Remember?

“Borrowing and spending by the public sector will crowd out investment and growth in the private sector.” Paul Ryan, “Path to Prosperity” (April 2012).

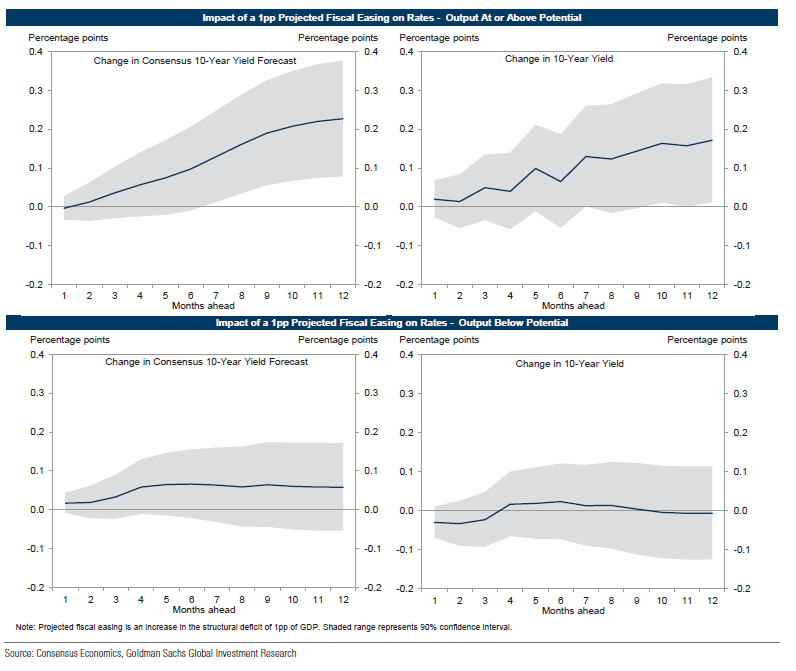

The reasons why interest rates did not rise appreciably in the wake of the American Recovery and Reinvestment Act included the accommodative Fed policy (see this post for graphical analysis augmented by a very little algebra), and the slack in the economy. Neither of these conditions hold in 2018, so one might think that elevated interest rates due to the massive increase in Federal government deficits and debt will now show up. A recent Goldman Sachs report (Hatzius et al, May 12, 2018) makes this point, as shown in the impulse response functions (IRFs) associated with a 1 percentage point of GDP increase in the structural budget deficit, displayed for below versus at or above potential GDP.

Source: Hatzius et al., “Budget Deficits and Interest Rates,” US Economic Analyst, Goldman Sachs Economic Research, May 12, 2018.

Notice that consensus 10 year yields and actual 10 year yields rise statistically significantly when the fiscal easing (equal to 1 percentage point of GDP) occurs with a zero or positive output gap. No such significant effect is found when stimulus occurs with a negative output gap.

Using other methodologies (including the Laubach approach incorporating expectations of future debt, see Chinn and Frankel (2005) for example), Hatzius and coauthors find a statistically significant positive impact on yields of additional deficits.

So, just like fiscal multipliers might very well exhibit state-dependency, the impact of debt and deficits might be asymmetric.

I so love it when you call that b*stard Ryan out. What really aggravates me about Ryan, was people were always trying to make him out to be a “technocrat” when he was nothing of the kind. He was a light-weight, shallow piece of crap. One of the cheerleaders for Ryan was David Brooks, who himself is a damned idiot and wouldn’t know the difference anyway. I’m glad David Brooks has joined the #MeToo movement though. Good for him. No word yet on if Brooks plans on filing charges.

https://www.youtube.com/watch?v=1WWWIYeS4Q4

Wouldn’t it be fascinating if you could actually “magically” know what percent of Senators and then what percent of House Reps actually know and understand the IS-LM model?? How many of them out and out don’t know or even what % know and just ignore it because it’s not politically pragmatic. I’d pay a minor fee to get the real stats on that one. I wager the ones like Rand Paul who spend the most amount of time insincerely pounding the table are the same ones who couldn’t jot the basic idea out on a napkin.

