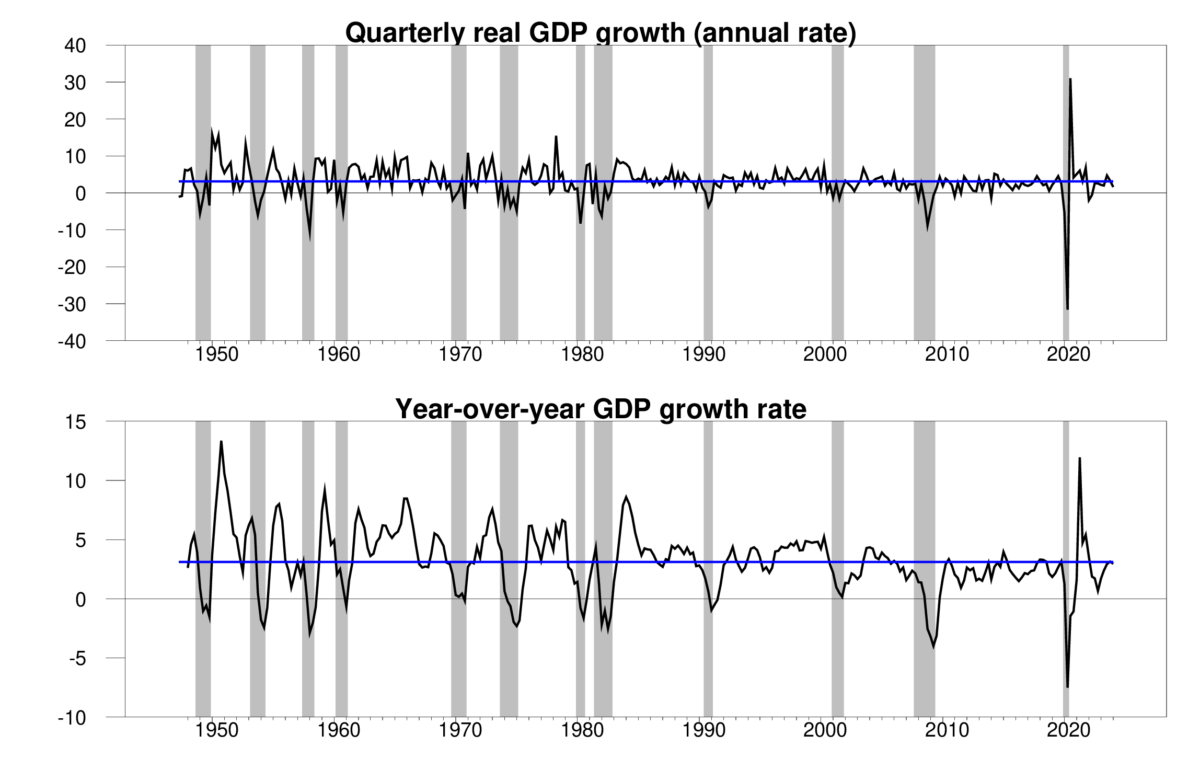

The Bureau of Economic Analysis announced today that seasonally adjusted U.S. real GDP grew at a 2% annual rate in the first quarter. That is below the historical average growth of 3.1% and also below some analysts’ expectations for the Q1 numbers. The new BEA report also revised down the estimate of the Q4 annual growth rate. The latter was originally reported to have been 1.4% but is now estimated to have only been 0.5%.

Continue reading

A worried Econ Watcher

7 Replies