Rates are down, but not as far down as in mid-2024.

Figure 1: Instantaneous inflation for headline CPI (blue), core CPI (brown), per Eeckhout (2023), T=12, a=4. Source: BLS via FRED, and author’s calculations.

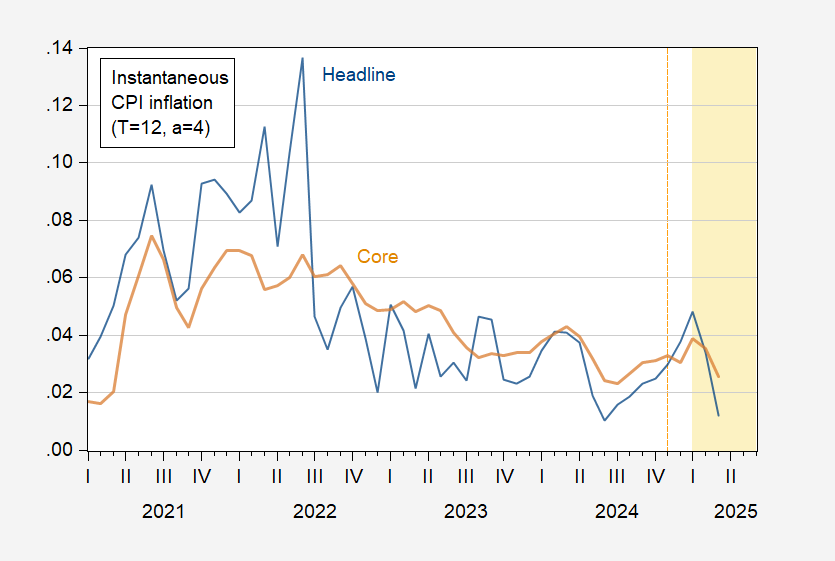

Rates are down, but not as far down as in mid-2024.

Figure 1: Instantaneous inflation for headline CPI (blue), core CPI (brown), per Eeckhout (2023), T=12, a=4. Source: BLS via FRED, and author’s calculations.

One thing which made a big contribution to measured CPI and PPI inflation during the Covid supply shock was used vehicle prices. The same thing sometimes happens around auto-sector labor strikes. When new vehicles are scarce, used vehicles are scarce. When new car prices rise, used vehicle prices rise. Used prices are sometimes more volatile than new. New vehicles count for 4.4% of CPI, used for 2.4%.

In March, used vehicle prices fell. We have maybe two, at the outside three months worth of auto and parts imports inside the tariff wall. If both new and used vehicle prices don’t add to inflation in April, even with 2-3 months supply in hand, I’ll eat my hat.

I think your hat will be pretty safe, although I think there will be some counterbalancing effects from reduced consumer expenditures as imported stuff gets more expensive and reduced goods diversity induces purchasing delays. General retailers are probably sitting on less inventory than auto sellers, and once it’s sold, how much stock will they try to order?

Will eventually be entering deflationary hell or inflationary hell?

I baked a whole wheat hat, just in case.

Here’s Krugman on reading market inflation signals, among other things:

https://paulkrugman.substack.com/p/the-cost-of-chaos-this-is-getting

Krugman isn’t a finance market professional, but he has been paying attention for a long time, and he’s good withmath. Here’s his take on why TIPS give bad inflation signals right now:

“When investors sell off bonds, they drive their price down, which means that they push their yield up. Why does this cause the breakeven rate to fall? Because the market for (inflation) indexed bonds is relatively small and thin, so the rush to sell has a bigger effect in depressing prices and raising interest rates for index bonds than for ordinary bonds.”

You should trust Krugman, but not my recommendation that you trust him. He agrees with me, so I recommend him, and what do I know?

If the inflation premium estimate derived from TIPS is wrong, then term premium estimates are also wrong, because GIGO applies to both.

Food at home rose +0.5%SAMM. I see the beginnings of Tariff effects here.

Regards

Cliff

Can margin calls increase recession odds? Probably. Sorry, but I can’t help myself.

Y’all know that the “basis trade” is a big part of what’s happening with the Treasury market over the past week. When Treasury notes (cash) and Treasury futures move sharply, the basis trade can be blown apart by margin calls.

