Does it matter if spreads are dis-inverting because short yields are falling, or long yields are rising? MacKenzie and McCormick (Bloomberg) say yes. With long yields rising…

If it looked at first glance as though the shift in the yield curve was a solidly positive sign — one indicating that the economy is now at less risk of a recession than it was — that’s probably not the case. True, it shows traders aren’t expecting the Fed to shift into firefighting mode soon. Even so, it’s almost certain to further dampen the economy as it ripples through to mortgages, credit cards and business loans. That will tighten financial conditions further, which may be a welcome development to the Fed. The risk, though, is that it hits the brakes so hard that the economy stalls completely.

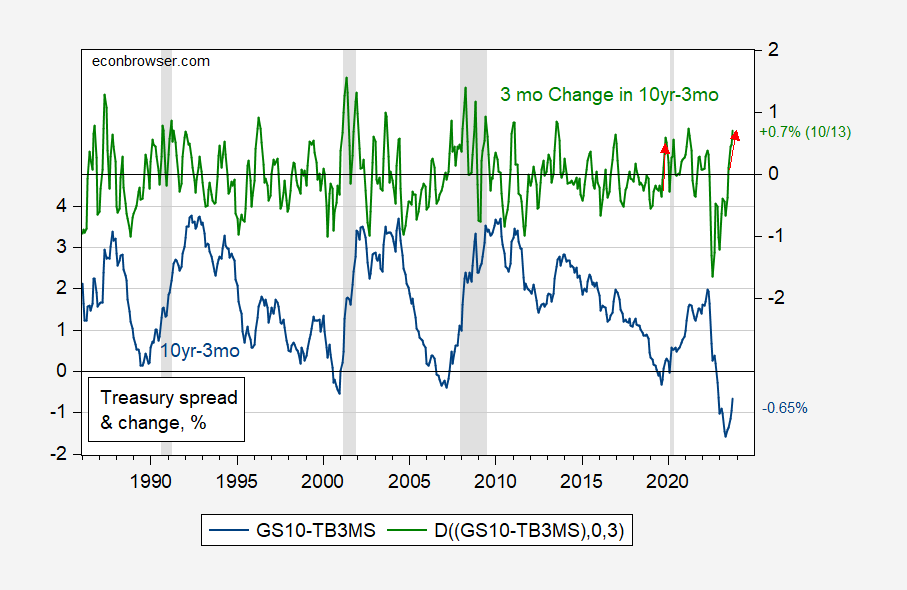

Does having a bull steepening prevent a recession? Figure 1, covering the Great Moderation, is somewhat conducive to that hypothesis, at least eyealling it. h

Figure 1: 10 year-3 month Treasury spread, % (blue, left scale), and 3 month change in 10yr-3mo spread, ppts (green, right scale). October observation for data through 10/13. NBER defined peak-to-trough recession dates shaded gray. Red arrows when 3 month change is positive during period when dis-inversion is occurring. Source: Treasury via FRED, NBER, and author’s calculations.

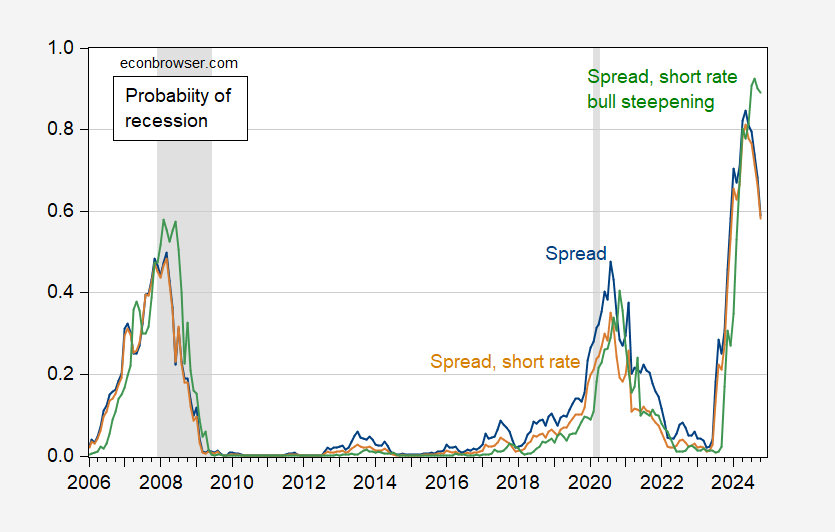

The evidence in favor of the bear steepening hypothesis is stronger when evaluating the proposition formally. I estimate probit models for (i) spread only, (ii) spread and short rate, and (iii) spread, short rate and 3 month change in spread. The 3 month change in spread is statistically significant and adds to the pseudo-R2.

