Lewis, Mertens, Stock Weekly Economic Index (WEI) is down 1.1 ppts, while Baumeister, Leiva-Leon, Sims Weekly Economic Conditions Indicator (for deviation from trend growth) is down 0.7 ppts.

Non-Federal Statistic of the Day: Recession Predictor?

We would’ve gotten Q3 advance GDP yesterday, and September personal income and outlays today, ordinarily. What indicators do we have for the state of the macroeconomy? Here’s one: delinquincies on auto loans (for pools of asset backed securities).

ACA Premiums without Extension of Expanded Tax Credit

Data from Pew, for average marketplace benchmark plans, per month:

Trump: China to buy a “tremendous” amount of soybeans

Per Bloomberg. Hmm. Commitment to 12 mn metric tons (MMT) “this year” (calendar, market?).

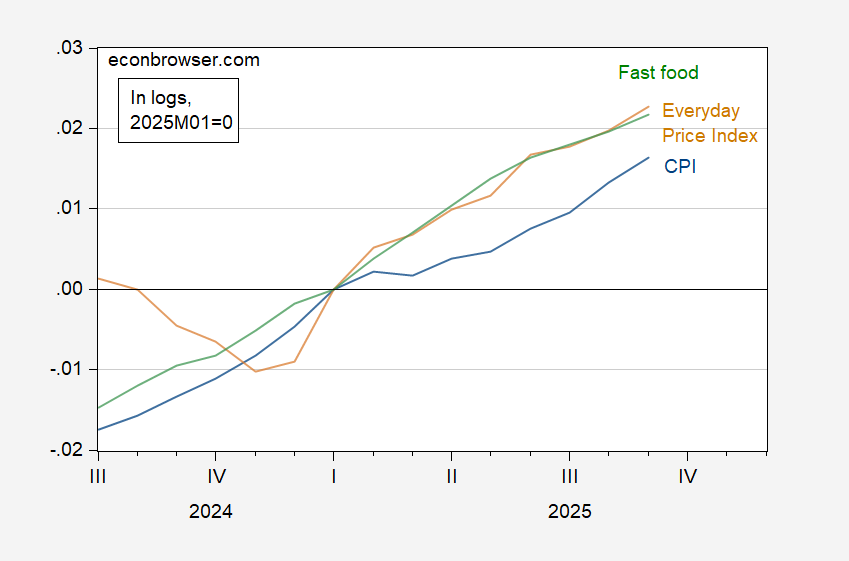

Hi Frequency Readout on Consumer Prices, Thru 12 October

Given we’re unlikely to get a CPI release for October…

Everyday Prices Up 2.2% since Jan. 2025

That’s the AIER Everyday Price Index ™ in September:

Figure 1: CPI all urban (blue), Everyday Price Index (tan), and CPI for limited service restaurants (green), all in logs, 2025M01=0. CPI for limited service restaurants seasonally adjusted by author using X-13. Source: BLS, AIER, and author’s calculations.

Up 2.3% in log terms.

CBO on Macro Effects of the Shutdown

From ” A Quantitative Analysis of the Effects of the Government Shutdown on

the Economy Under Three Scenarios, as of October 29, 2025″:

Conference Board Confidence Down Slightly

Both Michigan Sentiment and CB Confidence declined in October.

Macro Implications of Withholding Contingency Funding of SNAP

Contingency funds are available to fund SNAP disbursements for at least part of November. OMB Director Vought’s unprecedented decision to prohibit use of these funds will have macro implications (I eschew any moral or ethical judgments in this discussion), especially if the government shutdown continues.

States with Negative GDP, Employment Growth in 2025H1

Eleven states for GDP, ten for employment: