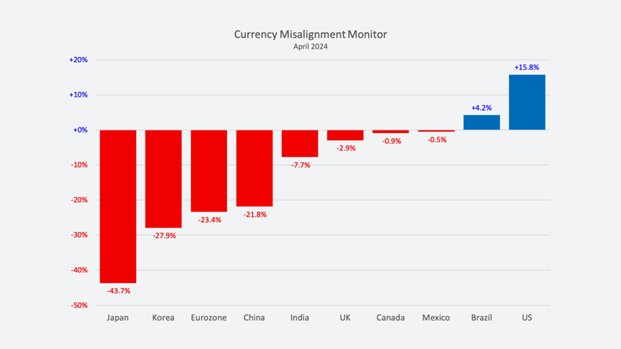

The Coalition for a Prosperous America and the Blue Collar Dollar Institute have developed a measure of currency misalignment, reported in their latest Currency Misalignment Monitor (April issue).

Source: CPA.

Note that the US estimate is for a multilateral balance, while the individual estimates are the implied dollar/local currency change for a given move to an individual country’s “equilibrium” exchange rate.

There’s a reason why I put the word “equilibrium” in quotes. The CPA/BCDI estimate is based on the approach adopted in William Cline’s (2008) SMIM. Using trade elasticities, the overvaluation is defined as the percent depreciation required to bring the current account to balance over time, requiring consistency across all other current account balances. However, Cline’s approach did not assume zero balances were the targets. Hence while the overall mathematical framework is the same (matrices, matrices!), the targets are quite different. In order to see how crazy this zero balance criterion is, this means that “fair” exchange rates are those that mean zero current account balances, which in turn means zero financial account balances. In other words, countries would be neither borrowers nor savers in the medium run. Here’s what this means in terms of an intertemporal model.

Note that no intertemporal trade results (in this case) in a lower indifference curve.

See discussion of earlier CPA analyses of the dollar’s value, here. Discussion of measuring misalignment, here. Contrast with the IMF’s EBA here.

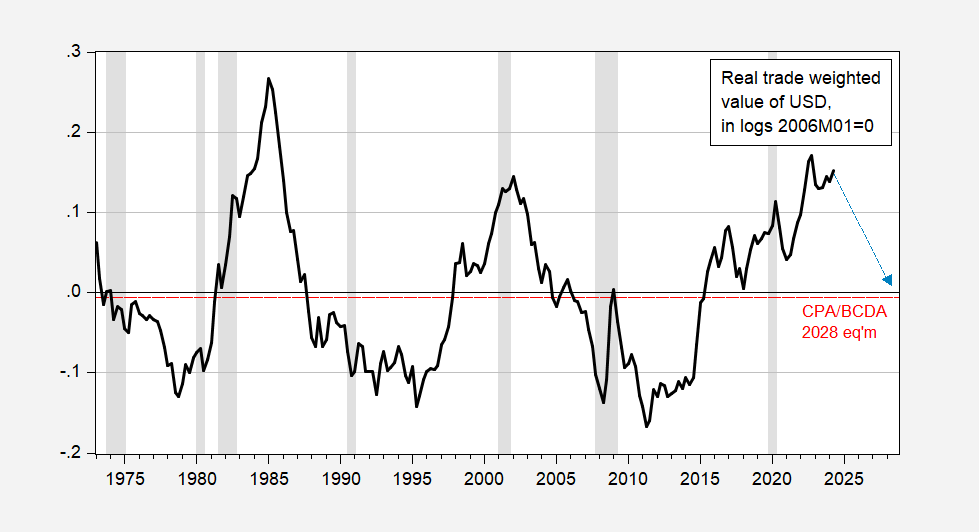

Here’s the implied path for the dollar to hit CPA/BCDI “equilibrium” by 2028.

Figure 2: Broad real dollar value (black), CPA/BCDI “equilibrium” for 2028 (red dashed line), and implied path (blue dashed arrow). 2024Q2 observation is for April. NBER defined peak-to-trough recession dates shaded gray. Source: Federal Reserve via FRED, CPA/BCDI (April 2024), NBER and author’s calculations.

Your graphs of the US real exchange rate show it got stronger after that stupid Trump trade war began. This is exactly what one would expect from the Mundell-Fleming model under floating exchange rates. Their model was an extension of the old fashion IS-LM model that incorporated the trade balance into the IS curve as well as added capital flows to the financial sector of the model. Most discussions of this model notes how fiscal policy becomes less effective under floating rates as fiscal stimulus (like Trump’s tax cut for rich people and his bloating of defense spending) would tend to appreciate the dollar while monetary policy would be more effective (as in Volcker’s tight money under St. Reagan added to the massive appreciation of the dollar in the early 1980’s). The model also suggests that trade protection so appreciates the currency that net exports do not change.

First the IS curve that specifies output (Y) as the sum of domestic (D) plus the trade balance (B) where:

D = d0 + d1(Y) – d2(r), r = interest rates, and

B = b0 – b1(Y) + b2(e), e = the price of foreign currency.

Next the LM curve where money supply (m) = money demand = m0 + m1(Y) – m2(r).

Finally the balance of payments = B + capital flows, where the latter rises as domestic interest rates rise relative to foreign interest rates.

The balance of payments, however, must be zero under floating exchange rates to any increase in either capital flows or net exports will lower the price of foreign currency. Trade protection may lower imports under fixed exchange rate which can be seen as an increase in b0. But the model notes that the fall in the price of foreign currency (e) is given by:

negative the change in b0/b2, which necessarily implies exports fall as much as imports fall. In other words, trade protection policies are completely ineffective under floating exchange rates.

Now I would submit that this is precisely what happened in 2018 and 2019, a stupid trade war that so appreciated the dollar that exports fell as much as imports did.

Now I get Bruce Hall will never see this effect even after looking pretty hard and his minnie-me Steven Kopits will say this does not pop out. But it is standard international macroeconomics, which may explain why these two MAGA trolls will never understand it.