(ii) Pr(recession=1)t+12 = 0.813 – 76.11spreadt + 9.80itshort

Pseudo-R2 = 0.28, Nobs = 241, bold denotes significant at 5% msl.

(iii) Pr(recession=1)t+12 = 0.736 – 98.37spreadt + 11.99itshort + 98.28Δ3spreadt

Pseudo-R2 = 0.34, Nobs = 241, bold denotes significant at 5% msl.

The recession probabilities are shown below.

Figure 2: Recession probability 12 month ahead estimated over the 1986-2023M10 period for spread (blue), for spread and short rate (tan), and spread, short rate, and 3 month change in spread (green). NBER defined peak-to-trough recession dates shaded gray. Source: NBER, and author’s calculations.

The bear-steepening specification implies 90% probability of recession in 2024M09, while it’s only 66.4% using the spread + short rate (peak probability for this specification is May 2024). Does this make me more pessimistic about avoiding a recession? Not really; the Ahmed-Chinn specification with the foreign term spread (but no steepening measure) was about 90.8% probability for September 2024.

Prof. Geoffrey Moore, the founder of ECRI, in his 1993 tome identified the change in yields in corporate bonds, as measured by the Dow Jones Bond Average, as a long leading indicator. His system did not make use of yield curve inversions at all.

A nearly identical result is true for BAA rated corporate bonds. Of the 17 recessions in the past century, BAA bond yields have been higher YoY 12 months before in 12 of them. Two of the 5 misfires were the pandemic and the 1938 fiscal contraction. The bigger the increase, the more likely a recession follows. If you use short term corporate paper as the measure, the relationship can be taken all the way back to the 1870s.

When we pare them with short term rates, as measured by YoY changes in the Fed funds rate, the record is even better. If corporate bond rates are up .8% or more YoY, and the Fed Funds rate has increased 1.5% or more in the past year, recessions have always followed with the exceptions of 1966 (saved by LBJ’s lavish “guns & butter” fiscal policy), 1984, and 1994. Here’s a link to the graph:

https://fred.stlouisfed.org/graph/fredgraph.png?g=1abrx

The nearly 10% decline in commodity (especially oil) prices beginning in June 2022, with some help from fiscal stimulus in the Inflation Reduction Act, kept us out of recession during that time. Unless geopolitical events drive them still lower, that stimulative effect is likely over. Which means the lagging effects of interest rate increases move to the fore.

The problem, of course, is that the simplest specification is under suspicion, what with recession not arriving in schedule. So we look to the details for confirmation.

If the neutral rate is much higher now, then a recession is less likely than simple rules suggest. If “This time is different” then simple rules are less reliable. In either case knowing that bears vs bull steepening made a difference in the past may not be useful.

Or maybe this recession is late in coming, but will arrive all the same.

Macroduck: Beginning of 10yr-3mo inversion was (on monthly basis) November 2022. With a variable window from 6 to 24 months, mean around a year, I hardly think the case is closed.

You know Menzie, I nearly always (genuinely) feel awkward and uncomfortable disagreeing with you or juxtaposing myself on a different side of something with you. But…….. you would possibly agree giving scholastic forecasters a 2 year error margin on an economic forecast is a low bar?? I certainly know real life market participants and private forecasters would pretty much let you saw off their left arm with a rusty jagged-ie saw for a two year error margin.

The only forecaster I know who allows himself that much margin, is Stevie Kopits’ self-imposed 75 year stretch to get his “Villagers toss Xi Jinping off the 10th floor terrace demanding Democracy” prediction correct.

Yeah, market types can’t make money this quarter (which is all that matters) on an 18-month-wide window. But the historic record gives you what it gives you.

I don’t think hiring can hold up forever, but so far…

If you look at rate hike cycles and the recessions that followed, the average length between the initial rate hike and the start of a bear market is 3.5 years, and it’s been 4.1 years between the initial hike and the start of a recession. At least according to the folks at Northwestern Mutual.

https://media.northwesternmutual.com/images/1100×618/fed-rates-long-term-market-performance-2022-03-028-02-04.webp

As long as we’re looking at rates as a predictor of economic conditions, let’s look at rates as a driver of economic conditions.

Higher rates have cut into demand for capital goods:

https://fred.stlouisfed.org/graph/?g=1abAR

And into residential fixed investment:

https://fred.stlouisfed.org/graph/?g=1a5vd

And have had a negative wealth effect:

https://fred.stlouisfed.org/graph/?g=1abAt

And have strengthened the dollar:

https://fred.stlouisfed.org/graph/?g=1abBp

So rates are working in the usual way to slow the economy.

