Coming down for June, according to the University of Michigan survey of consumers.

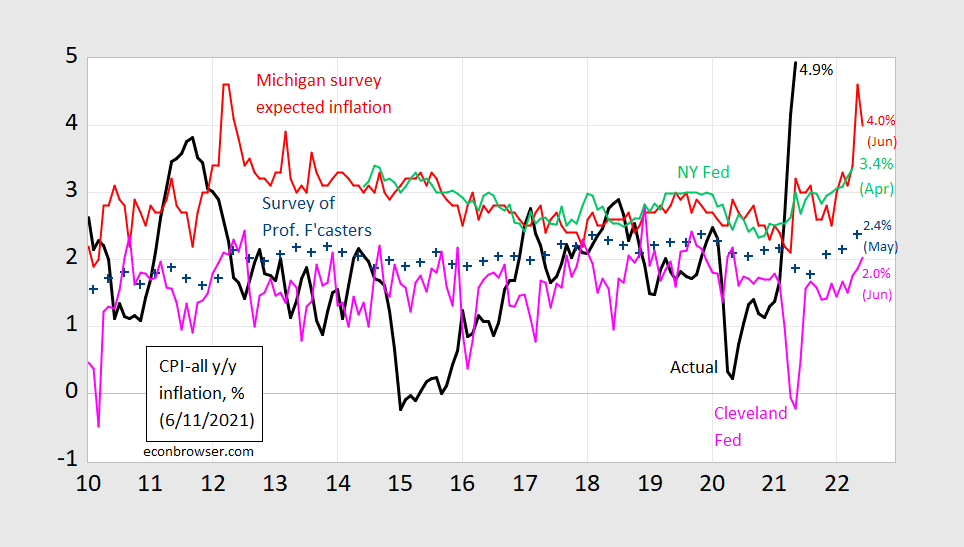

Figure 1: CPI inflation year-on-year (black), median expected from Survey of Professional Forecasters (blue +), median expected from Michigan Survey of Consumers (red), median from NY Fed Survey of Consumer Expectations (light green), forecast from Cleveland Fed (pink). Source: BLS, University of Michigan via FRED, Reuters, Philadelphia Fed Survey of Professional Forecasters, NY Fed, and Cleveland Fed.

The household survey measures are typically higher than those based on surveys of economists. Hence, looking at changes is perhaps more informative about how inflation sentiments have changed.

From November to June, the Michigan (survey) measure has risen 1.2 percentage points, while the Cleveland Fed (hybrid market/survey) measure has risen only 0.6 percentage points.

The gap between the Michigan measure and the SPF has widened to its largest since May/June 2008 surveys — 2.2 percentage points (for May, the last survey for the SPF).

Doing the sloppy/lazy “eyeball test” (my personal favorite way of doing these things, half-joke). Uhm…… It looks like the Cleveland number gets it slightly better than “SPF”. Still I can’t be sure. (???)

Either way this is interesting, because if the measure used to measure inflation that is traditionally the highest is going down, that at least implies the others will lower too. But I guess one could make a pretty solid argument that a measure based on “sentiment” of people mostly with non-specialized knowledge is not very reliable.

Again, for me, I like that pink Cleveland number a lot and Atlanta Fed’s sticky price thingymuhbopper. Lazy-dude is as Lazy-dude does.

Gasoline prices seem the biggest driver of consumer inflation expectations in the short term. They have been roughly flat, nation wide, since mid-May.

Shh – Princeton Steve has been telling everyone on Fox & Friends that gasoline prices are soaring. Of course he needs to on that show for the free bagels, which he now cannot afford.

Most gas stations around me are holding around the $2.56 range. I have been checking around, and there’s one 7-11 that is selling for $2.43, by far the cheapest price in my area. I’m certainly gonna fill up by Tuesday or before if that price holds steady. The only sense I can make out of their gap to other stations is that the station is pretty new, and maybe they are trying to drum up regular customers. Hoping they have a hardcopy NYT there on Tuesday. This aging man still likes holding the hardcopy.

https://cepr.net/may-cpi-puts-inflation-hawks-in-feeding-frenzy/

June 10, 2021

May CPI Puts Inflation Hawks in Feeding Frenzy

By DEAN BAKER

The consumer price index (CPI) rose 0.6 percent in May, with the core index (which excludes food and energy) rising at an even more rapid 0.7 percent. This brought the increases in the overall and core index over the last year to 5.0 and 3.8 percent, respectively.

