(Well, actually, the recession had been underway for nearly ten months, and after Lehman Brothers, on October 26th, 2008). Or why I worry about the White House economic policy management team.

NO DEPRESSION; NO SEVERE RECESSION

The medium term fundamentals point toward more real GDP, more employment, and (to a lesser degree) more consumption. Some employment and real GDP declines may occur in the short run, but they will be small by historical standards. Professor Cooley recently explained “The losses to date represent less than .5% of the work force. In the relatively mild recession of 2001 to 2002, job losses equaled about 1% of the work force. In the much more severe recession of 1981 to 1982, job losses totaled nearly 3% of the labor force–six times today’s figure. And in the (truly) Great Depression–invoked, now, with an alarmist frequency–job losses between 1929 and the trough in 1933 were 21% of the labor force.” Note that 21% over 3 1/2 years is an average decline of 2% every quarter for 14 consecutive quarters! If employment declines 2% in even one quarter, or 5% over a full year, I will admit well before 2010 that a severe recession is happening and that my 2010 forecasts are unlikely to be attained.

According to the BLS, national nonfarm employment was 136,783,000 (SA) at the end of 2006, as the housing price crash was getting underway. Real GDP was $11.4 trillion (chained 2000 $). Barring a nuclear war or other violent national disaster, employment will not drop below 134,000,000 and real GDP will not drop below $11 trillion. The many economists who predict a severe recession clearly disagree with me, because 134 million is only 2.4% below September’s employment and only 2.0% below employment during the housing crash. Time will tell.

More on Dr. Mulligan’s analyses here: [1] [2] [3] [4] [5] [6] [7] [8]

Here’s what the most recent vintages of the data say about Dr. Mulligan’s forecasts (recalling that ARRA was passed in February 2009). (A discussion of using the data available to Dr. Mulligan at the time of his forecast, see this post.)

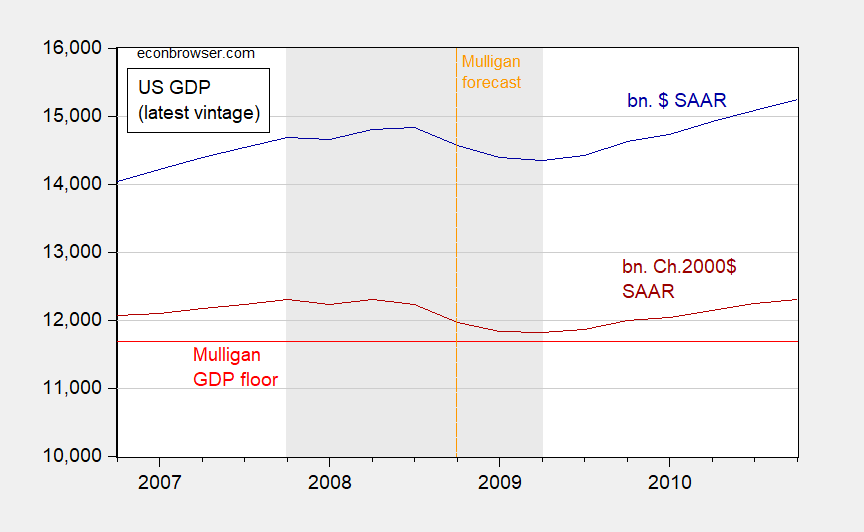

Figure 1: GDP in billions of $ (blue), and in billions Ch.2000$ (dark red), SAAR. GDP calculated using GDP deflator adjusted to 2000=1. Mulligan GDP floor in bn. Ch.2000$ SAAR, calculated by subtracting 0.4 trn from 2006Q4 real GDP. NBER defined recession dates shaded gray. Source: BEA, 2019Q1 second release, NBER, and author’s calculations.