But employment, which is typically slowed by the weakening in net exports, demand for fixed capital and the wealth effect, remains healthy:

https://fred.stlouisfed.org/graph/?g=1abCm

As a result, personal consumption also remains reasonably healthy:

https://fred.stlouisfed.org/graph/?g=1abDd

So perhaps we should be paying attention to leading indicators of hiring, like the NFIB hiring plans index:

https://www.nfib.com/foundations/research-center/monthly-reports/jobs-report/

So far, so good, though plans are translating into hiring at a slower pace; apparently, the low supply of qualified labor is slowing new hires.

Any thoughts on leading indicators of hiring?

Wait – you have actual evidence that higher interest rates might be curbing certain segments of aggregate demand? Now this is consistent with standard macroeconomics but you do know that JohnH is going to have a hissy fit.

Which is to say, Johnny’s going to write something.

Funny…It’s always interesting to see Ducky mention the negative impact of high interest rates on the “wealth effect” but fail to make any mention of high interest rates giving an income boost which may well be helping consumers maintain their spending spree.

And high rates haven’t yet slowed Real Private Nonresidential Fixed Investment Real Private Nonresidential Fixed Investment https://fred.stlouisfed.org/series/PNFIC1

Furthermore, multi-family construction spending seems to be perking along. https://www.statista.com/statistics/226511/value-of-us-multi-family-building-construction/

And even though (per Ducky’s first link) the asset value of corporate bonds has declined (negative wealth effect), the chart also shows that the value of shipments of machinery has been rising nicely.

So far, the knee-jerk standard dogma of “if higher rates, then recession” does not seem to be playing out. Maybe it’s time to give Sheila Bair’s piece some serious consideration: “Higher rates for longer are a good thing” https://www.ft.com/content/163db4c6-303d-4a52-9275-66359e4515e2?segmentId=b385c2ad-87ed-d8ff-aaec-0f8435cd42d9

For one thing, higher rates are good–not for the 1% whose “wealth effect” depends on low rates–but for those living on fixed incomes, saving for a new home, for their children’s college education, or for their own retirement…groups that have been largely ignored over the past decade in favor of making the fat cats obese

https://www.ft.com/content/163db4c6-303d-4a52-9275-66359e4515e2?segmentId=b385c2ad-87ed-d8ff-aaec-0f8435cd42d9

Well Jonny did write something but as usual it is nothing more than his usual trash. Dude – you are a bad joke.

“multi-family construction spending seems to be perking along.”

After all the fact that construction on single family homes does not count in Jonny boy’s cherry picking little world. Oh wait – I moved the goal posts. OK Jonny boy – put them back on the 30 yard line.

“the knee-jerk standard dogma of “if higher rates, then recession” does not seem to be playing out.”

The only person who said we were in a recession was YOU. Ah yes real GDI was falling even though profits were rising. Oh wait – real compensation was rising but in truth profits fell during this period.

Which is to say Jonny boy flip flops on a daily basis and he still gets everything wrong.

I think Johnny is rooting for higher rates BECAUSE he wants a recession. He pretends to think higher rates are great for the economy, but actually supports higher rates because:

– Johnny works for Putin, and Putin wants a recession in the U.S.

– Johnny works for Putin, and Putin wants the U.S. involved in squabbles about anything which causes internal divisions. Interest rates involve winners and losers, so Johnny wants to squabble about interest rates.

“The writer is a former chair of the US Federal Deposit Insurance Corporation and is a senior adviser to the Center for Financial Stability”.

Before Jonny boy pretends Republican lawyer Sheila Bair is some sort of champion of the little guy maybe he should check out who this Center for Financial Stability represents. Ah yes – rich people. After all the little guy tends to have a lot more financial debt than rich dudes. But little Jonny boy does not get that? Yes – little Jonny boy is THAT STUPID.

Johnny isback to throwing dust in the air because his positioning wildly wrong that it’s all he can do. Interest payments don’t have a positive wealth effect – that’s simply wrong. The fact that some economic activity is not contracting outright doesn’t mean interest rates aren’t having an effect on activity – that’s the whole point ofthe Fed’s “soft landing” hope. So on that claim, Johnny is again simply wrong. Johnny’s “so far, no recession” ignores what Menzie has written here and what many folks who are smarter than Johnny have concluded have discovered over the years.

When Johnny says higher interest rates are good for some groups, he is simply ignoring the cost to other groups. The rich are net lenders, the middle class net borrowers, so despite Johnny name-checking the 1%, he’s cheering for rich people when he cheers for higher interest payments.

