Asset price movements around “news” regarding policy can illuminate the market’s assessment of the outlook for trade policy. Looking at a small window (say half hour) around an event can allow one to separate other factors (weather, other demand factors) from other. With that, let’s look at soybean futures (September 2019)…

“Purchasing Power Parity and Real Exchange Rates”

That’s my new entry in the Oxford Research Encyclopedia of Economics and Finance.

The idea that prices and exchange rates adjust so as to equalize the common-currency price of identical bundles of goods—purchasing power parity (PPP)—is a topic of central importance in international finance. If PPP holds continuously, then nominal exchange rate changes do not influence trade flows. If PPP does not hold in the short run, but does in the long run, then monetary factors can affect the real exchange rate only temporarily. Substantial evidence has accumulated—with the advent of new statistical tests, alternative data sets, and longer spans of data—that purchasing power parity does not typically hold in the short run. One reason why PPP doesn’t hold in the short run might be due to sticky prices, in combination with other factors, such as trade barriers. The evidence is mixed for the longer run. Variations in the real exchange rate in the longer run can also be driven by shocks to demand, arising from changes in government spending, the terms of trade, as well as wealth and debt stocks. At time horizon of decades, trend movements in the real exchange rate—that is, systematically trending deviations in PPP—could be due to the presence of nontraded goods, combined with real factors such as differentials in productivity growth. The well-known positive association between the price level and income levels—also known as the “Penn Effect”—is consistent with this channel. Whether PPP holds then depends on the time period, the time horizon, and the currencies examined.

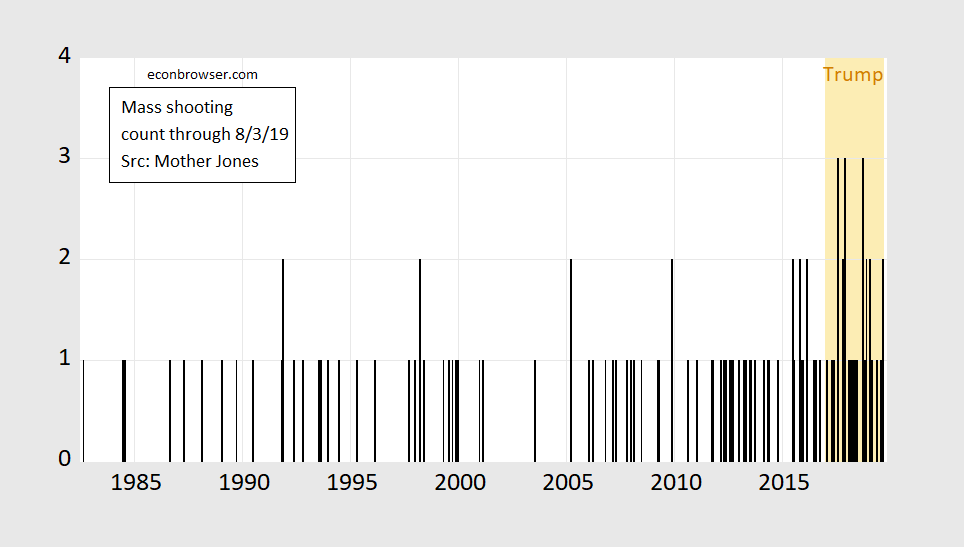

Mass Shootings and the Trump Effect (Part II)

Casualties (killed, wounded) from mass shootings are not continuously distributed; this suggests an alternative approach — given the high variance (shown in Figure 1 below for a subsample of the data) — I estimate a negative binomial regression (quasi-maximum likelihood).

Mass Shootings and the Trump Effect

Poisson regression, 1982M08-2019M08 (thru 8/4 for August):

eventst = -9.84 + 0.723 trumpt – 0.424 bant + 0.0039 time

Adj-R2 = 0.17, SER = 0.480, NOBS = 445. Bold denotes significant at 10% msl.

