From notes for PA854 (before AD-AS chapter), to be discussed tomorrow:

Assume the price level is sticky in the short run with respect to aggregate demand, but responds quickly to cost-push shocks:

![]()

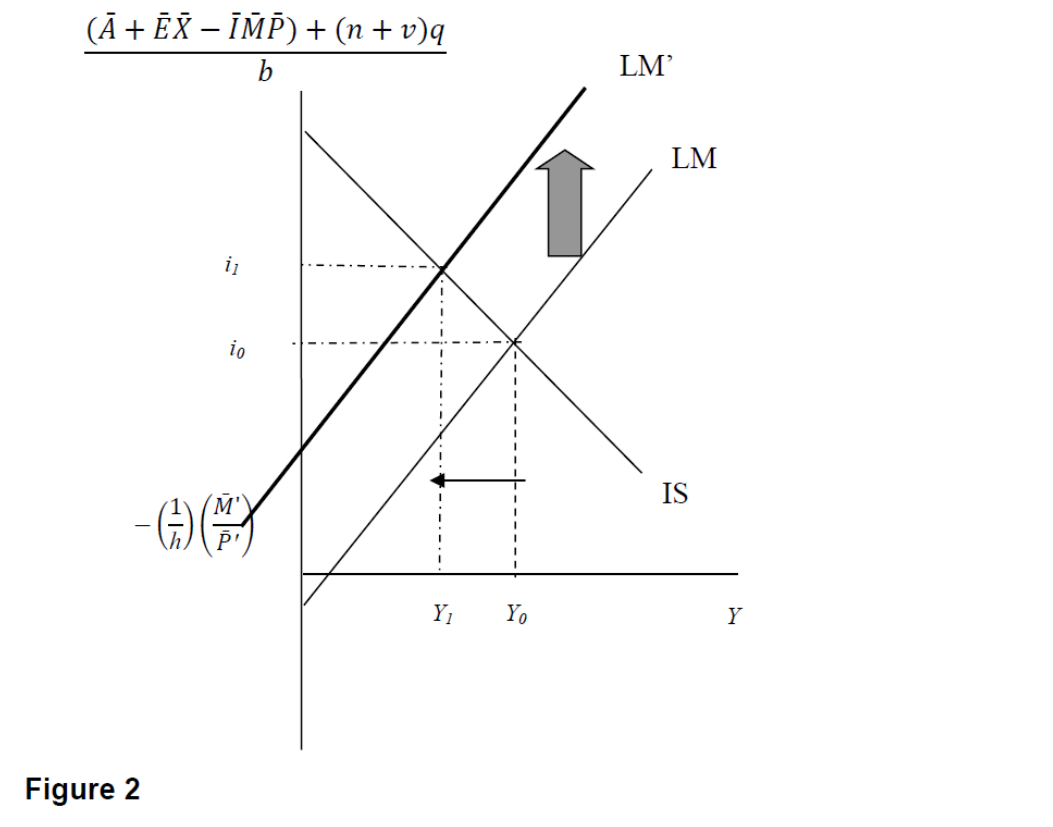

The elevated oil price (see this post) then induces a leftward shift in the LM curve (gray arrow), raising borrowing costs.

Output declines from Y0 to Y1, as interest rates rise. In reality, policy rates are likely to be set higher than they otherwise would have been.

Note that this is an old fashioned interpretation of central bank as targeting the money supply. One could reinterpret as an interest rate target, where the interest rate is targeted, but reacts positively to the price level.

An obvious question is whether the IS curve should shift out in response to an increase in government (defense) expenditures. The answer depends on whether production can be ramped up quickly to replace expended munitions (probably not, as we’re at capacity), or more importantly whether the war entails “boots on the ground”. Current betting on Polymarket indicates 42% probability by year’s end. For the moment, I assume no ground forces in Iraq for an extended period.

