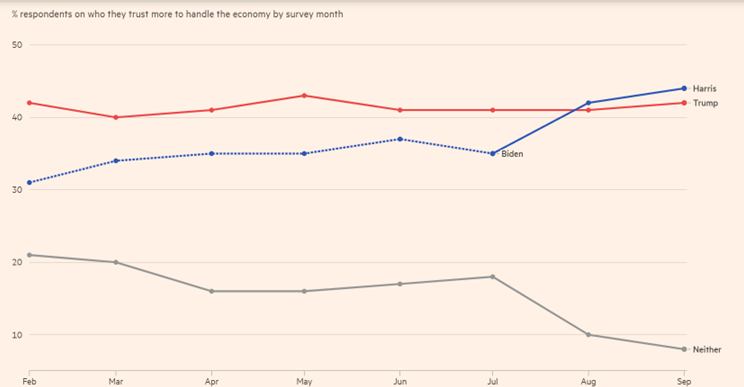

Who would do better, according to the FT today:

Source: FT, 16 Sep 2024.

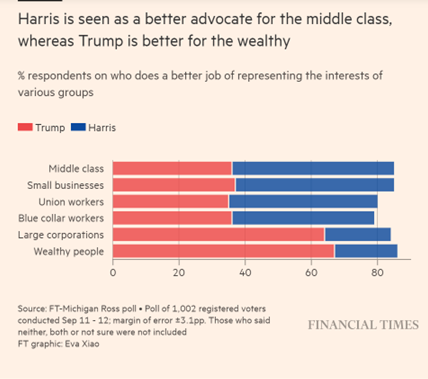

And who would benefit from the policies of respective candidates?

Source: FT, 16 Sep 2024.

Who would do better, according to the FT today:

Source: FT, 16 Sep 2024.

And who would benefit from the policies of respective candidates?

Source: FT, 16 Sep 2024.

That 2nd graph in the post is all you need to know Americans just do not like reading.

johnny Cuckrant’s latest comedy monologue:

https://www.grumpy-economist.com/p/monetary-ignorance-monetary-transmission

Oh dear – now I have to read something even worse than Steven Koptis suppression theory.

Hell hath no fury like a jilted prof who didn’t get his entitled invitation to Jackson Hole.

Get ready. The first time Grumpy Cuckrant receives a bad answer from his doctor on his annual prostate exam Johnny Cuckrant’s next 30 WSJ editorials will scream to us that the medical profession “has now become politicized”. ‘Cuz……. like…… that’s how Johnny rolls.

“There is a Standard Doctrine, explained regularly by the Fed, other central banks, and commentators, and economics classes that don’t sweat the equations too hard”

Jonny boy is such a arrogant turd. I read his babble and it was just that – long winded babble. MMT makes more sense. Even Village Idiot Steven Koptis makes more sense.

Cochran is mighty doctrinaire here. The formation of real-world inflation expectations MUST follow theory as he conceives it:

“A rise in interest rates must raise expected future inflation…”

I understand Cochran is offering a critique of theory, so a deviation of reality from theory is his point. Given Cochran’s frequent trouble with the truth, we can afford to suspect he has stated theory wrongly in an effort to make a contrarian point.

Where might he have gone wrong? Well, he says money and bonds are the same if both pay interest and if we can pay for things with bonds. But money and bonds don’t pay the same interest. And we don’t actually pay with bonds; we use bonds as collateral, borrow money and pay with money. Is liquidity not part of the picture? Do transaction costs not matter?

The “unexpected inflation” and “hyper-inflation/deflation” part of Cochran’s argument strikes me as la-la land imaginings. He hasn’t actually presented a mechanism by which Schrödinger’s cat is the future inflation rate. He simply declares that to be part of the “real” state of theory which everyone else chooses not to talk about. Again, reality isn’t Cochran’s “thing” in this essay, but in reality, hyper-inflation is the result of governmental collapse. Positing hyper-inflation, or hyper-inflation, as merely the result of monetary policy is detached from reality.Maybe I’m too poorly read in the monetary literature to have caught this part of standard theory?

It just seems to me that Cochran is leaving out anything that doesn’t allow him to make a showy demonstration of contrarian dazzle and making up things that do.

To a simpleton like me, interest rates are the cost of borrowed money. When rates are high, only investments which pay a high return will be undertaken because borrowed money finances investment, and that means fewer projects than at lower interest rates. By only addressing financial concepts, and by simplifying those concepts in tricky ways, Cochran convinces himself that he understands something that no other economist has understood. Pretty arrogant.

In the end, Cochran likes a fiscal explanation. Don’t we all? But his version of fiscal explanation sounds an awful lot like MMT, the whole history of which is to pretend that repackaging long-undedstood concepts amounts to seeing things others can’t see.

Perhaps someone more familiar with the ins and outs of monetary theory – not Modern, if you please – can think through Cochran’s argument more clearly than I have.

Thanks for taking the time to do a real critique. On Jonny boy’s

“A rise in interest rates must raise expected future inflation…”

That reminds me of the babble from Steven Koptis on Russian interest rates. Birds of a feather.

Some of his lying seems very intentional, impossible for me to believe he isn’t aware at least some of his statements are factually wrong. But some of his statements go so off-the-rails as to be self-damaging to his reputation (such that it is) and makes me wonder if his wild-eyed cacophony isn’t a byproduct of bipolar disorder.