Johnny seriously misunderstands how interest payments work in claiming a net positive wealth effect from higher interest rates. For every dollar of interest earned, a dollar has to be paid. The only net gain to the economy is when borrowing funds productive investment. Since some U.S. debt is held overseas, interest payments are a net drag on U.S. wealth – it’s just math.

Johnny doesn’t understand economics. He has demonstrated that repeatedly, and has done so again here. And he apparently doesn’t care. All he really wants to do is mislead. Like when he argues that Ukraine is wrong to defend itself against Russia.

the average household has far less in savings than they have in new and recurring debt. higher interest rates impact far more debt than savings for the average household. most people have very little in savings that is meant to be disposable income. the wealthy benefit from higher rates. our household is an example. my income has increased by the thousands this year due to higher interest rates. previous years that income was under a thousand dollars. i don’t carry any debt.

This is exactly right. Which is why little Jonny boy once again proves his is the dumbest troll God ever created.

Johnny wants us to believe that higher interest rates don’t have an effect on investment. He has been shown to be wrong, but he just keeps repeating his error. Johnny is a bit tricky with the evidence; he shows us a picture of real private non-residential fixed investment in levels. Oh, look! It’s going up!

Johnny only manages to show what he thinks is evidence that interest rates don’t affect investment by ignoring the subsidies for factory construction in the Inflation Reduction Act. Take out the subsidized sector and you see that a slower pace of investment follows the rise in interest rates, just as predicted in standard economics:

Real private non-residential fixed investment, with and without factory construction:

https://fred.stlouisfed.org/graph/?g=1agjV

Here’s the funny thing (if you think Johnny getting caught attempting a clumsy deception is funny) – Johnny got started on his “interest rates don’t matter” nonsense by pointing out that factory construction is rising despite higher interest rates. This time, Johnny hid factory construction among other forms of non-residential investment, trying to make it look like all non-residential fixed investment are unaffected by rates. Caught you, Johnny.

Johnny doesn’t seem capable of making a good-faith argument. Naughty, naughty, little Johnny.

When it comes to GDP; consumption is the 350 pound Gorilla. Until rate hikes have normal predicted effects on employment and consumption I would say that this time its different – and in a way that can be explained and connected to GDP.

EU natural gas prices soared on mostly supply issues, but some related to demand on colder than normal winter forecasts. I’ll be surprised if it ends up that cold, but we’ll see.

I wonder if our man Kopits has looked at the 2-year graph on WTI ?? Funny the things Kopits notices and the things he misses.

https://tradingeconomics.com/commodity/eu-natural-gas

EU Natural Gas price has risen of late but it where it was back in February.

As far as WTI prices – back to where they were two years ago. But little Stevie insists they will top $100 a barrel any day now. And no one can refute his forecast record since he does not bother to track his own forecast errors.

Still reading little rumblings about the Treasury market, liquidity, auctions not going splendidly shall we say. This still bears being watched. I saw some commenters in other threads erroneously attacking Macroduck for his warnings about Treasuries possibly being a problem. I wanted to defend Macroduck, but felt it better to keep quiet until I get a better grip on the issue. But I do think Treasuries, and market appetite for Treasury auctions, really merits being watched closely right now.

Gracias, my friend.

So on the one hand, the recent bond (30-year) auction showed signs of weakening demand. In particular, primary dealers have had to absorb more of the auction than normal; that’s their job:

https://finance.yahoo.com/news/treasury-bond-auction-runs-weak-034418412.html

On the other hand, the overall size of the bid relative to the auction size has remained fairly stead in recent ten-year note auctions:

https://en.macromicro.me/collections/51/us-treasury-bond/30431/us-10y-bid-to-cover-ratio

A quick look has not turned up historical data for other auction maturities. If I feel energetic, I’ll find more data.

Off topic but big news. I always knew Micrsoft had diverted a lot of its profits to tax havens but DAMN!

https://tech.co/news/microsoft-owes-the-irs-29-billion

Microsoft Owes the IRS $29 Billion, But It’s Refusing to Pay

Microsoft and the IRS’s tussle marks the biggest corporate tax dispute in US history, with the tech giant fighting back.

Microsoft currently owes the US Treasury $28.9 billion in back taxes, interest, and late payment fees, according to a recent notice from the Internal Revenue Service (IRS). In what is on track to become the biggest corporate tax dispute on record, the case revolves around Microsoft’s use of ‘transfer pricing’ between 2004 and 2013 – a tax avoidance practice that other big tech companies like Amazon have also been found guilty of. Microsoft has been fast to dispute these accusations, launching a formal appeal and claiming it would challenge the IRS in court if necessary.

