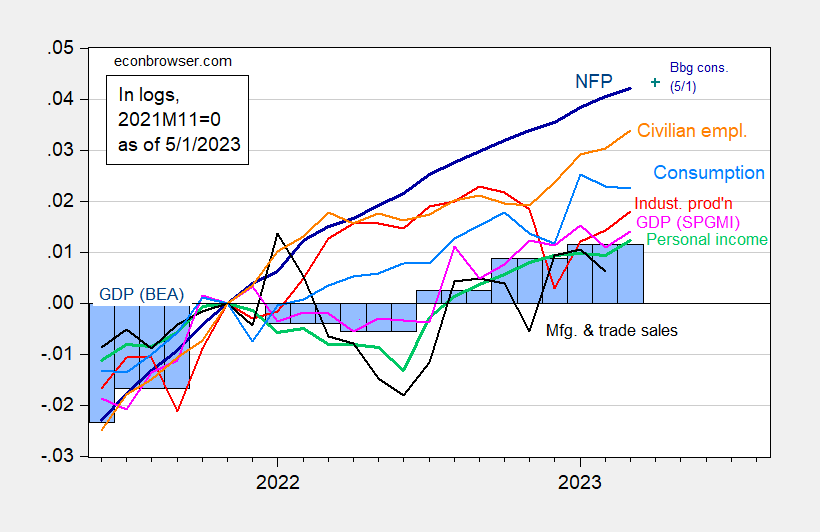

Monthly GDP from S&P Global Market Insights is up 0.3% in March (3.9% annualized), final sales up 6.3% (annualized). This follows on the heels of Thursday’s announcement that nominal personal income and nominal personal spending exceeded consensus by 0.1 ppts m/m. Here is a picture of the key series followed by NBER’s Business Cycle Dating Committee, augmented by monthly GDP (where the top two are real personal income excluding current transfers and nonfarm payroll employment).

Figure 1: Nonfarm payroll employment, NFP (dark blue), Bloomberg consensus of 5/1 (blue +), civilian employment (orange), industrial production (red), personal income excluding transfers in Ch.2012$ (green), manufacturing and trade sales in Ch.2012$ (black), consumption in Ch.2012$ (light blue), and monthly GDP in Ch.2012$ (pink), GDP (blue bars), all log normalized to 2021M11=0. Q3 Source: BLS, Federal Reserve, BEA 2023Q1 advance release via FRED, S&P Global/IHS Markit (nee Macroeconomic Advisers, IHS Markit) (5/1/2023 release), and author’s calculations.

Most series exhibit continued upward trends, asided from consumption. Employment growth as measured continue to lead the upward movement.

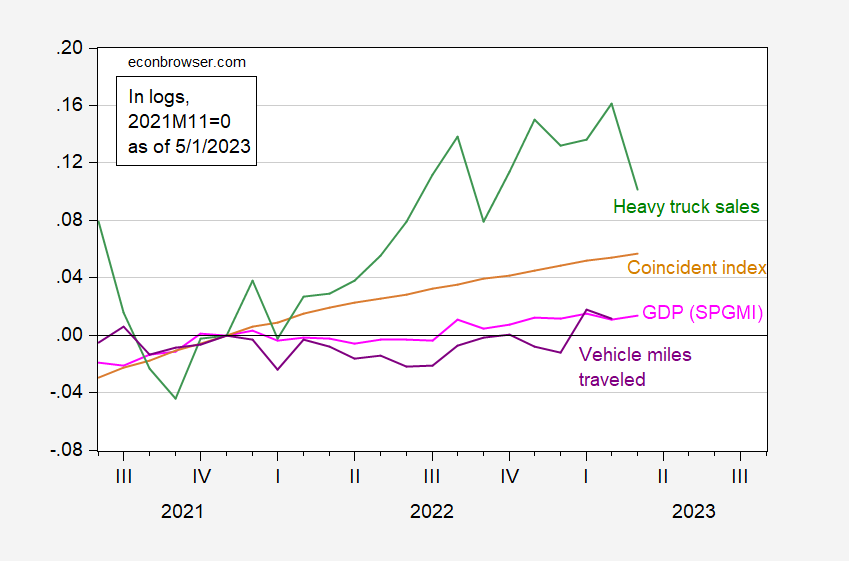

Some alternative measures have been suggested. In Figure 2, I show the Philadelphia Fed’s coincident index for the US, heavy truck sales and vehicle miles traveled, compared against monthly GDP.

Figure 2: Monthly GDP in Ch.2012$ (pink), coincident index (tan), heavy truck sales (green), and vehicle miles traveled (purple), all in logs, 2021M11=0. Source: S&P Global/IHS Markit (nee Macroeconomic Advisers, IHS Markit) (5/1/2023 release), Philadelphia Fed, Commerce, and NHTSA via FRED, and author’s calculations.

The coincident index, which largely reflects labor market measures, continues to rise faster than monthly GDP. Heavy truck sales, a particularly informative measure of business cycle movements, has outpaced the coincident index, but has dropped substantially in March. In contrast, vehicle miles traveled (a lousy coincident measure of recessions) continued to rise through February.

The foregoing suggests, in line with the advance estimate of GDP, that a recession has not yet arrived. (For more on GDP+ and final sales, see this post.)

https://www.nytimes.com/2023/04/30/business/media/hollywood-writers-strike.html

https://jacobin.com/2023/05/haymarket-affair-martyrs-memorial-history-chicago-may-day

https://jacobin.com/2023/04/labor-market-manipulation-big-tech-unemployment

The working class can only win through unification. And the power brokers always now that. Which is why they use the media~~especially television and radio, to divide people, over things which are less important than earning your daily bread, and not having your humanity trampled on.

In news about the wage recession, real-time inequality reports the distribution of real factor income as follows:

Bottom 5% -2.3%

Middle 40% -1.1%

Top 10% +5.8%

https://www.realtimeinequality.org/

For the vast majority, it’s Scant consolation to learn that the economic recession has not arrived…

…… and then she said “It’s because your VMT isn’t big enough” [ canned studio laughter here ]

I could have been the greatest writer on the “Friends” TV show writing staff you know. If I didn’t shoot myself after reading the scripts.