In Chinn and Ferrara (2024), we find substantial explanatory power for the 10yr-3mo, the 3 month rate, and the debt service ratio for German recessions (our analysis we also covered Canada, France, Italy, Japan, Sweden, and UK). Our sample extended up to 2022M12 (using spreads up to 2021M12), as we were unsure about recession in 2023. With Germany in a possible slowdown, it’s of interest to consider what our model would have predicted.

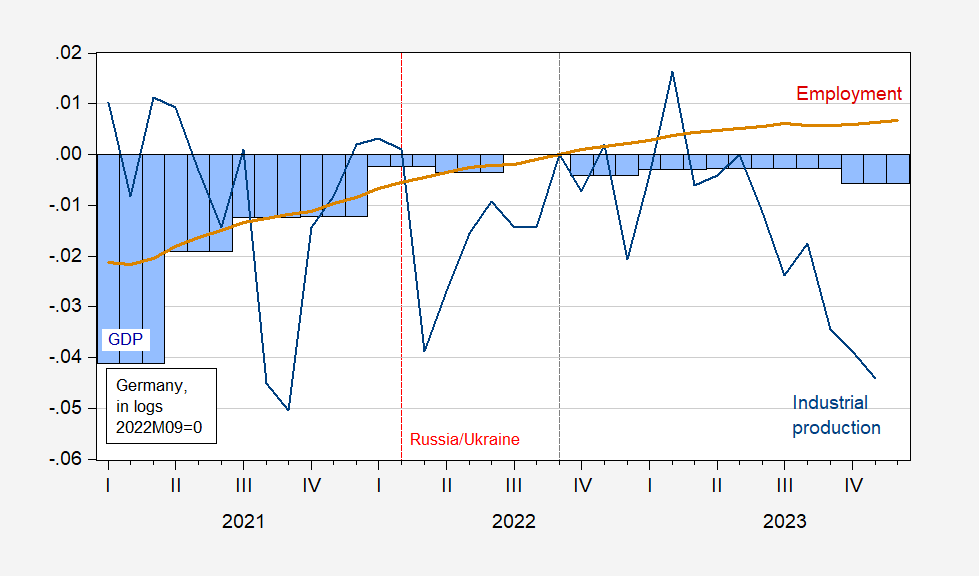

Figure 1: GDP in constant euros (blue), industrial production excluding construction (blue line), employment (red line), all in logs, 2022M09=0. Source: Eurostat, MEI via FRED, and author’s calculations.

The last peak in GDP is at 2022Q3. Peak industrial production is February 2023, while employment has continued its rise, pausing at 2023M07. I tentatively set the recession start date then. It’s important to note that neither the German Council of Economic Experts, nor ECRI have established a peak, so this is an assumption on my part. (Laurent Ferrara provides a chronology which extends up to 2019, as described here).

Suppose I estimate a probit regression over the period up to just before the expanded Russian invasion of Ukraine, i.e., 1985 to 2021M12 (using the spread, short rate (i3mo), and debt-service ratio (dsr) up to 2020M12) to estimate the year-ahead recession probability. The estimates are:

Pr(rec=1) = -4.85 – 60.6 spread + 5.7 i3mo + 33.9 dsr

Pseudo-R2 = 0.32, Nobs = 430, Smpl for spread, etc. 85M01-20M12. Bold face denotes significance at 10% msl.