Treasury occasionally estimates the amount of unpaid taxes. Most estimates show unpaid taxes in any year roughly equal to that year’s fiscal deficit.

Marshal taught us that economic efficiency occurs when the marginal this is equal to the marginal that (he was not alone). Every new dollar in the IRS budget brings in several new dollars in additional revenue, so the marginal cost of IRS operation is still well below its marginal revenue. Not efficient.

That must be why Congressional Republicans demanded a $20 billion reduction in the IRS budget as the price for passing the most recent continuing budget resolution. They are soooo serious about the deficit, the rule of law and stuff.

Since this audit covers the 2004-2013 period, I took a look at their 10K filings from 10 years ago. Cliff notes version. Worldwide revenues near $75 billion per year with profits near $25 billion. Half of its sales are to US customers and all of its R&D is done in the US.

But only $5 billion per year of its profits (20%) was sourced to the US parent. Just wow. The IRS is proposing what appears to be an increase in US profits near $10 billion per year (taking that 20% to 60%). Sounds reasonable to me.

But be warned – Microsoft hires very expensive tax attorneys who can spin faster than Lawrence Kudlow.

Trump Manages to Make Israel Attack All About Him

https://nymag.com/intelligencer/2023/10/trump-manages-to-make-israel-attack-all-about-him.html

Trump suddenly has a lot more to say about Israel since he has realized the attack was actually all about the primary topic he does have an organic interest in: himself. During a campaign rally in West Palm Beach on Wednesday, Trump tied the attack to his “stolen” 2020 election lies, aired his personal grievances against Israeli prime minister Benjamin Netanyahu, and repeatedly called the Lebanon-based militant organization Hezbollah, which has been clashing with the Israeli Army this week, “very smart.” … Trump’s criticism of Netanyahu is a bit more surprising as the two were close allies throughout his time in the White House and Trump insists he’s the most pro-Israel president ever. But in the final weeks of his administration, Trump turned his back on Netanyahu. (He actually told a journalist, “Fuck him.”) The Israeli leader’s crime: publicly congratulating President-elect Biden on his win.

While there are certainly many legitimate reasons to criticize Netanyahu at the moment, Trump instead focused on personal gripes. During the speech, he told a story he claimed he had never told before about the U.S. operation to assassinate Iranian general Qasem Soleimani in 2020. (“They’ll say, ‘Oh, it’s classified information.’ Well, maybe it is, but I don’t think so,” he mused aloud.) Trump said Israel had been collaborating with the U.S. on the plan for the operation but pulled out at the last minute. “I’ll never forget that Bibi Netanyahu let us down. That was a very terrible thing,” Trump said. “So we were disappointed by that. Very disappointed. But we did the job ourself. It was absolute precision, magnificent, beautiful job. And then Bibi tried to take credit for it. That didn’t make me feel too good. But that’s all right.”

General Frank McKenzie was asked about Trump’s claim over the 2020 operation to assassinate Iranian general Qasem Soleimani in 2020. It seems Trump made up this claim that Israel pulled out. Poor little baby – his little temper tantrums are insulting to one of our closest allies. But it all has to be about baby Trump.

I kept wondering, and wasn’t hearing a lot of open discussion about, “How did Hamas get past Israel’s ‘Iron Dome’ etc.??”. That one was really puzzling me. Maybe in this article lies some of the answer, which could be “the elephant in the room” as far as Israeli intelligence and defense ministries are concerned.

https://www.politico.com/news/2023/10/15/hackers-israel-hamas-war-00121593

But it has to be FIXED. And things don’t get FIXED if they are not discussed. Whether that is good or bad for a mid-20th century minded (and corrupt) Netanyahu or not, it still has to be discussed to be FIXED.

“Hacking groups with links to countries including Iran and Russia have launched a series of cyberattacks and online campaigns against Israel over the past week, some that may have even occurred in the runup to the Oct. 7 strike by Hamas. On Telegram, hacking teams claimed they compromised websites, the Israeli electric grid, a rocket alert app and the Iron Dome missile defense system. At least one Israeli newspaper, The Jerusalem Post, acknowledged hackers took down its site temporarily. It’s unclear how far and deep the cyberattacks went. But the online campaigns show an effort to bolster the physical onslaught with a digital offensive, potentially looking to replicate the way Russia and sympathetic hacktivists buffeted Ukraine with cyber strikes in the first days of that war.”

Is Putin behind this as well? That may explain why Trump has turned pro-Hamas.

