Jim will have examination of the GDP numbers tomorrow, but here is the picture as of today, in the wake of the international trade figures, industrial production, housing starts, yesterday and today.

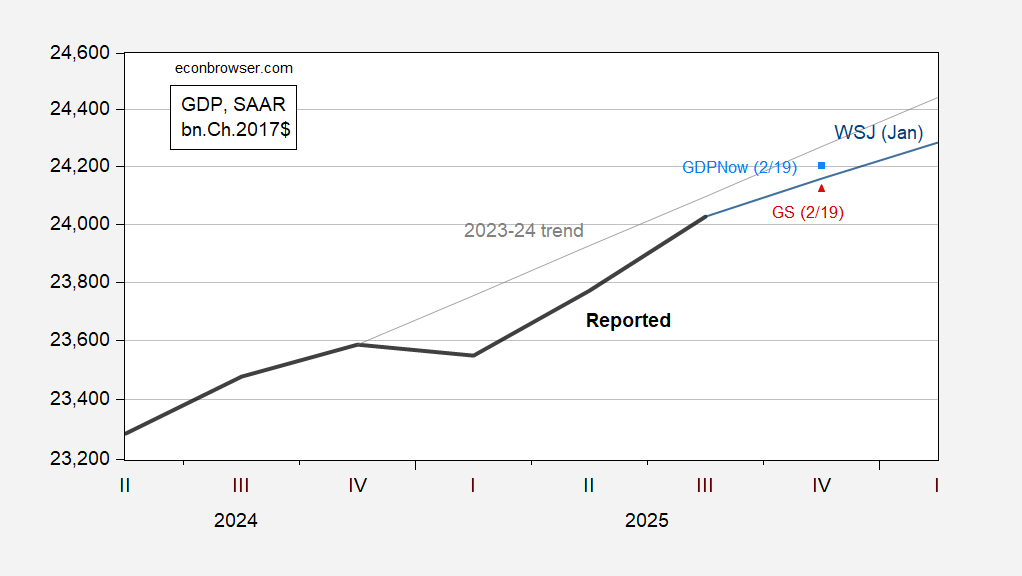

Figure 1: GDP as reported (bold black), GDPNow (sky blue square), Goldman Sachs tracking (red triangle), January WSJ survey mean (blue), and 2023-24 stochastic trend (gray), all in bn.Ch.2017$ SAAR, on log scale. Source: BEA, Atlanta Fed, Goldman Sachs, WSJ January Survey of Economists, and author’s calculations.

Note that there’s a wide divergence in q/q AR growth rates nowcasted: GDPNow is at 3%, while GS is at 1.6%. Even with rapid growth like 3%, we have not re-attained the 2023-24 trend.

