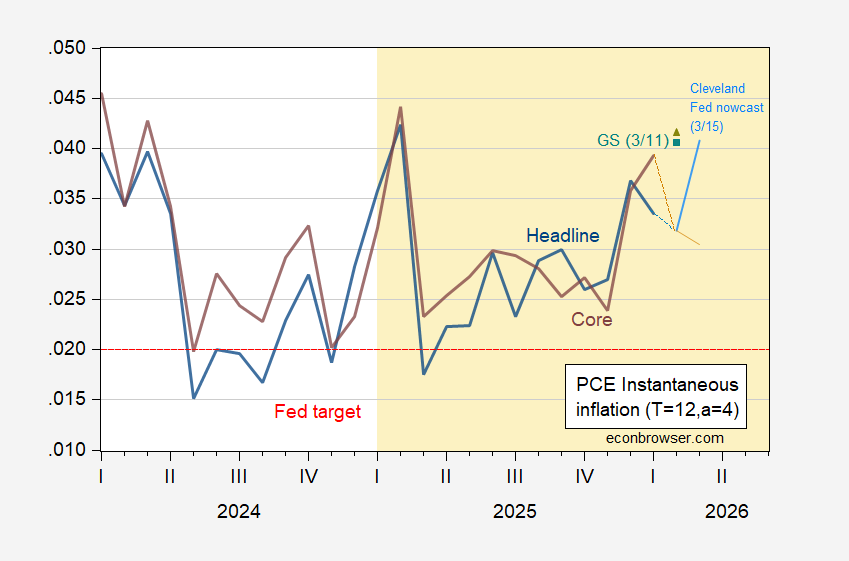

Goldman Sachs tracking ticks higher core PCE inflation for February. The Cleveland Fed’s core nowcast imply lower instantaneous inflation for February and March.

Figure 1: Instantaneous inflation (T=12, a=4, per Eeckhout (2023)) for PCE deflator (blue), implied from Cleveland Fed (light blue), implied from Goldman Sachs (teal square), for core PCE deflator (brown), implied from Cleveland Fed (light brown), implied from Goldman Sachs (chartreuse triangle). Source: BEA, Cleveland Fed accessed 3/15, and Goldman Sachs (3/11), and author’s calculations.

Note that the Cleveland Fed nowcast relies upon a limited set of time series (CPI, PCE, oil and gasoline prices for headline nowcasts) using a time series model, while Goldman Sachs tracking incorporates judgmental input.

With Isramerica stepping up bombing, assassinations and threatening a Marine invasion, as well as Iran’s incentive to extract reprisal, the probability of a long term Strait of Hormuz shutdown is very likely. Check out:

https://fredblog.stlouisfed.org/2020/04/oil-prices-and-expected-inflation/

….for the likely effect of longer term inflation effects from higher oil prices…. The analysis implies a 2.5 to 3% inflation bump 5 years after the higher price event.

Yep. Goid catch.

Except, so far, it’s not working this time:

https://www.willsmithmusic.com/songs-2/#/202-2

The guess in major markets, so far, seems to be that the war will end quickly, and things will go back to normal. Not sure why.