A few days ago, I linked to a piece by Noah Smith (https://www.noahpinion.blog/p/youre-not-going-to-like-what-comes) in which he describes the U.S. as a defender of the status quo, while Russia is “revisionist”. He pretty clearly means Russia wants to “revise” reality; Putin is unhappy with Russia’s second-class status. This dichotomy makes sense, since the U.S. is the author of much of the current ordering of the world and Russia is a former great power embarrassing itself on the battlefield.

Smith’s claim is that Russia wants to stir things up both because it is “revisionist” and because it can use unrest as an opportunity to make a show of diplomacy. The two can operate sequentially – make trouble and then offer to mediate.

As long as Russia is trying to take Ukranian territory through violent means, stirring up trouble elsewhere serves the particular goal of diverting attention and resources away from aiding Ukraine. So yeah, there’s reason to suspect Russian involvement. Evidence? Well, let’s see what floats up.

Forgot to mention –

Th U.S. was brokering a peace deal between Saudi Arabia and Israel. From the Russian perspective, that deal would have raised U.S. status, lowered oil prices and secured greater odds of peace and prosperity In the region while Russia has “revisionist” interests. When Hamas induced Israel to kill non-combatant Palestinians, the deal was shelved. That’s in Russia’s interest.

It’s a little hard for me to decipher this, not being familiar with Poland’s set-up. But it seems like a win for Democracy, as far as I can tell.

https://www.politico.eu/article/opposition-wins-polish-election-according-to-exit-poll-poland-kaczynski-duda-tusk-election-rule-of-law/

So, I would say it’s good news.

Kids, remember the wisdom that Uncle Moses imparts to you, so life is less confusing in your burgeoning years: Love is fleeting.

https://www.politico.com/news/2023/10/15/boebert-campaign-cash-beetlejuice-bar-00121606

Also, watch out for stubble on women’s faces and tube-like animals hiding under skirts.

https://www.newsweek.com/lauren-boeberts-date-own-drag-show-bar-1827636

Film of the couple being escorted out. Watch to the end and check out the faces of the two ladies. Classic.

HI Menzie,

Off topic: With its 10th Anniversary – what is your take on China’s Belt and Road Initiative – ? Has it increased economic activity in the Global South? (By the way, one of the most ironic things about Trump’s trade war – to me – was to make China pay more – but all it did was to force China to find other more reliable suppliers and markets. For example, Brazil has now overtaken the U.S. as the leading supplier of soybeans to China.) https://www.scmp.com/news/china/series/3238042/10-years-chinas-belt-and-road-initiative

pgl,

You’ve seen this?

https://www.justice.gov/opa/pr/justice-department-sues-agri-stats-operating-extensive-information-exchanges-among-meat

Thanks for letting us know:

The Justice Department filed a civil antitrust lawsuit against Agri Stats Inc. today for organizing and managing anticompetitive information exchanges among broiler chicken, pork and turkey processors. The complaint alleges that Agri Stats violated Section 1 of the Sherman Act by collecting, integrating and distributing competitively sensitive information related to price, cost and output among competing meat processors. This conduct harms customers, including grocery stores and American families.

I never heard of Agri Stats but what they do is textbook collusion. Which hurts competition and is indeed violating our anti-trust laws.

Agri Stats was founded in 1985 on a kitchen table in the USA’s heartland. Our founder, Jim Cox, started this business as a way to help industry participants make informed decisions based on accurate user data; delivered in a timely manner, and with the utmost confidentiality. Since retired, Jim has passed that legacy on. While we have increased both the scope of the reports and breadth of participation, we tirelessly strive to uphold the values of providing accurate, timely, and confidential data for our customers to make informed decisions to improve their bottom line profitability. From his kitchen table to now a 17,000 square foot facility in Fort Wayne, IN, we have over 100 employees dedicated to servicing our customers.

https://agristats.com/history

38 years illegally restraining competition.

David Dayen is all over this:

https://prospect.org/power/2023-10-03-lawsuit-highlights-why-meat-overpriced/

But a separate case from the Department of Justice against an agricultural analyst service called Agri Stats is perhaps the most emblematic of the old patterns of corporate America, and the new aggressiveness of this wave of antitrust enforcement.

Agri Stats, as described in the complaint, is essentially a work-around for explicit collusion by meat processors. The company delivers weekly reports based on proprietary data given to them by meat processors, which have so much granular detail that everyone in the industry knows precisely what everyone else is doing, including the prices they’re offering. This allows for specific coordination that raises prices for everyone purchasing meat, while boosting profits for the processor middlemen.