Does this mean the inflation hawks were right? Did Biden’s recovery package throw too much wood on the fire and is now setting off an inflationary spiral?

A little closer look at the numbers indicates that caution is still advised. First of all, prices plunged last April and May of last year, as the economy was shutting down in response to the pandemic. This means that the year-over-year comparison is not very informative.

To get a more honest evaluation, we should look at the rate of change of prices since February of 2020, before the pandemic was having an impact. Using this as a base, the overall CPI has increased at a 3.0 percent annual rate, while the core has increased at a 2.6 percent annual rate.

The 2.6 percent rate is somewhat above the Federal Reserve’s 2.0 percent target, but the Fed targets the personal consumption expenditure deflator (PCE), not the CPI. For coverage and methodology reasons, the core PCE is generally 0.2-0.3 percentage points lower than the core CPI.

Also, as the Fed has stated explicitly, the 2.0 percent target is an average, not a ceiling. Given that inflation has consistently run well below 2.0 percent, to maintain a 2.0 percent average the inflation rate has to be above 2.0 percent on occasion, so there is nothing in the data to indicate that we have a problem, accepting the Fed’s target.

The Used Car Crisis

In fact, even this above 2.0 percent inflation figure can be a bit deceptive. Used car prices have soared in recent months, rising 7.3 percent in May and 10.0 percent in April. (These are monthly increases, not annual rates of increase.) If we take the period since February of 2020, used car prices have increased at a 23.2 percent annual rate.

The weight of used cars in the core CPI is 3.8 percent. This means that this jump in used car prices alone added almost 0.9 percentage points to the rate of inflation in the core index in the months since the pandemic began. That means that if we pull used cars out of the core index, it would have been increasing at just under a 1.8 percent annual rate since the pandemic began, well below the Fed’s target.

The reason for the jump in used car prices is not a mystery. The worldwide shortage of semi-conductors has slowed auto production, leading several assembly lines to shut down for a period of time. (Most are now back up and running.) The shortage of new cars led many people to turn to buying used cars, sending their prices soaring.

This shortage of cars is a problem. People need cars for transportation and rental car companies need cars to restock their fleets, which they sold off at the start of the pandemic to conserve cash. But this is clearly a temporary problem. Semi-conductor output will increase as existing plants add capacity and new ones come back on line. When that happens, we are likely to see the price of used cars return to something comparable to their pre-pandemic levels. New car prices, which have also risen rapidly, should also fall back in line with pre-pandemic trends.

If we take the car story out of the picture, there is not much of a story of run-away inflation. The prices of some items have been rising rapidly, but this is a bounce back from price declines at the start of the pandemic. Apparel prices jumped 1.2 percent in May, car insurance 0.7 percent, and air fares 7.0 percent. These indexes are respectively 2.2 percent, 0.2 percent, and 6.3 percent below the February 2020 level.

Inflation in the rent indexes remains well contained. The rent proper index rose 0.2 percent in May, while the owners equivalent rent index rose 0.3 percent. Over the last year, they are up 1.8 percent and 2.1 percent, respectively. The medical care index, which has been a major source of inflation, has risen at just a 1.7 percent annual rate since the pandemic began. The index for college tuition has risen at less than a 0.6 percent annual rate.

We will see more erratic price movements as the economy continues to reopen. There will be some spot shortages of different items and there will be cases where strong demand gives workers the bargaining power to raise their wages, but there is not a story of an inflation crisis in these data….

CNN had a nice piece on car prices.

https://www.cnn.com/2021/06/11/business/car-prices-record-high-short-supply/index.html

One interesting piece of information was that seasonally adjusted new car sales in May are 34% higher than 1 year ago but ALSO 10.6% higher than 2 years ago. If they still have problems producing cars that would suggest they are selling out their inventory of new cars.