Why bother with econometrics when revealed truth will do?

Some Macro Implications of a Minimum Wage Hike

With updates on the econometric debates on effects, and efficacy in targeting low income groups (3/30)

Minimal employment number impacts and minimal inflation impacts. But I am sure the resistance to having a greater share of income going to labor will continue.

Russia to Recession?

From Reuters:

Russia is at risk of recession as investors pull money out of the country, with growth likely to evaporate if capital outflows reach $100 billion, the head of its largest bank, state-owned Sberbank, said on Monday.

Graphs of key economic trends

Here are some graphs of economic data that illustrate some interesting trends.

Crimes and Punishments

How vulnerable to sanctions — official and market-driven — is Russia?

The Midwestern Laggard

Wisconsin continues to lag the other regional economies

Time for Some Traffic

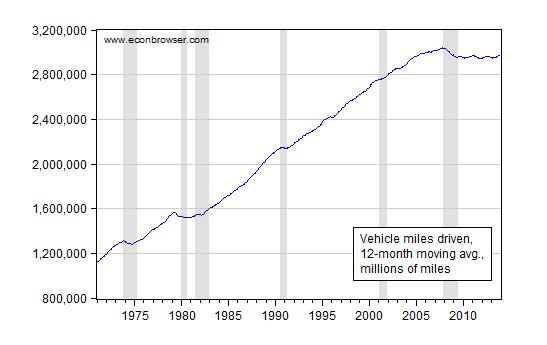

Total vehicle miles driven in the United States have not re-attained pre-recession peaks.

2014 Econbrowser NCAA tournament challenge

It may be snowing back east, but March Madness has arrived just the same. Time to invite everyone to test your uncanny ability to predict the outcome of the U.S. college mens’ basketball tournament. Field seems particularly wide open this year. If you want to participate, go to the Econbrowser group at ESPN, do some minor registering to create a free ESPN account if you haven’t used that site before, and fill in your bracket with who you think might be the winners of each game. Just be sure you complete your predictions before Thursday, because the Econbrowser group does not allow changes in your bracket after the round of 65 begins on Thursday.

Addressing growing student debt

Mortgage and credit card debt today are lower than they were before the Great Recession. But the dollar value of outstanding student loans has surged, growing from 4% of GDP in 2007 to over 7% today.

“The Jeep Plant Mitt Romney Said Was Moving to China Is Hiring 1,000 Workers in Ohio”

That’s the point of a Bloomberg article:

Anyway, that Jeep plant? It didn’t move to China. And it’s actually doing quite well. No, scratch that: It’s going gangbusters. Demand for Jeeps is so high that Chrysler workers are clocking 60 hours a week and still can’t keep up.

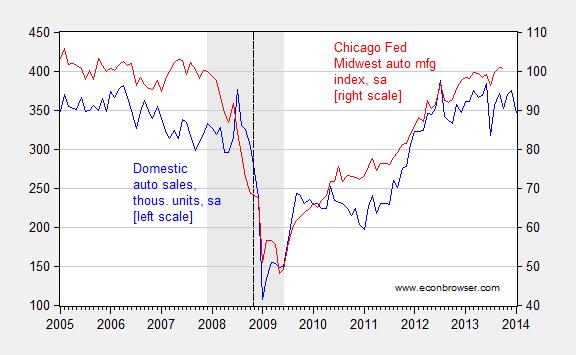

Figure 1 illustrates the context.

Figure 1: Auto and motor vehicle sales, thousands of units (blue, left scale), and Chicago Fed motor vehicle manufacturing index, 2007=100 (red, right scale), both seasonally adjusted. NBER defined recession dates shaded gray. Vertical dashed line at “Let Detroit Go Bankrupt”. Source: FRED.

Update, 3/16, 6PM Pacific: Reader Patrick R. Sullivan writes:

Looking at Figure 1, I’d say that sales of cars are pathetic. Only back to the level of 2005. And that after years of far below normal sales figures, which should have resulted in pent-up demand. This is nothing to brag about for this economy.

I think it is useful when thinking about production trends to consider the end-use of the product. One interesting point is that vehicle miles driven has declined, and is essentially flat, despite the fact that GDP has exceeded pre-recession peaks. This is shown in Figure 2.

Figure 2: Vehicle miles driven, 12 month moving average, in millions. NBER defined recession dates shaded gray. Source: Federal Highway Administration via FRED.