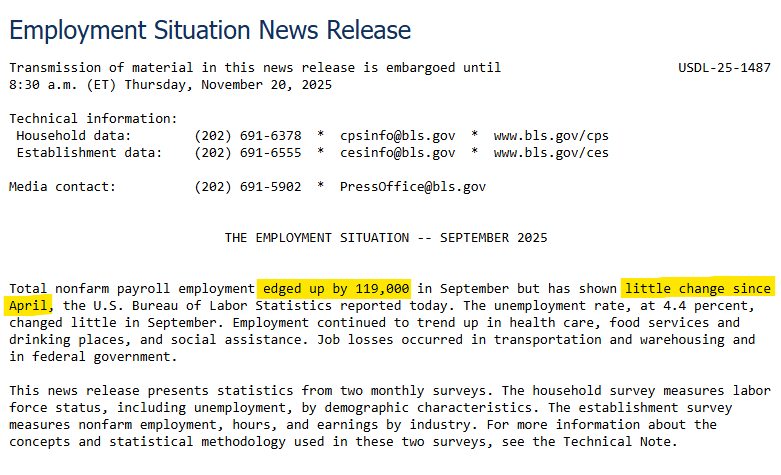

From EJ Antoni on X today:

Not even hiding it anymore – since when is a 119k increase just “edging up”? And since when is a 193k increase “little change”? They mentioned Apr b/c that’s when Trump announced tariffs; whether you’re for or against Trump’s trade policies, this is obviously a biased narrative: