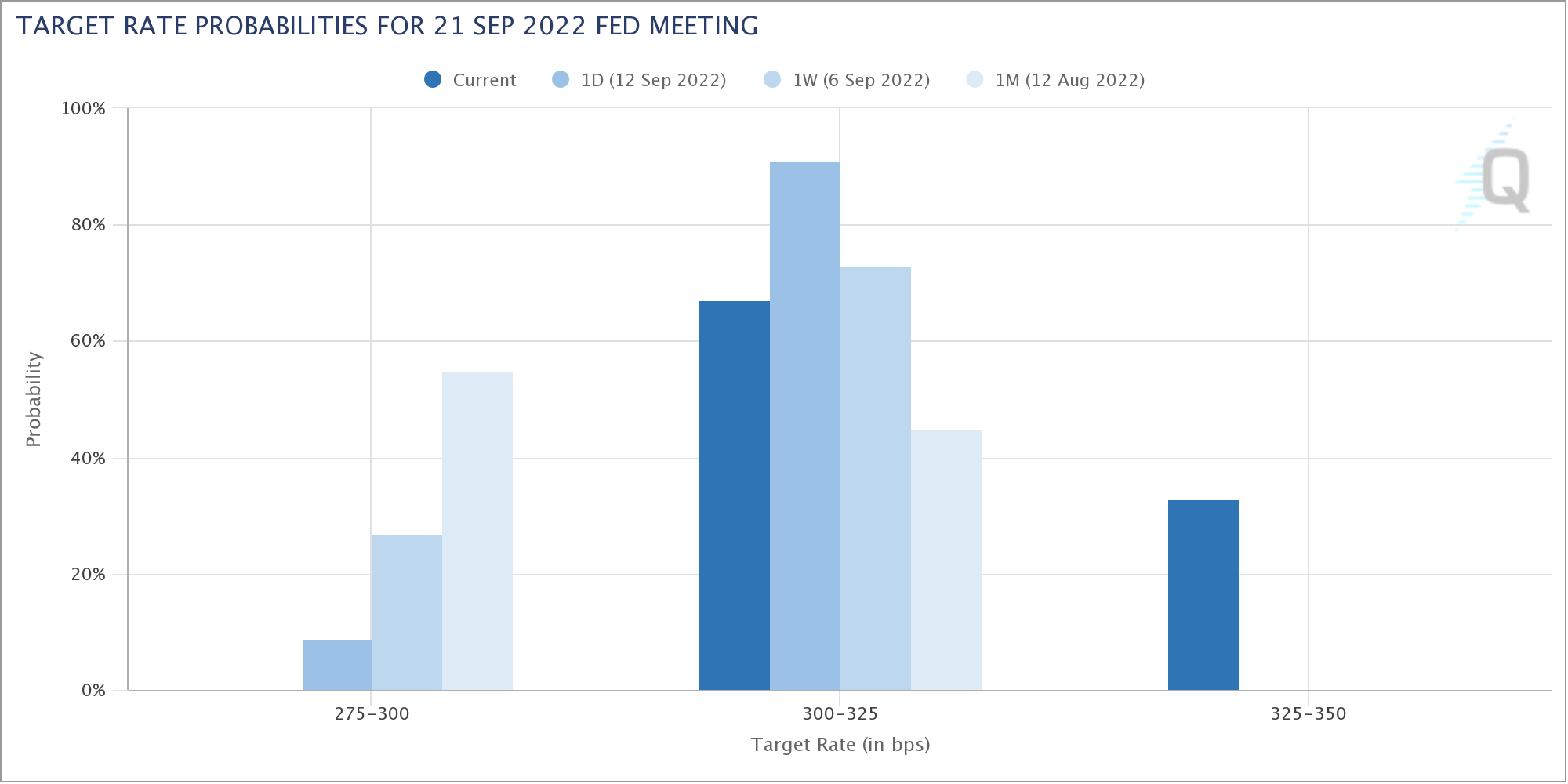

From CME FedWatch app, in the wake of the CPI surprise.

So the expected Fed Funds rate (assuming risk neutrality) is:

Source: Federal Reserve via FRED, CME FedWatch (accessed 9/13), and author’s calculations.

From CME FedWatch app, in the wake of the CPI surprise.

So the expected Fed Funds rate (assuming risk neutrality) is:

Source: Federal Reserve via FRED, CME FedWatch (accessed 9/13), and author’s calculations.

It’s too much. But you can’t tell a bureaucrat trying to protect his own job any different. Even if thousands/millions of others suffer in the process. Jerome gonna take care of Jerome.