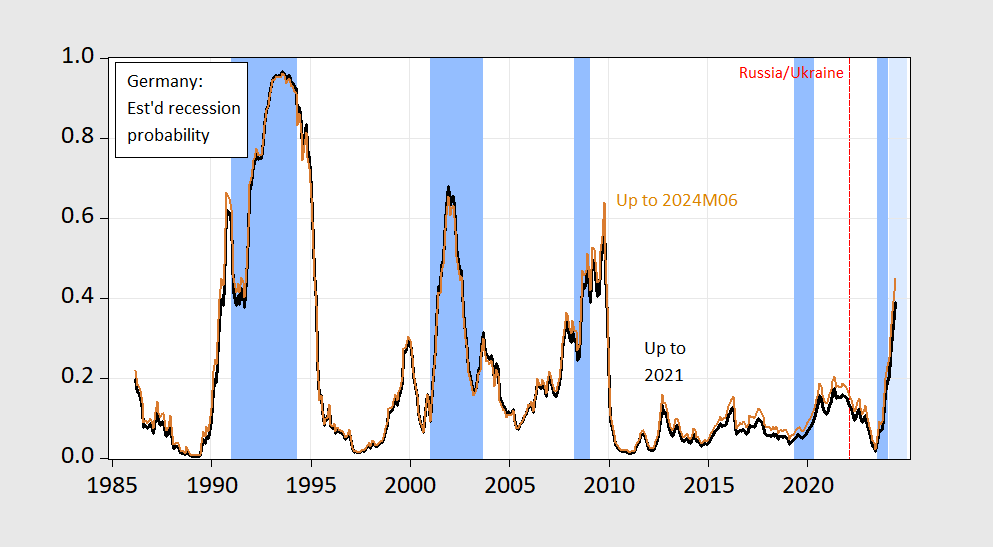

The estimates of recession probabilities are shown in black, with ECRI defined recession dates shaded light blue, where I have assumed last peak at 2023M07.

Figure 2: Estimated probability of recession using probit models estimated up to 2021M12 (black), estimated up to 2024M01 (tan). ECRI defined peak-to-trough recession dates shaded light blue. Source: ECRI, author’s calculations.

Note that the regression misses the 2020 pandemic recession, although the probabilities do rise from a very low level. The probability of recession for 2024M01 is 19%.

Suppose I use the entire sample period up to 2024M01 (and hence the spread and other determinants up to 2023M01). Then one obtains the following estimates:

Pr(rec=1) = -4.05 – 59.7 spread + 6.54 i3mo + 27.8 dsr

Pseudo-R2 = 0.29, Nobs = 455, Smpl for spread, etc. 85M01-23M01. Bold face denotes significance at 10% msl.

The estimated probabilities for this regression are much the same, with a slightly higher probability for January 2024, at 23%.

In both cases, it doesn’t seem that the model would predict a recession at the time they are likely to have started. That being said, nobody has confirmed an ongoing recession in either Germany or the Euro area.

