On Face the Nation, on timeline, impact:

HASSETT: …look at futures markets, which are interesting because you’ve cited over and over the spot price of gasoline, which, of course, is affected right now by the disruption of the strait, but if you look at the futures prices, they are expecting a rapid, rapid end to the situation and much, much lower prices. In fact, I don’t think I’ve seen a sort of future price path with such a steep decline in all my years watching futures.

…

HASSETT: Well, first of all, you have to understand that America is not going to have its economy harmed by what the Iranians are doing. The bottom line is that in the ’70s we didn’t produce much oil, but now we do. So America is in a very strong position. They think that they’re going to harm the U.S. economy and get President Trump to back down. There couldn’t be anything that was a stupider thing to say because the bottom line is that our economy has got all this momentum in the world and we’ve got lots and lots of oil.

So, unlike in the 1970’s, there’s not a large terms of trade effect (we import and export oil and oil products). But apparently in Hassett’s mind, there is no cost-push inflation effect, because the disruption of 20% of world oil trade will be temporary.

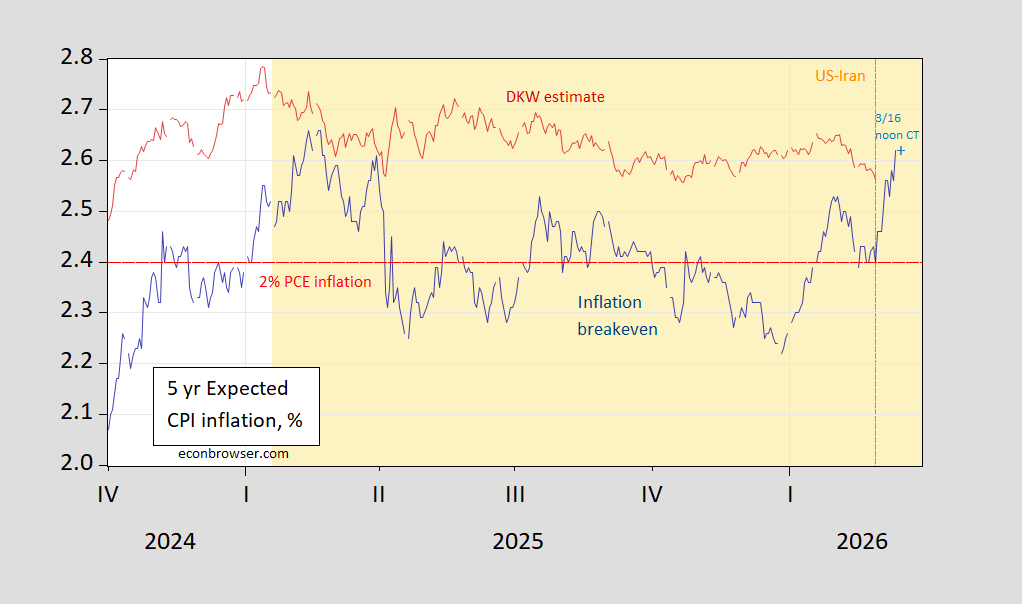

I’ll just note at this point that, in addition to this assessment being at variance with investment bank economics department assessments, the 5 year inflation breakeven has risen about 0.22 percentage points since the outbreak of the war as of today.

Figure 1: 5 year Treasury-TIPS spread / inflation breakeven (blue), DKW estimated 5 year inflation (red), both in %. 3/16 observation at noon CT. Source: Treasury via FRED, Federal Reserve Board, Bloomberg.

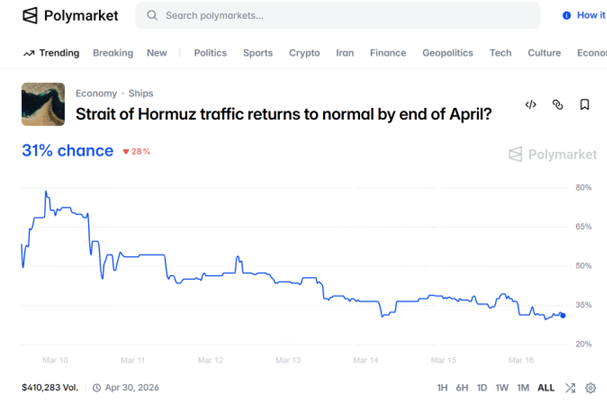

From the prediction markets, Polymarket has the odds of the Strait opening by end-April at 31%.