Walter Heller used to draw diagrams for President Kennedy. But when LBJ became President, he wanted one page summaries. It seems Treasury always wrote 3 to 4 page memos which the Chief of Staff would not give LBJ. No the Chief of Staff would walk over to the CEA and ask Heller to rewrite the memo so no staple was required. Heller was an excellent writer so he could do so but it sort of made him angry. Until he realized the power that this gave the CEA – all economic communications to the President first had to get past his desk!

“Borrowing and spending by the public sector will crowd out investment and growth in the private sector.” Notice how Ryan phrases this. Tax cuts for the rich as SOOO different. Well not really but then Ryan does not peddle honesty – does he? We had this experiment under St. Reagan. Government spending as a share of GDP did not go up. Yes defense spending rose but then Reagan managed to squeeze reductions in government spending from not just transfer payments but also infrastructure investment. We did see that massive 1981 tax cut which led to more consumption spending on Rodeo Drive. And yes real interest rate soared not only crowding out private investment but also net exports. But the Paul Ryan crowd tries to deny this reality at every turn.

The Wikipedia entry for Paul Ryan describes his college education as follows:

Ryan has a bachelor’s degree in economics and political science from Miami University in Oxford, Ohio,[30] where he became interested in the writings of Friedrich Hayek, Ludwig von Mises, and Milton Friedman.[21] He often visited the office of libertarian professor Richard Hart to discuss the theories of these economists and of Ayn Rand.

https://en.wikipedia.org/wiki/Paul_Ryan

I’d like to see the econ courses he took in college. I’d be willing to bet dollars to donuts that he took a bunch of “Survey of …” classes that sort of skimmed the history of economic thought. It’s the kind of stuff that people more interested in political economy than economics end up taking. In other words, no rigorous math and no econometrics. It’s the kind of curriculum you might expect a sociology major to take when testing the waters in econ land.

If Milton Friedman read the BS that Paul Ryan puts out he would disown any association with such an ignorant person.

BTW – Ryan’s math skills are amazing. He is the only one who has figured out how to keep Federal purchases at 3.5% of GDP while having Federal defense purchases stay at 4% of GDP. Plus he managed to run a sub 3 hour marathon whereas the clock said 4 hours and 2 minutes. Truly impressive!

Menzie This analysis is based on changes to the structural deficit. For the benefit of some of our friends here (you can guess the usual suspects), you might have to explain the difference between structural and cyclical deficits because it’s pretty clear to me that not everyone understands the difference. They seem to think it’s some kind of left-wing Keynesian mumbo-jumbo.

The two upper graphs (when above potential) don’t look to be flattening out, even at the 12 month ahead period; i.e., they’re explosive. That’s unexpected.

E. Cary Brown wrote the seminal paper on this which was published in the American Economic Review back in 1954. I presume the Usual Suspects have not read that either. Anyone who has not read Brown’s paper should be required to do so before making another comment on fiscal policy.

Cutting taxes and spending will help offset rising, although low, interest rates, to spur private consumption and investment. Entitlement spending, in particular, can be cut to promote work and finally close the output gap. More defense spending will boost R&D spending and spin-offs, along with strengthening national security and deterring aggression. Incentives can be created to benefit both the economy and individuals or families. GDP and therefore tax revenue will increase. And, government debt can be reduced as a percent of GDP.

You have contradicted yourself faster than anyone in the history of time! First you advocate cutting government spending and then you advocate increasing government (defense) spending. And if this were not the most amazing flip flopping in the history of time – you advocate fiscal stimulus at the same time that you call for reducing government spending.

I wonder if the Nobel Prize is given out for the category of dumbest flip flopping ever. You will win hands down!

Pgl, you certainly have no shortage of dumb and ignorant comments.

It’s possible to reduce entitlement spending more than raise defense spending, for example.

And, some spending and tax cuts have higher multiplier effects.

PeakTrader some spending and tax cuts have higher multiplier effects.

Prove it. Show us the math. Time to put up or shut up.

2slugbaits, I’ve explained the math many times before. When government pays people not to work, e.g. with excessive unemployment benefit extensions or disability payments, guess what? They don’t work. When there’s a consumption boom and huge trade deficits, money needs to be recycled to refund consumers, rather than selfishly spent and squandered by government, to allow the spending to go on. When government requires means testing for benefits, that creates a disincentive to work, etc.. I’ve explained it all in detail many times before. You still don’t get it.