The basis trade makes (or loses) money due to small differences in pricing between cash and futures, and small differences make for small profits. The way you make big profits is to do the trade many times – through leverage. Many leveraged trades, especially “directional” (price up or down) trades, are leveraged at a small multiple of the collateral value of the underlying security. That way, the lender has a chance to make a margin call before the trade is worth less than the loan.

Basis trades, because they are not “directional”, don’t lose value just because prices move. Only if the price difference moves the wrong way do they lose value. As a result, lenders allow much higher leverage, maybe 100x. Hedge funds, because they make so little on each pair of securities, need high leverage to make much money.

What’s the point of all this? Hedge funds have become big, big, big holders of Treasuries. That’s how they can do so much damage when they face margin calls. Anybody remember Long Term Capital Management? Look it up. This has all happened before. LTCM, the housing crash and Covid all caused basis trades to blow up.

Banks were once the big liquidity providers in the Treasury market, along with insurance companies and pension funds. They still are, but less so now that hedge funds are involved. Importantly, banks are shielded from some of the pain of Treasury market losses because for regulatory purposes, Treasuries are considered safe – Tier One assets. On the assumption Treasuroes are held to maturity, they’ll pay a dollar for a dollar, so all is well.

However, regulatory certainty isn’t everything. Balance sheets are balance sheets, and banks hold big piles of Treasuries. If long-end losses persist, say because inflation expectations turn out to be high, then banks’ balance sheets will be smaller in reality, even if not for regulatory purposes. That means tighter bank lending. Tighter bank lending typically means weaker economic growth. Small and medium-sized firms would be most damaged by weaker bank lending.

So when, for instance, tariffs raise inflation expectations, that can impair bank lending and economic growth, not just because of higher rates, but also because of stingier lending standards. Market volatility, to the extent it makes banks more cautious, can do the same. So maybe scaring the crap out of financial market investors with tariffs is a bad idea.

Heard somebody make the point that basis trades are done with 2 year and not 10 year treasuries. Haven’t looked up 2 year action yet. However, the 10 year yield continues to rise in this chaotic market. Even with a slight market increase, still does not seem right.

I’m no expert, but my understanding is that the choice of security has to do with pricing anomalies. If ten-year cash an figures are misaligned, that’s where he trade happens.

I’m not the only one who sees Liz Trust as a model for the felon-in-chief’s policy vanity:

https://www.nytimes.com/2025/04/09/business/economy/us-bonds-trump-truss-treasury-yield.html

Imagine, if you will, that foreign market participants had not expected the insurrectionist-in-chief to risk the health of the U.S. economy and the welfare of its citizens as he did on “Liberation Day (sic)”. They might now want to reevaluate their assessment of the insurrectionist. His actions have been more reckless, more extreme and more immediately harmful that market participants had expected.

Now, imagine that foreign market participants cast their eyes upon Miran’s “Mar-El-Lago accord” document. Miran’s document outlines a plan for default on U.S. obligations on a massive scale. So what action might a rational foreign holder of U.S assets take? Keep in mind that the Heritage Foundation’s “Project 2025” documenr has become the agenda for the insurrectionist administration, and its authors now occupy high office. There is reason to think that Miran, who occupies high office, has also authored part of the insurrectionist’s agenda. So what’s a foreign holder of U.S. assets to do?

How much are we talking about? From the “Preliminary Report on Foreign Holdings of U.S. Securities at End-June 2024”:

“The survey measured the value of foreign holdings of U.S. securities as of June 30, 2024, to be $31,288 billion…”

https://home.treasury.gov/news/press-releases/sb0037

So $31.3 trillion. Outstanding U.S. fixed income securities amount to about $47 trillion. Stock Market capitalization in the $50-$60 trillion range. Money markets about $7 trillion. Call it $110 trillion. Foreign holdings account for something like 28% of U.S. securities.

What would happen if foreign holders began to assign a substantially higher default risk to U.S. assets? Not talking about China using sales of Treasuries as a weapon – that’s a separate issue.

Sell, Mortimer! Sell!

If you are a reader of this blog, your elected representatives very likely aren’t as smart or well-informed as you are. You should educate them.