There was a noisy minority of analysts thinking we were in, or imminently in, recession (see a list here). It’ll be interesting to see how those views are revised. However, as I noted, while the data was not supportive of being in a recession as of October, three possibilities could reconcile observations with such views: (1) the model is wrong, (2) the recession is here, but we don’t know it, or (3) the recession is still to come.

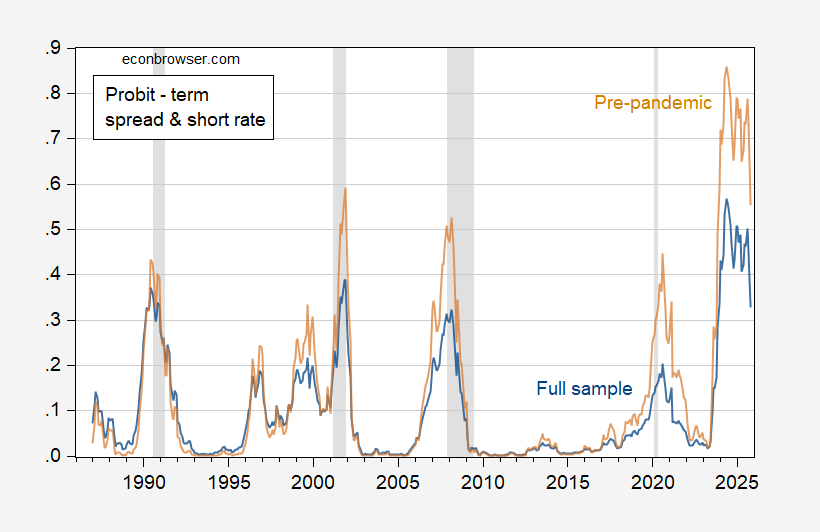

For instance, here’s the probit model predictions from a standard term spread plus short rate 12-month ahead model, estimated both 1986M01-2023M10 (so assumes no recession occurred as of October 2024) and 1986M01-2018M12 (the latter means it omits the 2020 pandemic recession).

Figure 1: Estimated probability of recession 12 months ahead using 10yr-3mo term spread and 3mo rate, estimated over entire 1986-2023M10 sample (blue), over restricted 1986-2018 sample (tan). NBER peak-to-trough recession dates shaded gray. Source: NBER and author’s calculations.

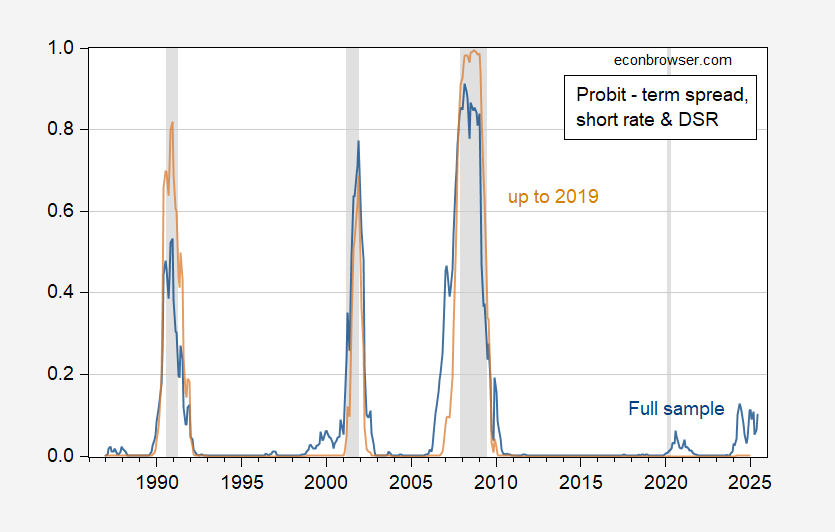

Going by these estimated recession probabilities, the probability of being in a recession in January 2025 is 79% using the entire sample. Using a pre-pandemic sample, it’s 50%. However, as noted in Chinn and Ferrara (2024), this simple specification is dominated in terms of pseuo-R2 and AUROCs by specifications including foreign term spreads and debt-service ratios. Augmenting the term spread & short rate specification with debt service ratio (and using real-time debt-service ratios) yields the following graph.

Figure 2: Estimated probability of recession 12 months ahead using 10yr-3mo term spread, 3mo rate, and debt-service ratio, estimated over entire 1986-2023M10 sample (blue), over restricted 1986-2018 sample using relevant vintage of debt-service ratio (tan). NBER peak-to-trough recession dates shaded gray. Source: NBER and author’s calculations.

The pseudo-R2 for the term spread plus short rate is 0.21, while that for the debt-service augmented specification is 0.56 (full sample estimates).

The pre-pandemic estimates indicate zero probability of recession up to December 2024, while a full sample estimate yields 11% probability in January 2025. Adding in a foreign term spread (a la Ahmed and Chinn (2024)) pushes up that probability to 23%.

If the correct model is the DSR-augmented specification, then a recession in the next year is not foreseen by the markets. On the other hand, if something unexpected occurs between now and 12 months from now (e.g., pandemic, war), then the outcome might be very different from the market’s expectation.

Addendum: 5pm CT

Or…one could see what the betting markets are saying about two consecutive quarters of negative GDP growth in 2025 (presumably using advance release for the 2nd consecutive quarter…)

Source: Kalshi, 9 Nov 24, 5pm CT.

Polymarket uses the NBER BCDC call as a payout criterion.

Question (not being snarky): at what point would you say that option #3 is no longer valid? E.g., if a recession begins 3 years from now, is the model still valid? I certainly would think not. So what do you think is a/the expiration date on option #3?

New Deal democrat: The probit regressions are for 12 months ahead. If the recession doesn’t show up in that time frame (12 months plus minus 6) when the estimated recession probability > 0.5, then I rate option 3 as expired.