresearch.com/data-bites/off-price-department-stores-won-the-pandemic-but-are-losing-2022/

MD,

I don’t know about Fred data, but I looked at BEA and inventories changes were negative in Q!. They followed imports as being one of the main reasons GDP went negative so unexpectedly in Q1. There certainly have been lots of reports about a massive buildup of “unwanted” inventories in the US economy. They may be unwanted, but a buildup of them pushes that GDP number up.

We shall see. Data on them seems to be spotty and mixed.

when the fed was trying to instigate inflation a while back, I think they would not have had a problem with it in the range between 4% and 6%. while we are over that target right now, it is not unreasonable to see us in that range before the end of the year. the problem will be if the chorus begins to push sub 2% inflation going forward. that target will push us into recession.

as an aside, our house now has $60k sitting in savings bonds earning 9%, risk free. there were some on this blog criticizing savings bonds a year ago. you may not retire on savings bonds, but you sure can offset your inflation costs to a reasonable degree.

Let’s say we ended up with 4% inflation. Summers used to advocate a 5% target inflation back in the day but now his hair is on fire than we may not see 2% inflation for the near future.

Real estate bubble bursting and bank runs in China.

https://www.cnn.com/2022/07/18/economy/china-stem-anger-mortgage-boycott-bank-protests-intl-hnk/index.html

The official propaganda machine may have to work overtime to deal with this

Yeah, and because China insists that bad news is good, and because closing he productivity gap has made economic management look clever, we aren’t going to get the straight story from China or from Western analysts who insist China “has the necessary tools”* to avoid credit problems. Shade your expectations for China downward. Shade your global outlook lower in conjunction.

And keep your eye on China’s dealings ith Russia. India’s, too. Let’s see how things go when domestic concerns get in the way of solidarity.

* Don’t know how “necessary tools” became magic words, but I’ve send them all off the place whenever China’s credit troubles are discussed.

I don’t know what this changes in terms of foreign funding of Russia’s War on Eastern Europe. Seemingly nothing. Still, it’s an interesting data point:

https://www.yahoo.com/finance/news/russias-crude-deliveries-china-india-172227578.html

Cool find. Filling stockpiles at a discount can only last so long.

But remember, you are a western economist who cannot understand the magic of Russia. Western math doesn’t apply. Russia is gonna do great, ’cause… Oh, look! Balloons!

Armchair wanna-be Economist. As you and Menzie know too well. Like Archie Bunker watching Jim Plunkett of the Raiders on Monday Night Football. I know all the passes that Jim missed that I could have gotten.

But I can “BS” my way as long as Menzie doesn’t ask me to produce my model results in “R” or “show my work” on the final exam.

: )

A story just came out the Saudis are exporting more oil to China. Better them than Russia.