Here is a picture of recession probabilities from probit regressions on 10yr-3mo and 10yr-2yr term spreads, in light of Cam Harvey’s updated views.

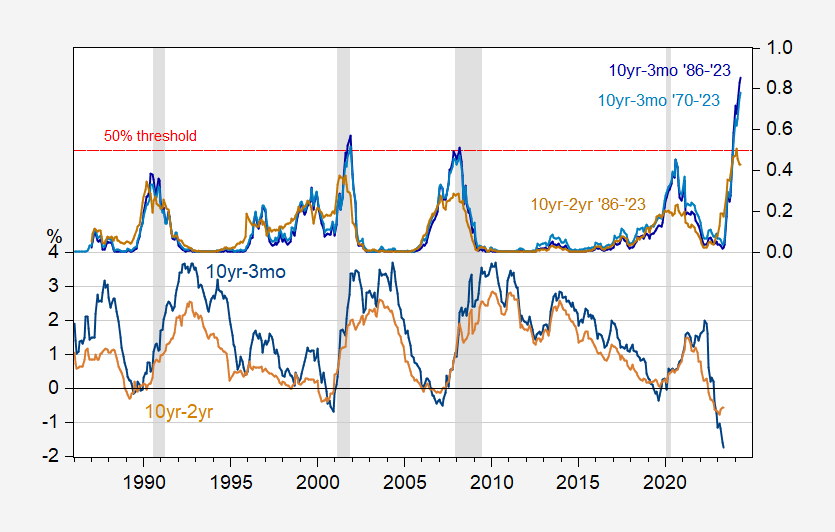

Figure 1: 10yr-3mo Treasury spread (blue, left scale), and 10yr-2yr spread (tan, left scale), both in %; and probability of recession from 10yr-3mo over 1986-2023M05 period (dark blue, right scale), 1970-2023M05 (light blue, right scale), and 10yr-2yr over 1986-2023M05 period (brown, right scale). NBER defined peak-to-trough recession dates shaded gray. Regressions assume no recession occurred as of May 2023. Source: Treasury via FRED, NBER, and author’s calculations.

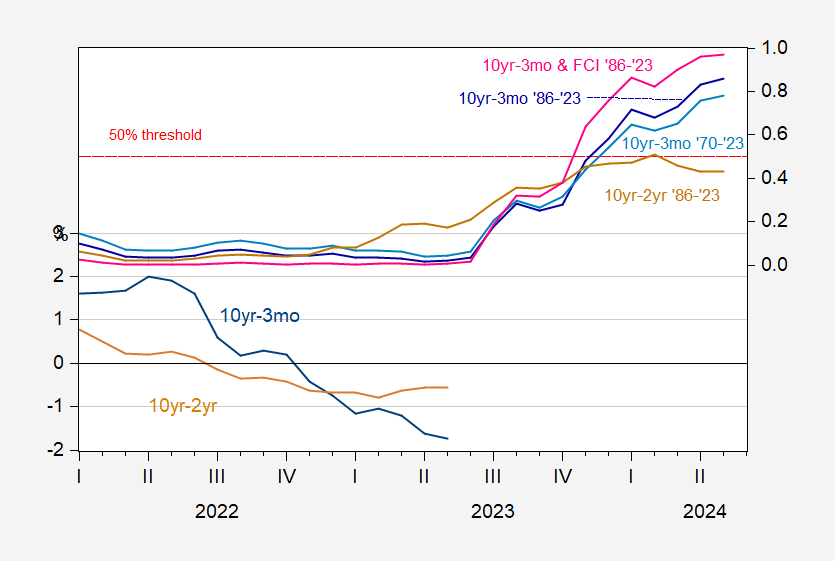

Note that omitting the 2020 pandemic related recession and subsequent time period does not change the basic results; then the probability (using 1986+ sample) rises from 0.86 to 0.89 for May 2024. The results are also insensitive to inclusion of time trend. The estimated probability does rise noticeably if the Chicago Fed’s national Financial Conditions Index is included. Figure 2 shows a detail of the above forecasts along with the FCI augmented series.

Figure 2: 10yr-3mo Treasury spread (blue, left scale), and 10yr-2yr spread (tan, left scale), both in %; and probability of recession from 10yr-3mo over 1986-2023M05 period (dark blue, right scale), augmented by Financial Conditions Index (pink, right scale), 10yr-3mo term spread over1970-2023M05 (light blue, right scale), and 10yr-2yr over 1986-2023M05 period (brown, right scale). NBER defined peak-to-trough recession dates shaded gray. Regressions assume no recession occurred as of May 2023. Source: Treasury via FRED, Chicago Fed via FRED, NBER, and author’s calculations.

I haven’t checked for the inclusion of the foreign term spread a la Ahmed-Chinn (2022), but I’m confident it would raise the implied probability, as in this March post.

What this means is that, if historical correlations persist, then a recession (of some sort) is likely. (So, sure makes sense that Bill McBride/CR is on recession watch.)

The Cam Harvey link has a link to this on the same page:

https://www.bloomberg.com/news/articles/2023-06-02/summers-says-fed-should-mull-half-point-july-hike-if-june-a-skip?re_source=boa_related

The guy just won’t quit.