“he says money and bonds are the same”

I’m jumping on this for a reason. Grumpy like Greenspan prefer higher bank equity requirements over regulation which sort of makes sense (I’d do both) but Greenspan sensibly wanted equity requirements to be 20% of total assets whereas Grumpy advocates 100% equity. Now his equity money idea would take away the prospect of households wanting a safe private asset, which strikes me as bat$hit insane. Then again – most of his views on economics are bizarro world.

You would think a finance professor would know better than such statements but not Grumpy.

Should have been “hyper-inflation, or hyper-deflation…”

Harris and Walz have done a good job of articulating their economic policies of opportunity for all in contrast to Trump/Vance – xenophobic mass deportation, tax cuts for billionaires, widespread (not targeted tariffs) tariffs/tax on imported goods, and repealing healthcare and replacing it with some “concepts” –

I expect to see more of more of failing Trump trying to re-frame the media narrative to focus on Trump’s b.s. – derogatory gestures to dead soldiers at Arlington, taking a 9/11 denier to 9/11 memorial, repeating and promoting xenophobic and baseless smears against people – causing school kids to be evacuated from threats. Trump’s harmful and violent tirades do have consequences.

We all know that Sen. John Kennedy (R-La.) is a total jerk but DAMN!

https://www.msn.com/en-us/news/politics/gop-sen-john-kennedy-to-arab-american-witness-you-support-hamas-don-t-you/ar-AA1qJdzo?ocid=msedgdhp&pc=U531&cvid=14279b9456574a489c69c50c1fe013be&ei=10

Sen. John Kennedy (R-La.) on Tuesday baselessly accused an Arab American witness of supporting terrorists during a Senate hearing, and as she called out his blatant Islamophobia, the GOP senator told her to “hide her head in a bag.” Kennedy lashed out at Maya Berry, executive director of the Arab American Institute, a nonpartisan national civil rights advocacy organization, during her testimony before a Senate Judiciary Committee hearing focused on stemming hate crimes. Berry was the only Muslim witness in the hearing. “You support Hamas, do you not?” Kennedy abruptly asked Berry, referring to the terrorist group behind the Oct. 7 attacks on southern Israel. His question drew audible gasps in the audience.

“Senator, oddly enough, I’m going to say thank you for that question, because it demonstrates the purpose of our hearing today,” Berry responded. “Hamas is a foreign terrorist organization that I do not support. But you asking the executive director of the Arab American Institute that question very much puts the focus on the issue of hate in our country.”

Several people in the audience clapped after she spoke. But Kennedy continued in the same vein, asking if she supports Hezbollah, an Islamist political party and paramilitary group that’s also a designated terrorist organization. “Again, I find this line of questioning extraordinarily disappointing, senator,” Berry began to respond as Kennedy talked over her, demanding she give a yes or no response. “The answer is I don’t support violence whether it’s Hezbollah, Hamas or any other entity that invokes it,” she finally got out. “So no, sir.” “You can’t bring yourself to say no, can you?” Kennedy replied, even after she said no. The GOP senator pressed on, raising his voice, asking Berry if she supports Iran and talking over her as she tried to answer his questions. Someone started yelling in the audience as Kennedy kept talking. “I think it’s exceptionally disappointing that you’re looking at an Arab American witness before you and saying, ‘You support Hamas,’” Berry said, as she repeatedly rejected his claims that she supports terrorist groups. “You should hide your head in a bag,” Kennedy finally said, drawing loud outcry from some in the audience.

Here’s a video clip of the Republican senator’s offensive questioning:

Off topic but very interesting, regarding the dwindling Russian oil production:

https://www.youtube.com/watch?v=IbmexUrGYR0

From the comments to that video:

“It took a decade or more of Western expertise and money to get the disastrous Soviet legacy oil wells up and running. I worked for a company that was involved in doing this and it was an horrific amount of effort and cash. Then there are refineries which are probably some of the most vulnerable assets to forces that can damage them like explosives, earthquakes and storms. One hit from a drone on a catcracker for example which is filled with catalyst and hydrocarbons at many hundreds of degrees even thousands will cause a huge explosion and damage all the equipment around it. The oil industry is a finely balanced string of assets which must all be in sync. Crude must by moved to tanks and shipment which must go somewhere to be offloaded which must by continually consumed in a refinery whose products must go to storage and be shipped on to consumers. If any part of this chain shuts down the entire operation slows and runs inefficiently and might have to shut down altogether. This is a huge problem for oil wells in a cold climate which then freeze and gum up and may never pump again. Ukraine is hitting Russia in its most vulnerable spot and winter is a month or two away.”

Nobody would pay attention to Cochran if he were not “Nobel adjacent” due to his father-in-law Fama. But both Fama and Cochran are financial economists, not macroeconomists. They both pontificate out of their narrow lane of expertise with no more understanding of macroeconomics than a typical lay person.

They both established their ignorance of macroeconomics during the Great Recession when they argued that stimulus spending was useless because government spending subtracted from private investment, and instead would lead to hyperinflation. It was an embarrassing episode which should have forever excluded them from being taken seriously on macroeconomics.

Well Grumpy claims he is a macroeconomist and would have you read papers like these:

“Long term debt and optimal policy in the fiscal theory of the price level” Econometrica (2001).

“Permanent and Transitory Components of GNP and Stock Prices”, Quarterly Journal of Economics (February 1994).

“The Sensitivity of Tests of the Intertemporal Allocation of Consumption to Near-Rational Alternatives” American Economic Review (June 1989).

Maybe there are more but these are the 3 that come to mind. And none of them are Nobel Prize winning worthy. And your last point is spot on.