Notice that realized GDP in 2009Q2 was only 0.55% above the Mulligan floor. Since CBO low/high estimates of the impact of the ARRA — passed in 2009Q1 — was 1.2% to 2.4%, this means that Mulligan’s floor would’ve been breached in the absence of the ARRA. (If you are wondering about the calculations, CBO midpoint is 1.8% impact, so 0.982 of realized 2009Q2 GDP expressed in 2000$ is 11603, while 0.4 trn below 2006Q4 levels is 11668.)

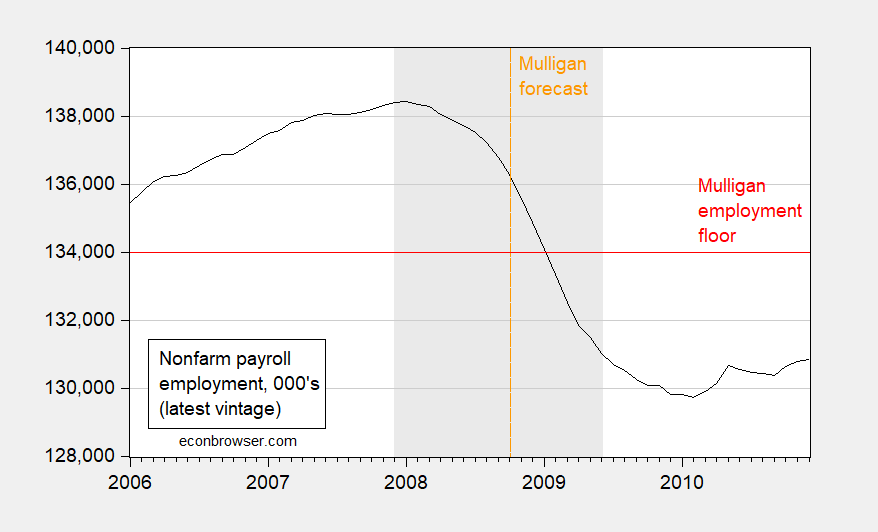

What about employment? Well, even with the ARRA, we blew way past the Mulligan floor of 134 million. This is shown in Figure 2.

Figure 2: Nonfarm payroll employment in thousands, s.a., (black). NBER recession dates shaded gray. Source: BLS, May release, and NBER.

Let me observe that we breached Mulligan’s floor even before passage of the ARRA. So if we believe — as Mulligan did, and apparently still does, — that the ARRA increased labor wedges thereby worsening the recession, he missed (since to my knowledge, no nuclear war occurred).

So, now that I’m pretty sure a slowdown is coming, and a recession highly likely, I’m ever more worried about the economic crisis management team at the White House. I hope I will be proved wrong.

Interesting fact: Mulligan wrote his October 2008 post after Don Luskin wrote his September column, thereby showing that an actual advanced degree in economics (Luskin has no degree at all) is no protection against complacency.

Are you trying to tell us that if Casey Mulligan was paid a nice monthly salary to hoodwink “the great unwashed” masses that the wind was moving in the opposite direction than reality was authenticating, that Casey couldn’t stand outside and tell us which way the wind is blowing??

https://youtu.be/_4ezPvzKe5M?t=58

Actually he is saying Casey Mulligan was more clueless than Donald Luskin!

“Barring a nuclear war or other violent national disaster, employment will not drop below 134,000,000 and real GDP will not drop below $11 trillion. The many economists who predict a severe recession clearly disagree with me, because 134 million is only 2.4% below September’s employment and only 2.0% below employment during the housing crash. Time will tell.”

The collapse of Lehman Brothers was part of a violent national disaster aka the troubled financial institution sector. The melt down of our automobile sector was a national disaster. All of this was well known when Mulligan wrote this. No wonder many economists disagreed with him at the time. It sort of sort of like me wondering why people took umbrellas this morning when I was on my run – BTW I got very wet.

No jogging. Oprah Winfrey says it’s bad for you. 9 boxes of Weight Watchers per meal, 4 times daily, is the pathway to better health. This is because if you do calisthenic or aerobic exercise you will miss out on the Oprah Winfrey certified tire around your midsection—one of the key chakras to an aligned soul spirit.