And, I predicted the Obama stimulus would be a failure, including to close the output gap, in early 2009, although it turned out worse than I expected. Robert Barro’s prediction was more accurate:

https://www.wsj.com/articles/SB10001424052748704751304575079260144504040

Robert Barro:

“Consider the expansion of social-safety-net programs, including food stamps, unemployment insurance, Medicaid (prospectively) and housing and mortgage programs. In a study published last month by the National Bureau of Economic Research, University of Chicago economist Casey Mulligan observed that, because these programs were means-tested (falling or ending as income rises), expanding them raised the effective marginal tax rate on labor income.”

https://www.hoover.org/research/why-slow-recovery-no-recovery

PeakStupidity turns to Casey Mulligan??? Excuse us all for falling on the floor laughing!

OK I just read that Hoover Institute babble from Robert Barro. He is one of the dudes that feared that the FED’s QE policies would lead to hyperinflation. That alone should disqualify this washed up New Classical type. But yea we had a strong recovery from the 1982 recession but of course everyone who knows anything knows it was the FED that drove that recovery.

Which of course undermines just about all of PeakStupidity’s incessant intellectual garbage.

“because these programs were means-tested (falling or ending as income rises)”.

Now that I have stopped laughing and got up from the floor, let’s dissect how stupid this Casey Mulligan line is. This could be said about any countercyclical feature of fiscal policy. Only a hack like Mulligan could turn a desirable feature into something that allegedly makes business cycle worse. That Barro did not realize that shows he is washed up. That PeakStupidity highlights this as a critique shows he never under basic Keynesian math. No wonder he refuses to show his arithmetic – it is all wrong!

PeakTrader I didn’t ask you to regurgitate old nostrums. I asked you to prove that spending and tax cuts have higher multiplier effects. I asked you to show us the math. Instead you show us idiotic op-ed pieces from the WSJ. Do you understand what a fiscal multiplier is? It doesn’t sound like it. Now, one more time. Show us the MATH that demonstrates how tax cuts have HIGHER multipliers than spending increases. Don’t just tell us that a tax cut has a positive multiplier because we know that. What you keep claiming is that a tax cut has a HIGHER multiplier than a spending increase. Show us the math. Show us that you can do some real economics. Show us that you’re not just a poser with a lot of time on his hands.

As far as explaining the math in terms of equations, I performed the math successfully in grad school. Many of my grad econ classes were all math – with some of the longest and most detailed equations you can imagine, where instructors used four chalkboards and had to write smaller at the end. I received A’s, A-‘s, and B+’s (below a B was a failing grade). About half the students were math majors and about half econ majors. Some had majors in something else. I noticed, many of the math majors didn’t understand the economics that well, while econ majors had problems performing the math (for example, not knowing a mathematical trick to rearrange an equation for the next step, would stop you on your tracks – my Ph.D math tutor would ask me more questions about economics, which is rich in terminology, than I asked about the math). No one completed a one hour test on time, including the math majors. I was more interested in understanding what I was doing, rather than writing equations as fast as possible, although that’s what I did in class. A lot of students failed to get a minimum B in a core class to graduate, transferred to an easier program, or dropped out. I successfully jumped through the hoops, with the main purpose of understanding the material, which was often condensed, where one page could be expanded to 100 pages, when the terminology is explained and the intermediate mathematical steps are included. Anyway, piecing together a crude general equilibrium model provides a better picture than one detailed partial equilibrium model, although that’s very helpful.

2slugbaits, Robert Barro is a highly rated economist:

https://ideas.repec.org/top/top.person.all.html

And, 2slugbaits, if you want more government spending, and more regulation, then you need faster GDP growth. Haven’t you learned anything from the 2009 “recovery?”

Moreover, 2slugbaits, I’ve stated before, a large tax cut, rather than the small and slow tax cut, was the appropriate response to compensate not only for the steep fall in production in the private sector, but also to strengthen household balance sheets and the banking sector, which weakened substantially.

The weakness was the result of overconsumption, in the 2000s, where there was up to $800 billion a year trade deficits – dollars flowed to foreigners and foreigners bought U.S. Treasury bonds, and homeowners used their homes as ATMs. Households would’ve used a big tax cut to pay down or pay off debt, which would strengthen households and banks, and raised discretionary income to raise production in the private sector. That would’ve closed the output gap faster than the (temporary) government spending and squandering, which was less effective to address the problem.

When you’re behind on car payments, paving a new road doesn’t help you much, although it may look good on paper.

A $5,000 middle class tax cut, for example, with a boost in unemployment benefits, rather than extensions, would’ve allowed households to catch-up on bills, pay off a credit card or car loan, and raise monthly discretionary income. It would’ve also strengthened the banking industry.

PeakTrader You still haven’t answered the question. I asked you to prove that tax cuts have a higher fiscal multiplier than spending increases for a given change in the deficit. You’ve had multiple opportunities to answer the question and you keep ducking the issue. It’s not exactly difficult math to show that spending multipliers are greater than tax cut multipliers, so I frankly don’t believe your claims about your math skills. Just another keyboard jockey in St. Petersburg. It’s no wonder no one on this blog takes you seriously.

Pgl, that wasn’t my response to 2slugbaits ridiculous statement. I just happened to post it before 2slugbaits response showed up. It’s easier to recall the many ideas that fell out of the equations than recalling all the math details, when you haven’t used much math in a while. I don’t recall what textbooks I used, but they were standard. I recall, the top schools my professors got their econ Ph.Ds from. Just because someone has a limited understanding of economics doesn’t mean the ideas are wrong.

2slugbaits, along with your false assumptions and simple economics, you want a nonsensical answer to an assumption that every recession is the same. You haven’t come close to explaining any economics, just reciting some econ 101 sometimes.

https://www.economist.com/node/14505361

PeakTrader Sorry dude, but your economist.com article still doesn’t answer the question I asked. The article simply points out that the econometrically measured multiplier can vary because consumers and the Fed might have different reaction functions. All that’s true, but it doesn’t have squat to do with what I asked you. Here’s the question in its simplest form: Which action will have the highest fiscal multiplier, ceteris paribus, a $1T spending increase or a $1T tax cut? You keep insisting that the latter will have a greater multiplier. Now prove it.

2slugbaits, you need proof government spending that creates disincentives to work or work less lowers GDP growth?

And, you need proof high household debt without powerful and immediate relief lowers GDP growth?

I correctly predicted the Obama stimulus would fall well below expectations.

Of course, not all government spending and all tax cuts are the same.

Dude – calling out your idiocy is child’s play. And your rebuttal is always the same. Telling us facts and economic theory represents dumb and ignorant comments. By now even your own dog is laughing at you.

I’ll grant that there may be different multiplier effects but you have the sign wrong. Infrastructure investment has a higher multiplier effect but it is still positive. FYI!

This is Peaky’s response to 2slug?

“As far as explaining the math in terms of equations, I performed the math successfully in grad school.”

I doubt it as Peaky could not answer Menzie’s question about which economic texts he used. Besides some people get pass their exams and then forget everything they ever learned. Based on Peaky’s incessant and incoherent rants where he ducks the real question – he clearly is one of these people. So he just continues with his some old rants over and over again.

“It’s easier to recall the many ideas that fell out of the equations than recalling all the math details, when you haven’t used much math in a while. I don’t recall what textbooks I used, but they were standard.”

Please stop embarrassing yourself with this babble. The many ideas you express here appear to be cut pasted from Fox & Friends. None of those clowns received a Noble Prize. None of them have ever published a single academic paper. For good reason – they are babbling idiots. Alas – you babble their stupidity. Please stop as it really a waste of everyone’s time.

Peak,

The US is spending more on war per year [since 2004] than anytime since WW II, inflation adjusted dollars. The variable costs for wars to throw out Assad cost more than the next three big war spenders spend in total. ‘Sequestration’ meant the pentagon trough was less of a growth industry. What are you getting?

The new authorization bill is bat sh!t crazy splurging on a lot (too much current operations and readiness to go to fiction wars crowding better profits on readiness for future fiction wars) to keep unreliable, poor maintenance stuff running and “procurement”, around $147B for 2019 which is not enough per AEI and does not go long considering $143M a copy F-35 which flies like an A-7 ‘lead sled’, or $13B aircraft carriers to haul around F-35’s and launch them on unreliable catapults…

While AEI/Heritage, [less than 7% of GDP for war means the Taliban win] want more procurement spending and GAO notes the big stuff is bought not knowing how it works] wants more procurement spending!!