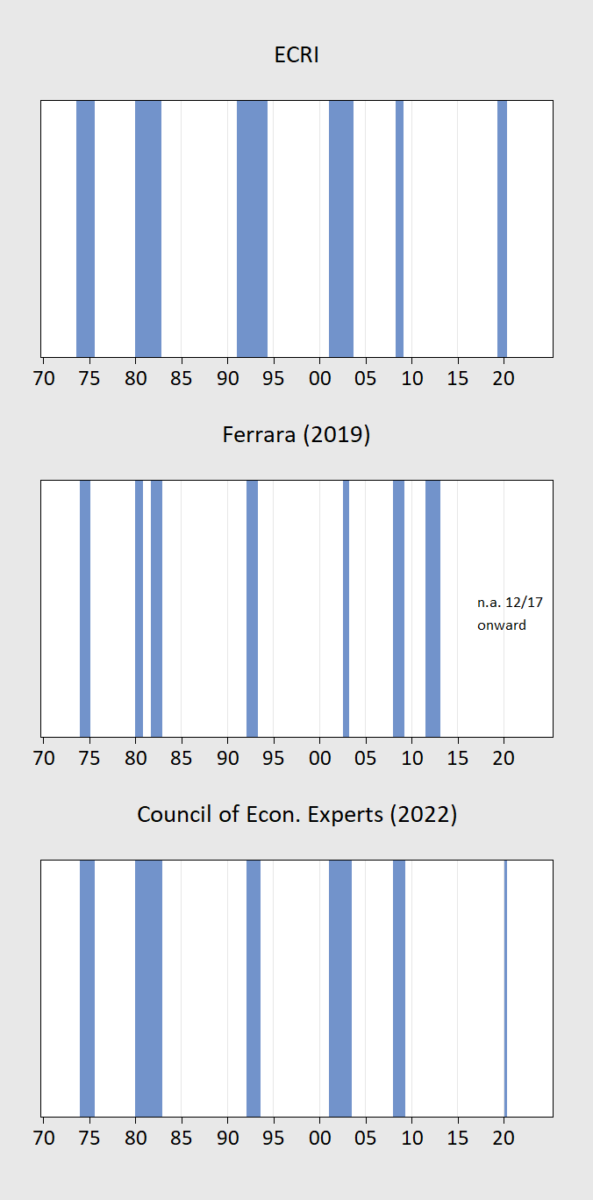

Note that there are different results if one uses different chronologies, two of which (from Ferrara (2019), and GCEE (2022)) are shown below.

Notes: All recession dates peak-to-trough shaded light blue. Sources: ECRI, Ferrara (2019), German CEE (2022).

The answers to both questions, then, are (1) maybe, and (2) maybe.

From Euronews in October, 2023: https://www.euronews.com/business/2023/09/23/germany-went-from-envy-of-the-world-to-the-worst-performing-major-developed-economy-what-h

Brucie ducks the question in the headline “what happened”. Maybe Brucie boy finally realized that Germany’s export/GDP ratio us much higher than China’s so little Brucie boy in all his fake knowledge of basic economics thinks the problem is that Germany’s economy is too open to trade. Of course little Brucie boy has not said that as he has not received the email from Kelly Anne Conway.

Nobody may have yet confirmed a recession in Germany, but the outlook is not good: “Germany’s days as an industrial superpower are coming to an end…

The underpinnings of Germany’s industrial machine have fallen like dominoes. The US is drifting away from Europe and is seeking to compete with its transatlantic allies for climate investment. China is becoming a bigger rival and is no longer an insatiable buyer of German goods. The final blow for some heavy manufacturers was the end of huge volumes of cheap Russian natural gas.”

https://www.bostonglobe.com/2024/02/10/business/germanys-days-an-industrial-superpower-are-coming-an-end/

The question is–why have China’s potential problems garnered so much attention among commenters here while Germany’s so little? Could it be that, as some have suggested, that Germany was the real target of Russia sanctions and the destruction of NordStream II?

JohnH: If you read Bloomberg instead of the Scheerpost, maybe you wouldn’t be wondering.

Scheerpost? If I recall, I recently linked to Jeffrey Sachs and Jaimie Galbraith and their assessments of the Chinese economy in the context of US politics.

OK. The Boston Globe piece was also published by Bloomberg. And here is a another Bloomberg piece: “ Europe’s Economic Engine Is Breaking Down… Germany is at risk of a long, slow decline — with consequences for the whole of the EU.” https://www.bloomberg.com/news/articles/2023-05-25/germany-enters-recession-europe-s-largest-economy-is-breaking-down

Europe’s growth engine is breaking down? It sounds as newsworthy as China’s problems to me, yet there is a constant stream of negative commentary here about one and almost nothing about the other.

Complaining about little coverage of Germany’s problems in a post discussing the strong possibility of recession in Germany. This possibly ranks in the top 5 of reading comprehension howlers on this blog.

I have found in the past you can get around the Bloomberg paywall by using BNN Bloomberg (the Canadian version of Bloomberg). I always hesitate sharing these things as if more people do it they are more apt to slice off “the workaround”.

I don’t know why I am sharing this with an idiot who won’t use it anyway, but this naive childish part of my personality can’t seem to not give people the benefit of the doubt.

Is that the same idiot who never learned how to read 10-K filings at http://www.sec.gov or the data on national income by factor at http://www.bea.gov?

“why have China’s potential problems garnered so much attention among commenters here while Germany’s so little?”

I read two links to Germany’s issues in this comment section alone. Then again the links were provided by two morons – you and Bruce Hall.