Our good man, Mr Edward Leamer, giving his views on a possible recession. I’ve said before I take great joy in listening to Mr. Leamer’s presentations as I like his dry style of humor and just seems like a solid person. I also like his pal David Shulman who also has a good sense of humor and is a joy to soak up the knowledge from. In an ideal world these type guys would either be on the President’s CEA or on the mobile phone speed dial of the young bucks (like Menzie or Gita Gopinath) working on the CEA for advice in times of uncertainty. We don’t live in that ideal world, but it’s fun to daydream about:

Professor Leaman—–>> https://www.youtube.com/watch?v=6iYy3khe7ZI

Professor Shulman——>> https://www.youtube.com/watch?v=G8l568G-Rcg

Dear Folks,

Unfortunately, though he is exaggerating it a bit, Moses Herzog is correct. Is there a way to check whether there is some sort of a respect for actual data and unbiased conclusions in an administration, or “Your job is to make the President look good, and use whatever techniques you have to do it”?

J.

Yesterday afternoon, Bill McBride again said that he’s not on recession watch and has not been since 2007. The Great Recession began in late 2007. What that tells me is that when he goes onto recession watch, we are only a few months away from the bottom falling out. In my line of work, I saw signs of a downturn sometime in 2006. The economy had turned, and the signs were in the air for a decent while before anybody said anything about it. I’m doing different and more interesting work now, thanks to the Great Recession, which means I don’t have the same kind of immediate information. That said, what I see around me tells me that things will be wrapping up in the next 18 months or less and we are headed for slower or no growth. I still don’t think we will be into a recession before the end of this year, but a recession or an economy that feels like a recession to knuckle draggers like me is far more likely.

Willie,

The earliest sign of recession starting in late 2006 was declining residential construction after the housing bubble peaked in mid-summer of that year. Dean Baker and Nouriel Roubini jumped on that to predict that the US would enter recession at the beginning of 2007, but a low value of the dollar propped up exports and kept down imports sufficiently to hold off the recession until the end of 2007.

Being a great blogger and being a great forecaster are two different things. McBride knows real estate. Now one can make an argument real estate is closely tied to the economy and that’s fine. But real estate isn’t what tipped Lehman or the other TBTF banks over, or created the derivatives crisis. And if McBride is saying he called the crisis pre-Lehman instead of implying he did with cute wording—then McBride can link the post where he “called” the recession in this comment thread anywhere he likes. I keep hearing people repeat this mantra that McBride “called” the recession, but I have never seen the damned post. The closest one that I had seen was Roubini. And even Roubini could have been claimed to just be yelling “fire!!!” so many times that it finally happened.

https://www.marketwatch.com/story/coming-recession-will-be-nastier-than-2001s-economist-says

When I attempt these things, I give myself an entire year’s time margin, because the truth is, I don’t know. I think I gave myself a 13 months time margin somewhere on this blog on when I thought the recession would happen. Is that a recession “call”?? Of course I will try to brag if it happens, but it’s not really a recession “call”. “Calling” a recession inside a 13 months timespan (I think I said late June 2019 to late July 2020?? Anyone can correct me if I’m remembering that wrong) is just giving myself more chance not to be blatantly wrong.

Oh, Moses, I really do not wish to argue with you as you are likely to make it personal, but you are simply wrong on this one. It was real estate. The collapse of the housing bubble was what did in all the shadow banking pyramid schemes. See my post above. As it was at the time, I did call it, very closely. Dean Baker has even publicly agreed that the analysis that I reported above was right, and I delivered it in real time. He and Roubini were right that residential construction was falling after the peak of the housing bubble, but they ignored the low dollar. All three of us and a few others were aware to varying degrees about the pyramid of of over-leverage that had built up on all those mortgage -backed securities that went bust and brought us late 2008.