Note:: the independent testers do not start ‘real world’ testing on F-35 until 2019 when nearly 500 are in the inventory or ordered. And we know it won’t be repaired because they cannot get its logistics software to work……

The answer is leave Syria and Kim alone and look to the US.

See

https://www.defensenews.com/congress/2018/05/17/trump-budget-wont-rebuild-the-military-and-thats-dangerous-think-tank-says/

Refers to AEI sales pitch for more trough filling.

“The US is spending more on war per year [since 2004] than anytime since WW II, inflation adjusted dollars.”

I just went to http://www.bea.gov Table 1.1.6. Real Gross Domestic Product, Chained Dollars line 24 for inflation adjusted defense purchases, which were $652.7 billion (2009$) in 2004. This spending rose to $813.5 billion by 2010. Yes as we unwound the 2003 mistake, defense spending fell $667 billion in real terms by 2016. So you are absolutely correct.

But do not forget – PeakyStupidity gets paid by the word to spread lies for his leader – Donald Trump.

Our Treasury Secretary should be prosecuted for obstruction of justice:

https://talkingpointsmemo.com/muckraker/democrats-crew-ask-mnuchin-recusal-cohen-sara

“For months, good-government groups and some Democratic lawmakers have been calling on Treasury Secretary Steve Mnuchin to recuse himself from matters related to the federal investigation into Russian election meddling. Mnuchin’s role as finance chair of Donald Trump’s 2016 campaign means he can’t impartially oversee a probe that delves into Trump associates’ financial affairs, they have argued. Those calls took on a new urgency this week when The New Yorker revealed that Suspicious Activity Reports (SARs) filed on long-time Trump fixer Michael Cohen were removed from a database kept by the Treasury Department’s Financial Crimes Enforcement Network (FinCEN) division.”

Wait – there is more:

“In December, progressive groups noted in their own letter to Treasury’s Inspector General that Mnuchin had replaced the director of FinCEN with his own choice, just days after former Trump campaign chair Paul Manafort was indicted for money laundering and a host of other financial crimes.”

@ PeakIgnorance

PeakIgnorance, you’re getting confused on time again, your annual holiday greetings with Tonto and Tarzan aren’t until around early December. You can practice in the mirror though.

https://www.nbc.com/saturday-night-live/video/seasons-greetings/2868079

Since we’re borrowing to finance tax cuts, it must be time to cut Social Security, Medicare, and Medicaid. Problem?

The crowding out relates to the financing of the deficit which means all of the deficit. Thus when times are reasonable people will buy government bonds over corporate bonds thus the ‘crowding’ out.

Interest rates are thus higher than they should be however from the evidence from both the Reagan and Bush Jnr years the impact on interest rates are not as great as perhaps they were in the past.

why some Republicans and their supporters only worry about crowding out when the economy is in recession and not when the economy is okay is very strange however Hayek thought it occurred absurdly in a depression.

What is clear in chaos land it that should be trying to reduce the structural deficit not increase it. This would boost growth

Does PeakIgnorance even read his own links? 2slug has been suggesting that the fiscal multiplier for government purchases (building bridges for example) is larger than the multiplier from giving someone a tax cut. So PeakIgnorance googles and finds this 2009 discussion:

https://www.economist.com/node/14505361

A key excerpt:

“The multiplier is also likely to vary according to the type of fiscal action. Government spending on building a bridge may have a bigger multiplier than a tax cut if consumers save a portion of their tax windfall. A tax cut targeted at poorer people may have a bigger impact on spending than one for the affluent, since poorer folk tend to spend a higher share of their income.”

What 2slug said. This is game, set, and match to 2slug!

Another odd excerpt:

“An alternative assessment by John Cogan, Tobias Cwik, John Taylor and Volker Wieland uses models in which interest rates and taxes rise more quickly in response to higher public borrowing. Their multipliers are much smaller.”

They forecasted that interest rates would rise “more quickly”. Seriously? We had a decade of near zero interest rates. I guess their model found its way to the dust bin in very short order.