More from David Dayen

What’s incredible, after reading this case, is that Agri Stats has been allowed to exist out in the open for nearly 40 years. There are similar third-party facilitators in other industries, like the airline-owned Airline Tariff Publishing Company, which publishes up-to-the-minute airfares for over 500 airlines numerous times per day. The Justice Department sued ATPCO in 1992 for price-fixing, but it ended in a settlement that didn’t fundamentally change the business. It took 30 years for a new DOJ to bring essentially the same complaint against Agri Stats, with a mountain of data to back it up.

The conduct quoted in the lawsuit goes back to 2009, and there has been enough private antitrust litigation against Agri Stats that it shut down reports on two main lines of business—turkey and pork—four years ago. (Broiler chicken reports are still distributed.) Successive Justice Departments, for four decades, saw nothing wrong with a company that coordinates an entire industry on how to raise prices, in some cases explicitly according to the lawsuit. The muscles of antitrust were so shriveled that even the most obvious misconduct was ignored. It’s definitely a new day.

Agri Stats has not responded to a request for comment.

AGRI STATS WAS FOUNDED IN 1985 by an Indiana poultry consultant, “as a way to help industry participants make informed decisions based on accurate user data; delivered in a timely manner, and with the utmost confidentiality.” Bizarrely, the company fell into the hands of pharmaceutical giant Eli Lilly in 2013, which held it for five years until pressure from antitrust lawsuits led to a sale. Today, four individual Agri Stats executives and two foreign nationals own the company, funded through a Swiss venture capital firm.

The company essentially recruits the leading meat processors, all of which compete with one another, into its information-exchange service. The lawsuit states that the participating companies, which are listed in its reports, comprise at least 90 percent of the market for broiler chicken, 80 percent of the market for pork, and 90 percent for turkey. (Agri Stats estimates that those numbers are even higher.)

Agri Stats offers a “give-to-get” policy: If processors give up complete information for all their facilities, they will get complete information for everyone else’s. It sets up what is described as an automated “direct download” of key information from the various processors; none of it is survey data. It’s just precise, weekly information about births of livestock, raising and slaughter of animals, packaging and cutting of meats, and delivery to grocery stores, complete with production costs (including labor wages and benefits) and prices charged to customers.

Thanks for sharing this. David Dayen has been one of the best financial journalists out there. I have to confess I hadn’t read him in awhile, but he is always worth the time.

Lisa Desjardins on the Speakership (they will blather tonight for weirdos like me that used to watch C-SPAN in their teens. Yeah, you guessed it, about zero friends):

https://www.pbs.org/newshour/show/house-enters-3rd-week-without-speaker-as-gop-infighting-keeps-congress-at-standstill

I will try to put up a “Politico” link before 21:00 Pacific Time tonight in this or most recent thread if I see anything I feel is above average insightful.

This seems like the best rundown I could find. I was thinking they were gonna debate late into the evening, but apparently they broke early evening to meet again tomorrow (Tues) at noon:

https://www.politico.com/live-updates/2023/10/16/congress/jordan-gains-critical-traction-00121758

A vote for paterno. Disgusting.

A jerry sandusky reference?? Yeah paterno is in the same boat with Jordan, I agree. In my younger years (prior to the sandusky “open secret” being revealed to the broader public, I’m embarrassed to say I was a big joe paterno fan. I bought his whole “the student athlete” schlock. I’ve told this blog I think I am very perceptive about people and can tell the bad apples from the good apples pretty quickly. But I do get it wrong sometimes. And I TOTALLY let paterno blow smoke up my skirt pre-sandusky, I cannot deny it.

But friend Baffling, there are still those out there, seemingly controlled by geographic and fraternal bias, who still believe in the “purity” of joe pa.

i used to be a fan of joe pa. but as a parent, i see his abdication of responsibility as morally reprehensible today. no amount of good that he did can right the wrong he allowed to occur. he is a fallen hero in my book. jordan is no different. he failed in his moral responsibility and duties. and to reward somebody with such a flawed moral compass with the house speaker position? exactly what are republicans thinking?

trump, sexual assault, becomes president

hasert, sexual molestation of boys, speaker

kavanaugh, sexual assault, supreme court

jordan, cover up of sexual molestation of boys, speaker??

seriously, you can’t make this sh!t up. i have no confidence that jordan is able to do the right thing when called upon. he failed miserably already. he was an enabler of child molestation. and i support those wrestlers 100% in bringing this to light today.

“kavanaugh, sexual assault, supreme court”

Baffling’s interesting list needs one more:

Clarence Thomas, sexual harassment, supreme court

Voting now. Of the first 100 votes – 5 Republicans have already voted for some than Jordan with the Dems sticking with Jeffries. Jordan is not going to win on round 1.

