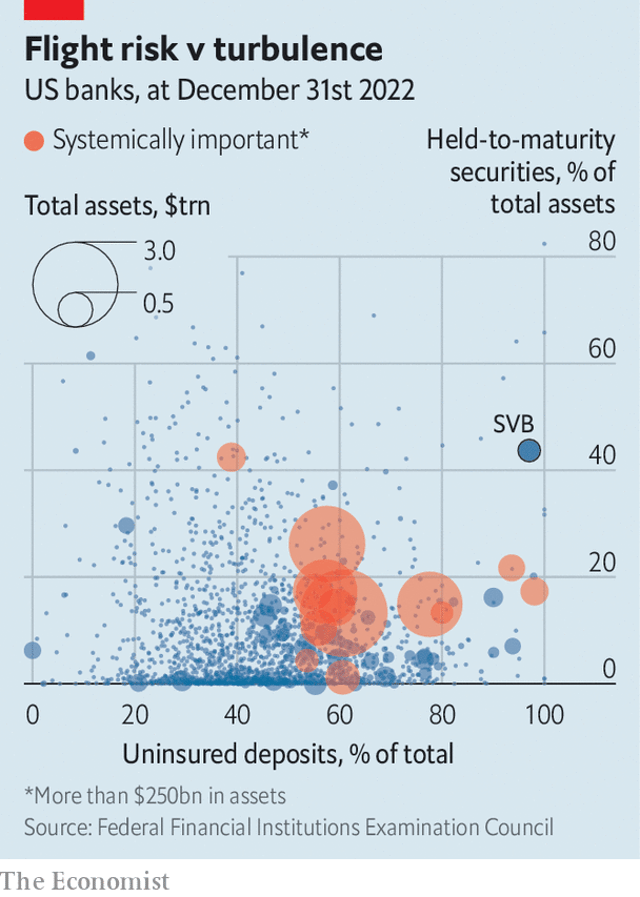

Pretty unique, in terms of size, and the combination of uninsured deposits and held-to-maturity securities. From the Economist:

Pretty unique, in terms of size, and the combination of uninsured deposits and held-to-maturity securities. From the Economist:

Says the New York Times:

“The bank was using an incorrect model as it assessed its own risks amid rising interest rates, and spent much of 2022 under a supervisory review.”

Really? Under supervisory review for much of 2022 and no flags raised about risk management, about having no Risk Officer, about duration mismatch, about monolithic depositor base?

Um, who was doing the “supervisory review”?

“Really? Under supervisory review for much of 2022 and no flags raised about risk management, about having no Risk Officer, about duration mismatch, about monolithic depositor base?”

those red flags are probably what put it under review to begin with. that does not mean the bank will take meaningful action. but it indicates regulators knew there were problems.

The other factor that’s not shown on the chart is the mix of those HTM assets. SVB made the mistake of going with long dated securities as opposed to laddering short-dated ones. Those long dated bonds were much more sensitive to the Fed’s interest rate hikes which put them into a loss position much quicker than they otherwise would have been.

I’d love to see a stat on how other banks are positioned in their HTM portfolios. Especially those orange (pink?) circles.

that is a problem from a fast increase in interest rates. some banks may have handled it better than others.

those systemically important banks probably handled it better than the local and regional banks.

Lest We Forget

The $147 billion financial institutions borrowed from the Fed in the week to the Ides of March is a clear signal that Something is Wrong. It isn’t a record (as the New York Times seems to think), not by a long shot, but it should be a clear reminder of the need for proper financial oversight.

For 20 scary weeks, from September 2008 through February 2009, borrowings averaged $268.7 billion a week, including an actual record $437.53 billion in mid-October. From then until last month, the average was less than $9 billion a week.

https://fred.stlouisfed.org/series/TOTBORR

$300billion was added to fed balance sheet per week of 16 mar report.

qe over?..

Nope, it will reverse out quickly.

let us know when?

https://www.federalreserve.gov/monetarypolicy/bst_recenttrends.htm

$300b is roughly 50% of the recent qt.

Not really. Your talking 300 billion in assets, not dollars. Assets don’t last on balance sheets in this case.

There is no doubt that SVB was a particularly poorly run bank – with no risk manager. But it is also clear as noted by “w” that the oversight was very poor. It seems that the Fed is not up to that job. Maybe we need to let the FDIC do the oversight and also charge fees according to the risk that a bank is taking. We can all look at this and see the problem. But how early was this visible and why didn’t someone step in a block the bank from doing operating at this level of incompetence.

“But how early was this visible and why didn’t someone step in a block the bank from doing operating at this level of incompetence.”

i don’t disagree with your comment. but at what point do you pull the trigger? that is the big problem. it is easy, in hindsight, to say this should have been done. but you are asking regulators to pull the trigger before a disaster strikes. much tougher to do in real time for prevention.