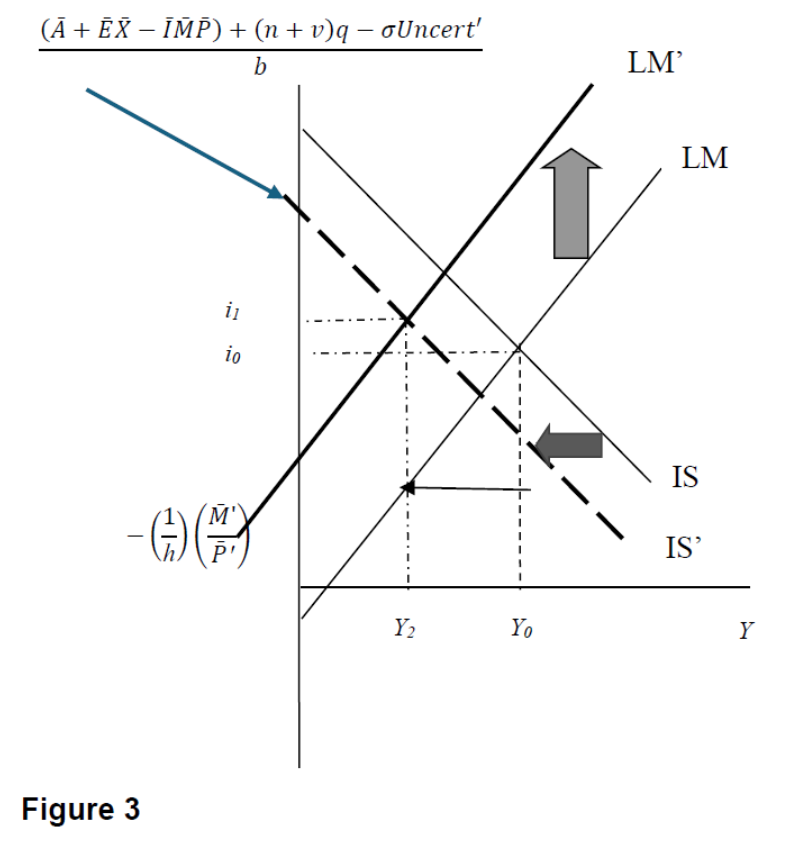

We’re in a period of great uncertainty with respect to the conduct of economic policy writ broadly, as well as geopolitical risk (see here). How can we interpret this in a simple IS-LM model. We can’t unless we augment the model. The obvious place is investment; relying on empirical work (e.g., Baker, Bloom and Davis), restate the investment equation as:

![]()

Elevated uncertainty (see here) then implies slowing investment, shifting in the IS curve (dark gray arrow).

Output then falls to Y2.

“The answer depends on whether production can be ramped up quickly to replace expended munitions (probably not, as we’re at capacity)…”

At capacity in the military-industrial sector, or the economy as a whole? The first implies that we can’t quickly boost real aggregate output by making more things that go boom. The second implies that we can’t quickly make more things. I guess the IS-LM presentation refers to the second case.

Here’s the prime age employment-to-population ratio:

https://fred.stlouisfed.org/series/lns12300060

So yeah, it kinda looks like we can’t quickly make more things. A shift toward making more things that go boom would necessarily mean making less other stuff. Like Russia duriing the Ukraine fiasco, but in a less dramatic way.

Axios has counted up the countries the Mad King has attacked during his second term in office:

https://www.axios.com/2026/03/02/trump-iran-war-military-strikes-maga

The list us Iran, Iraq, Nigeria, Somalia, Syria, Venezuela and Yemen, seven in total. That’s more than any other modern president. There’s a reasonable chance we’ll add Cuba to the list, and there are plenty more countries in Africa to bomb, if we don’t run out of bombs before we get to them. I’m not an expert in this stuff, but my impression is that bombardment alone almost never achieves important military goals. I do wonder what the Taylor-Greene/Paul wing of the MAGA crowd is going to think about this “bombiest president ever” story.

Iran is the most militarily capable of the countries the Mad King has attacked. There are suggestions in the press that air defense munitions are running low for the U.S. and Israel, as well as for other countries within striking distance for Iran. In an artillery duel, the first one to run out loses.

Iran has been through something similar both in the 12-day war with Israel last June and in the War of the Cities with Iraq in the mid-1980s. In the 1980s, they kept fighting under bombardment of their cities for over four years. Casualty tallies for the Iran/Iraq war vary widely, with high-end estimates for Iran at 750,000. I’d like to hear how we think a few weeks of bombing is going to “improve” Iran’s behavior.

It would be classic Mad King to not have a plan B in case we run out of air defense munition before Iran run out of airborne munition. Competence matters – a lot.