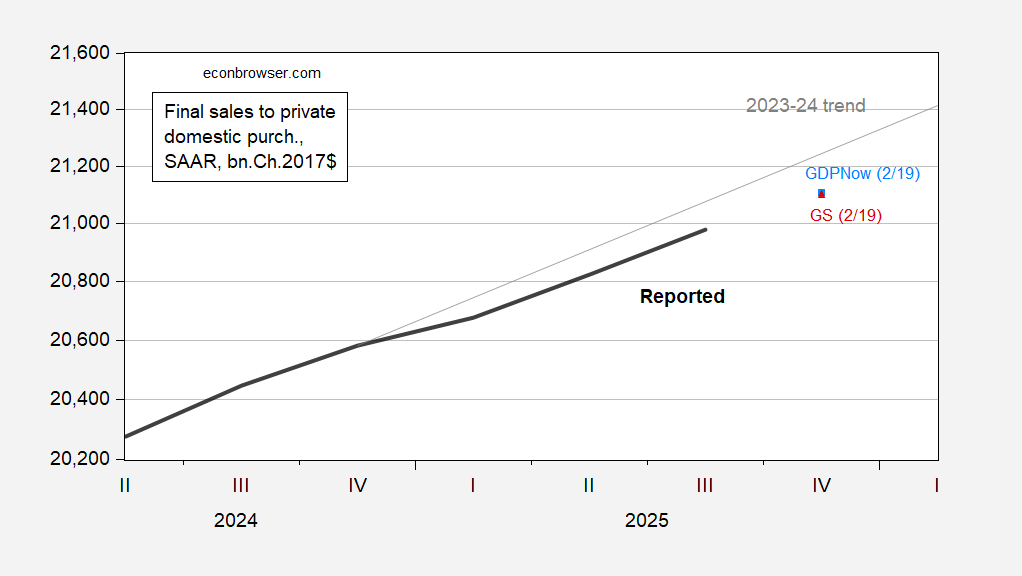

Once one strips out volatile foreign elements (exports, imports) and inventories, one gets more of a consensus. Here’s a plot of “Core GDP”, which is final sales ex-imports, imports and government spending.

Figure 2: Final sales to private domestic purchasers as reported (bold black), GDPNow (sky blue square), Goldman Sachs tracking (red triangle), and 2023-24 stochastic trend (gray), all in bn.Ch.2017$ SAAR, on log scale. Source: BEA, Atlanta Fed, Goldman Sachs, and author’s calculations.

From Figure 2, it’s clear that as currently estimated we are not closing in on the 2023-24 trend. To the extent that “Core GDP” proxies for trend aggregate demand, then the economy appears to be on a track that is falling further and further below the 2023-24 trend. That being said, CBO estimates 0.9 percentage point of GDP fiscal stimulus emanating from provisions of the BBB in 2026, so this year might look different.

As to the effect of the Big Bloated Bill, here’s the Hutchins Center on the effects of fiscal policy on real GDP in 2026:

“Fiscal policy is projected to boost GDP growth by about 3 percentage points in the first quarter of 2026 as delayed federal spending resumes and the OBBBA tax cuts boost spending. For the remainder of 2026, as the post-shutdown spending boost gradually dissipates, fiscal policy turns restrictive.”

The shutdown and it spending rebound get top billing, ahead of the Big Bloated Bill, and for good reason. The largest addition to the deficit was from extending “temporary” tax cuts. That’s a change in the fiscal balance “under current law” but not so much in reality. There is a good bit of hope that large tax refunds resulting from the Bloated Bill will boost spending in March, April and May, but that depends on whether tax payers anticipated a tax increase in tax withholding – an educated guess.

Note that Hutchins estimates do not employ fiscal multipliers. In this case, that’s probably good, since tax cuts go mostly to the rich, who spend less as a share of disposable income than do others.

One more thing. Tomorrow’s Q4 data will give us a look at the impact ofthe shutdown on Q4 GDP, so a way of assessing the further likely impact of the reopening on Q1 GDP.

The shutdown was a drag on growth, a 1.15% drag, and made forecasting tough. That sets up a rebound in the current quarter.

Note that real dispossble personal income rose just 0.1% in Q4, after no growth in Q3. That’s the slowest 2-quarter performance since H1 2022. Part of the problem is that inflation picked up in Q4 relative to the 2025 average. I glation in 2025 as a whole was up slightly from 2025. Real DPI is not a reliable predictor of recession, but is part of the affordability problem.

Press reports indicate the Supreme Court will rule today on the felon-in-chief’s national security tariffs. Looks like the headline decision is that the tariffs are unconstitutional. Details matter, and I don’t see and press on the details.

In court filings, the felon-in-chief administration has said that all tariffs found to have been collected illegally will be refunded, with interest. (Find link here https://www.usatoday.com/story/news/politics/2026/02/20/tariffs-trump-supreme-court-refunds-trade-deals/88103891007/)

Bessent has said refunds may take up to a year. This adds another $2.5 trillion to the 10-year deficit projection. Maybe we need a tax hike?

So, within the space of two days, the felon-in-chief’s immigration and trade policies have been largely overturned by the courts. As a result of the tariff decision, the felon’s already giant budget deficit has been made $2.5 trillion larger over the next decade. As a cherry on top, New Mexico’s Attorney General has requested the complete Epstein files, unredacted.

Under the circumstances, seems like we’ll be bombing Iran soon, simply to draw attention from the felon’s many failures. The felon himself says the timeline is the next ten days.