The highest-odds estimate is still a 75 basis point hike. The least disruptive policy decision for the FOMC is thus a 75 bp hike. The FOMC can gain little from an extra 25 bps in the short term, and can anticipate more market volatility like today’s if they go ahead with 100 bps.

The pricing in of a chance of a 100 bp hike need remain in the market at most a week. It may be of little comfort to those who went into today’s CPI release long equities, but that’s not much time to affect the real economy.

Equities will short squeeze that back up. Equities have far little impact on real economic activity.

@ Macroduck

“The FOMC can gain little from an extra 25 bps in the short term,”

So what about the long-term, into 2023?? And if only moving it 25 bps Sept 21 means a healthier/sturdier 2023, do we move rates 75 bps to please “market makers” and cats like Summers?? We want the two kids to stop screaming and crying in the kitchen, we agree to let them have 5 Oreo cookies each late afternoon because turning them into fatties in mid-2023 is worth getting them to stop having tantrums every other late afternoon??

I mean I think you have sensed how I feel about this for weeks now, and I’m not arguing with you here, but earnestly asking your opinion, does a 75 bps move that makes 2023 an economic nightmare worth 3 months of going “Yeah, we did what we needed to do to stop inflation” that wasn’t going to be enduring/perpetual either way?? I just think this 75 bps move has asinine written ALL OVER it when we look in the rear view mirror from July 2023.

We’ve seen effects of future rate hikes pulled forward – this is “the most anticipated tightening cycle ever” as they say. That mean this time is different. There have been two big supply shock in quick succession, one of which was mostly not energy-focused. That also makes this time different. Europe is suffering a far more severe supply shock than we have. China has turned the first supply shock into a series of rolling shocks, with a widening financial shock to go with it. That’s new, too.

All of which is to say, 25 basis points of additional demand supression – next week, next month, next quarter – isn’t likely to matter much. Fed policy makers are operating mostly in the dark this time. They are also working with tools inappropriate to the task. They have no good choices, no clear path.

One thing they still have is control overtheir tools and control over their tools allows them to be predictable. The appearance of a clear plan and determination to carry it through is mostly a show of being predictable.

The one thing in this performance of central bank steadiness that I really wish theu’d stop doing is yammering about the labor market. We don’t need wage suppression. We need rebalancing.

If I were the king of the world, tell you what I’d do. I’d raise rates gradually in order to increase the cost of fundinf for financial activity. Let wages rise, but get stock valuations back in line with historic norms. Deleverage the economy to reduce risk.

But what do I know? I’m just another peasant.

If you’re a “peasant” then you’re a wise peasant, I’ll take that over these oblivious sovereigns any day of the week. I was trying to think of a fictional character here to compare you to, to give a better gist of my meaning. Obi Wan Kenobi??

https://en.wikipedia.org/wiki/Wise_old_man#/media/File:Rembrandt_Harmensz._van_Rijn_038.jpg

https://images.app.goo.gl/6GgYRjfyDXNcSAUs5

Lol, ex rent core cpi fell and overall cpi ex-rent was quite negative…….

Make that the change in cpi. Else Ricky Stryker pooh will go all legal on us with fancy calculus!

There’s something worth knowing.

Gold standard types argue (usually without knowing it) for whipping all other prices around as needed to stabilize the price of gold. Focusing on bringing CPI inflation down to 2% when it’s driven mostly by implicit rents of private homes is sort of like substituting housing for gold. To heck with other economic factors, as long as we stabilize one measure of housing costs.

Foretunately, the PCE deflator has a lower weight for housing.

The equity indices are still technically in an uptrend from the June’s lowest point.