Almost done with round one voting:

Jeffries 212

Jordan 200

Other Republicans 19

Not voting 2

I think this is it. So Jordan did worse than McCarthy in the 1st round.

Correction – all 432 voted eventually

Jeffries 212

Jordan 200

Other Republicans 20

Are there 5 Republicans that would rather vote for Jeffries than Jordan, both begin with a J

Problem with right wingers and other authoritarians is the deep inside they believe in right and might – not democracy. They will bully, threaten and finally bribe those who don’t support them. What kind of bribes will Jordan offer.

A lot of Jordan’s GOP detractors are appropriation Chairs and he has been hard core voting against the appropriation bills those people send to the speaker. Will they demand that any appropriation bill going out of committee must be voted on, no more than 5 days later?

My understanding is (and I’m happy to be corrected if I am wrong) that there are ways this can play out that Jordan can win with only 213 votes. So that would be like if some House members who strongly dislike Jordan just voted “present”. So, if we’re keeping count here, Jordan needs 13 more Republican votes.

Yes Jordan needs the majority of the votes for a candidate – so if some of the people who are not pleased with Jordan don’t vote, the threshold will be less. But they better get that one organized well. If too many decide to vote present they could end up with Jeffries 212, Jordan 211 and the rest just voting present. That would be equally “interesting” (Democratic speaker in a GOP majority house), but at least more fun.

the problem with the present votes, is if the right combination of present and “other” occurs, jeffries gets elected. now that would not last for long, mind you, but it requires a very coordinated approach by the republicans. right now the republican party is a dumpster fire. and it is all because of a handful of maga fools. even with they have the majority, they can’t get their act together.

Another vote today and the prediction is that Jordan will get less than 200 votes this time.

Can someone state the obvious? No sane person likes Jim Jordan.

Forecasting is forecasting is forecasting. That said, I do not recall a period where recession forecasts were repeatedly extended into the future like this.

Now the WSJ survey of economists is saying the probability of a recession is less than 50%.

Bullish for oil prices. Perhaps not so bullish for incumbent re-election in 2024.

“Funny…It’s always interesting to see Ducky mention the negative impact of high interest rates on the “wealth effect” but fail to make any mention of high interest rates giving an income boost which may well be helping consumers maintain their spending spree.” -JohnH

High interest rates will clearly benefit conservative savers, especially those who are not financially sophisticated.

Near term, higher interest rates mean higher borrowing costs and will negatively impact capital expenditures by consumers and business investment. Private investment is the most volatile component of GDP. GDP is what is typically used to monitor ‘economic growth’.

Y = C + I + (X-M) Income = consumption + investment + net exports

“High interest rates will clearly benefit conservative savers, especially those who are not financially sophisticated.”

Yep. Conservative savers are savers. Saving isn’t spending. Borrowers, on the other hand, spend to to the point that they need to borrow. The idea that higher interest rates “may well be helping consumers maintain their spending spree” is simply nonsense, a complete misunderstanding of the flow of funds in an economy. Savers lend to spenders.

There is often some group which benefits from what hurts others – savers benefit from higher rates at the expense of borrowers. To focus on one and ignore the other, as Johnny has done, is a fundamental error in thinking.

Borrowing funds spending. Higher rates restrain borrowing. Higher rates restrain spending. It’s that simple.

It is simple. Tying one’s own shoe laces is simple too but little Jonny never learned to do that either.

Discounted Cash Flow (DCF) is perhaps the most basic building block in financial economics. But something tells me that little Jonny boy has never heard of DCF. After all – the value of any asset rises if expected future cash flows go up. But little Jonny boy has never figured this out when it comes to real world applications.

Furthermore DCF falls if the cost of capital rises. But time after time – little Jonny boy tries to deny that. Maybe little Jonny boy does not know his incessantly stupid rants deny basic financial economics. Then again little Jonny boy does not know the meaning of a lot of the stupid things he writes.

The Energy Information Administration has released its home heating cost estimates for the coming winter:

https://www.eia.gov/outlooks/steo/report/perspectives/2023/10-winterfuels/article.php#casetab4

The upshot is that lower natural gas prices, steady electricity prices and warmer weather on average will mean steady to lower home heating costs compared to last winter.

The National Energy Assistance Directors Association offers a similar outlook (of course), including a table showing average heating costs this coming winter likely to be lower than those for the past two winters (hit the link to the pdf):

neada.org

Should give a modest boost to disposable income and consumption.