In other words, the threatened deployment of a CRG to the region has not materially altered the odds. I will observe that I do not see how, for instance, seizing Kharg Island and its oil processing facilities would increase the chances that tankers and cargo ships will be able to transit the Strait (although Robin Brooks has argued that depriving Iran of oil exports by the US blockading Strait would induce Iran to relent; whether seizure and possible damage to the oil facilities on Kharg Island would result in the same outcome is up in the air).

(On the forecasting record, Dr. Hassett predicted zero daily fatalities due to Covid-19 by mid-May 2020).

My favorite part was the very end, and Miss Brennan goes “So a 6 week war for $6,000,000,000??” Dry/Straight humor is sweet as honey sometimes.

Hassett can’t even keep a straight face when he listens to himself dish out scoop-loads of bullcrap

Anyone have a fact-based understanding of what the Houthis are up to? They have not done anything since the war on Iran began to help Iran, but claim to be ready “should developments warrant it”:

https://www.yahoo.com/news/articles/yemens-houthis-join-mideast-war-145117102.html

Saudi Arabia has a major petroleum export facility, Yanbu al Bahar, on the Red Sea. It has reportedly stepped up shipments substantially since Hormuz has been closed:

https://www.reuters.com/business/energy/saudi-aramco-boosts-red-sea-oil-shipments-hormuz-disruption-curbs-exports-2026-03-06/

Bab el Mandeb is to the Red Sea more or less as the Strait of Hormuz is to the Persian Gulf, only narrower; shipments from Yanbu al Bahar have to pass through either Bab el Mandeb or the Suez Canal, and the Suez has limit capacity.

So Saudi Arabia can continue to export oil, though at a reduced rate, while Kuwait, Qatar and the UAE cannot. Notably, Saudi Arabia has mostly stayed out of the attack on Iran.

So is that the deal? Saudi Arabia gets to export through Bab el Mandeb as long as it doesn’t do anything to hurt Iran?

The Houthis are quite droned up:

https://smallwarsjournal.com/2025/12/30/the-houthi-model-non-state-actors-and-multi-drone-capabilities/

They could, presumably, do more damage than simply closing down Bab el Mandeb.

I’ll ignore Hassett, because you shouldn’t wrestling with pigs and because ine of my points in response to Brooks seeves for Hassett, as well.

Brooks is mixing geopolitical forecasting with market forecasting. That’s unavoidable, but also really fraught with risk of error. Humility and a consideration of alternative scenarios, not claims of foreknowledge, are the credible path.

It’s just part of the investment analysis landscape that economists and market specialists are called upon to perform polotical analysis; most shops don’t have the budget for a political scientist, so thst function falls to others. Getting comfortable in that role is a mistake, and Brooks commits that mistake here.

Now, about that oil price spike. Brooks points to that spike to claim that the unitial reaction was overdone. He then extends that point to claim that fear of higher prices in the future is overdone. Brooks seems to misunderstand that price spike.

End users of oil have very different motives than do brokers, wholesalers ans speculators. End users have large expenses, contractual obligations and the like, all of which will go BLOOEY!!! if they can’t get oil. If a firm can operate in the short run at $120/bbl oil and it looks like there may be an interruption in supply, that firm will lock down future delivery at any price up to $120. Having done so, job done. The next day, the bid at $120 is gone.

Brooks claims that spike and subsequent price decline represents an error, a panic. He is ignoring the possibility that end users were making an entirely rational grab at future physical delivery of oil.

If you look at Brooks’s chart, but ignore the spike, the trend is toward higher prices, not lower. His point about prices coming into weekends higher than the open on Monday is either naive or disingenuous. Grabbing futures ahead of a weekend in which news can’t be traded is caution, and is common as all get-out. If he doesn’t know that, he has no business talking about short-term market fluctuations. Both Brooks’s arguments based on short-term price fluctuations are not well-founded.

I’m sure Brooks is better at economics than I am. No question. But good golly, the man needs to give up his pretensions to understanding geopolitics or short-term market behavior.

Hassett, too, of course.