Addendum, 8/6 8am Pacific: events is mass shooting event count as defined by Mother Jones tabulation, ban is assault weapons ban dummy, trump is a Trump administration dummy, time is a linear time trend.

Interpretation: Each month of the Trump administration is associated 0.7 more mass shooting events 70% more mass shooting events, so jumping from 0.43 to 0.88 events going from 2016M12 to 2017M01; or approximately 5.4 more events per year 8.4 more events per year. [h/t Rick Stryker for correction of interpretation].

The Answer Is No (and No)

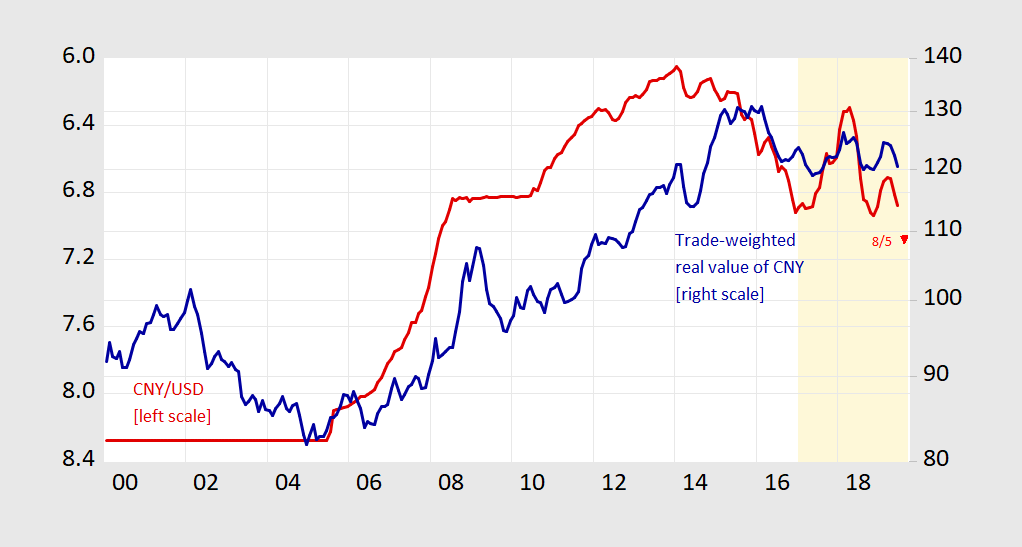

Figure 1: CNY/USD nominal exchange rate (red, left inverted scale), 8/5 value (red triangle, left inverted scale), trade weighted real value of CNY against broad basket of currencies (blue, right log scale). Up denotes appreciation. Light orange shading denotes Trump administration. Source: FRED, and BIS.

In a new (and extremely timely) EconoFact memo on Should the United States Try to Weaken the Dollar?, Michael Klein and Maury Obstfeld ask:

Business Cycle Indicators as of 8/4/2019

Still rising, so likely no recession as of June 2019.

The 16 Month-long Blip in Soybean Prices

On July 9, 2018, reader CoRev disparaged futures prices as accurate predictors of future spot prices for soybeans, writing:

no one has denied the impact of tariffs on FUTURES prices. Those of us arguing against the constant anti-tariff, anti-Trump dialogs have noted this will probably be a price blip lasting until US/Chinese negotiations end. We are on record saying the prices will be back approaching last year’s harvest season prices.

A Business-Cycle Mystery: Manslaughter or Murder?

If recoveries don’t die of old-age, then they either have “accidents” or they’re murdered. I’m not sure what a business-cycle accident is, but we can check what might have killed the recovery, should we enter a recession in 2020, as suggested by some forward looking financial indicators. I’ll look at investment spending, a forward looking variable, highly sensitive to interest rates, and the outlook for economic activity and uncertainty.

Estimated Recession Probabilities, August 2019

Based upon July 2019 spreads

Equipment Investment, Capital Goods Imports, and the Impending Slowdown…Again

Equipment investment is flat; capital goods imports (aside from aircraft and computers) declining 4% per annum.