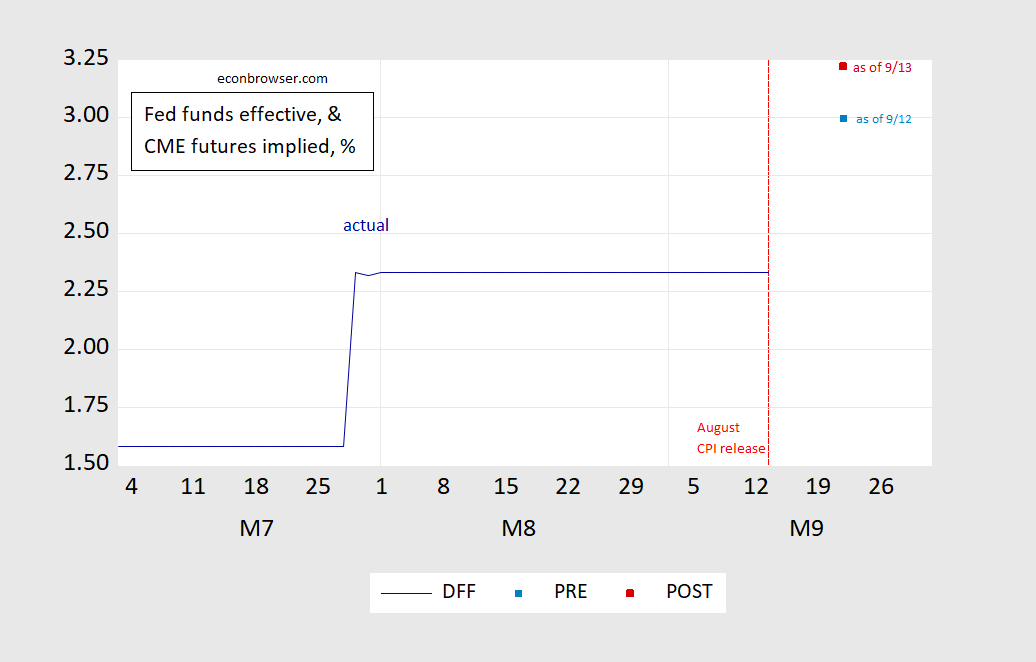

There isn’t much surprise to the CPI print, other than inflation still being here, and that rates will go up.

That’s not new information.

Rates going a bit higher? by how much? 200 basis points? to “neutrality”

It’s laughable.

The goal of going back to 2% will never happen.

Neutrality is the goal.

Love to have a new kid in the conversation, but need more clarity regarding this:

“The goal of going back to 2% will never happen.

“Neutrality is the goal.”

Which 2%? Inflation? Whose goal? Yours? How do you know?

I’m slow. I need a few more words.

@ Macroduck She made at least one intelligent comment prior. No one here will believe this but I was hoping so bad we’d have a regular female commenter on this damned blog.

Trying hard to reserve judgement. We don’t have any Emi Nakamura’s sitting silently in the audience?!?!?!?!? Come on…… show up and show half-decent intelligence. I promise I’ll keep all 15 bad multiple personalities of my 20 total concealed in my orange VW van toy whenever you’re on here. Tomorrow if some female commenter shows up here with even a faint pulse on her wrist, I promise to take some valium pills with my beer, so as not to even care to disagree. Just like, pretend you don’t need a “safe space” to protect you from your own shadow and we’ll all play along, and you’ll get the take home game version from Menzie at the end.

See, even pgl at one time thought I was pure evil and we locked bullhorns more than once, and ever since I haven’t revealed his real ID since figuring it out, even pgl will swear I am probably almost 1/8th human now. We will be nice, show up economist females.

Isn’t “noise” the most likely explanation?

Kevin Drum has several excellent posts of late including this:

https://jabberwocking.com/heres-how-best-to-look-at-inflation/

Here’s how best to look at inflation

prices have been flat for the past two months.

HEY – that is what I said!!!!

Lets also note hedgies who brought properties are not selling. They are fixing and renting. Sellers are striking. This means far lower transactions and from a inflation, much more rental properties……..deflation is coming.

https://www.msn.com/en-us/money/markets/wholesale-prices-fell-01-25-in-august-amid-inflation-fears/ar-AA11P7m8

PPI actually fell in August. Now CPI did rise but by a mere 0.12% (M/M). All this press over how inflation remains high strikes me as reporters who flunked 1st grade arithmetic.

One swallow does not a spring make. Mathematically, you are correct. Inflation is very low in July and August, 0 and 0.1 respectively for CPI. But I don’t think it is reasonable or even theoretically sound to base your projections on one month. You are in essence saying that inflation will be 0.12% for the next year. Why not say it was 8.5% over the past year? It boils down to knowing where prices are heading, right? You are saying you know that prices will be stable for the next twelve months so leave rates alone.

Inflation has been running very high for very long, though, with interest rates at levels which would make even Greenspan blush. Most indicators show that stocks and housing are in bubbles. There are always arguments about Shadow Stats, hedonics and substitution as well. Or stripping out volatile elements that are out of Fed control (as if the Fed is supposed to control specific elements of the CPI but not others). Then there is continuing and very high global inflation. The notion that America is magically immune when the rest of world is running at 8% and higher is laughable. Perhaps it’s all supply chain problems which will just take time to be solved? so let’s leave rates low to make sure that house prices and stock prices keep rising, right?

It’s been a while since I got may econ masters so the mechanics and reporting are not really at my finger tips any more. Constructive criticism welcome.