Today, we present a guest post written by Jeffrey Frankel, Harpel Professor at Harvard’s Kennedy School of Government, and formerly a member of the White House Council of Economic Advisers. Sohaib Nasim contributed to this commentary. A shorter version was published by Project Syndicate.

Category Archives: Uncategorized

Updating Antoni-St.Onge (2024): The 2022 Recession Is Over!

Recall, EJ Antoni and Peter St. Onge argued the US economy has been in recession since 2022.

CA, NY, and the Nation: GDP vs. Employment

Mark Zandi has asserted that whether the US goes into recession depends on how CA and NY economies evolve. If we rely on GDP to define activity, then the outlook appears sunny.

Growth Deceleration Relative to “Liberation Day”

Lewis, Mertens, Stock Weekly Economic Index (WEI) is down 1.1 ppts, while Baumeister, Leiva-Leon, Sims Weekly Economic Conditions Indicator (for deviation from trend growth) is down 0.7 ppts.

Non-Federal Statistic of the Day: Recession Predictor?

We would’ve gotten Q3 advance GDP yesterday, and September personal income and outlays today, ordinarily. What indicators do we have for the state of the macroeconomy? Here’s one: delinquincies on auto loans (for pools of asset backed securities).

ACA Premiums without Extension of Expanded Tax Credit

Data from Pew, for average marketplace benchmark plans, per month:

Trump: China to buy a “tremendous” amount of soybeans

Per Bloomberg. Hmm. Commitment to 12 mn metric tons (MMT) “this year” (calendar, market?).

Hi Frequency Readout on Consumer Prices, Thru 12 October

Given we’re unlikely to get a CPI release for October…

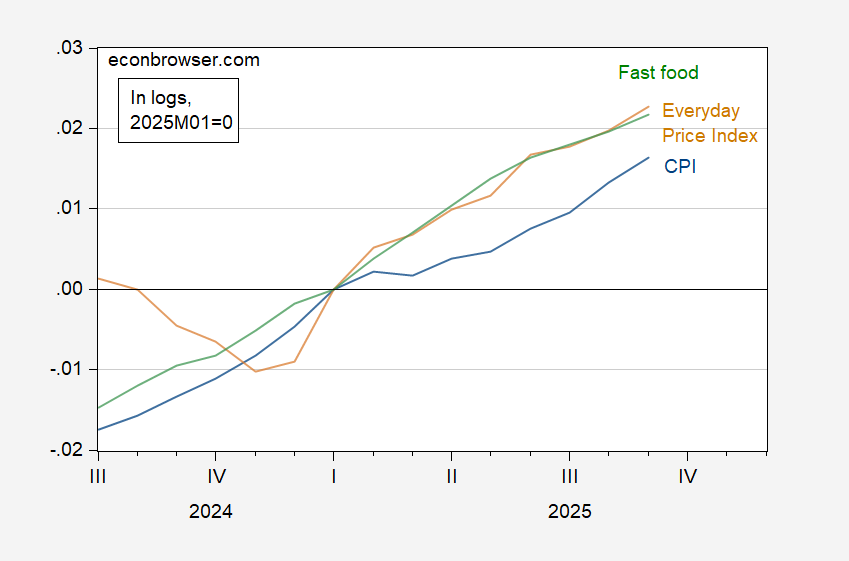

Everyday Prices Up 2.2% since Jan. 2025

That’s the AIER Everyday Price Index ™ in September:

Figure 1: CPI all urban (blue), Everyday Price Index (tan), and CPI for limited service restaurants (green), all in logs, 2025M01=0. CPI for limited service restaurants seasonally adjusted by author using X-13. Source: BLS, AIER, and author’s calculations.

Up 2.3% in log terms.

CBO on Macro Effects of the Shutdown

From ” A Quantitative Analysis of the Effects of the Government Shutdown on

the Economy Under Three Scenarios, as of October 29, 2025″: