As measured by near month futures:

As measured by near month futures:

Reader Ed Hanson insists I plot soybean prices from 2014 onward, instead of 2016, to show how factors other than tariffs affect soybean prices. I am happy to accommodate his request. I wonder why soybean prices suddenly deviate from grains overall, starting in March 2018.

That’s what reader sammy asserts, trying to support the proposition that Chinese retaliatory tariffs on imports of US soybeans had no impact on US soybean prices.

… chart of soybean prices there are a number of other commodity price charts, such as copper, wheat, coffee etc. They are unaffected by the tariff war yet are remarkably similar to the soybean chart.

Back in July 2018, reader CoRev wrote:

…no one has denied the impact of tariffs on FUTURES prices. Those of us arguing against the constant anti-tariff, anti-Trump dialogs have noted this will probably be a price blip lasting until US/Chinese negotiations end. We are on record saying the prices will be back approaching last year’s harvest season prices.

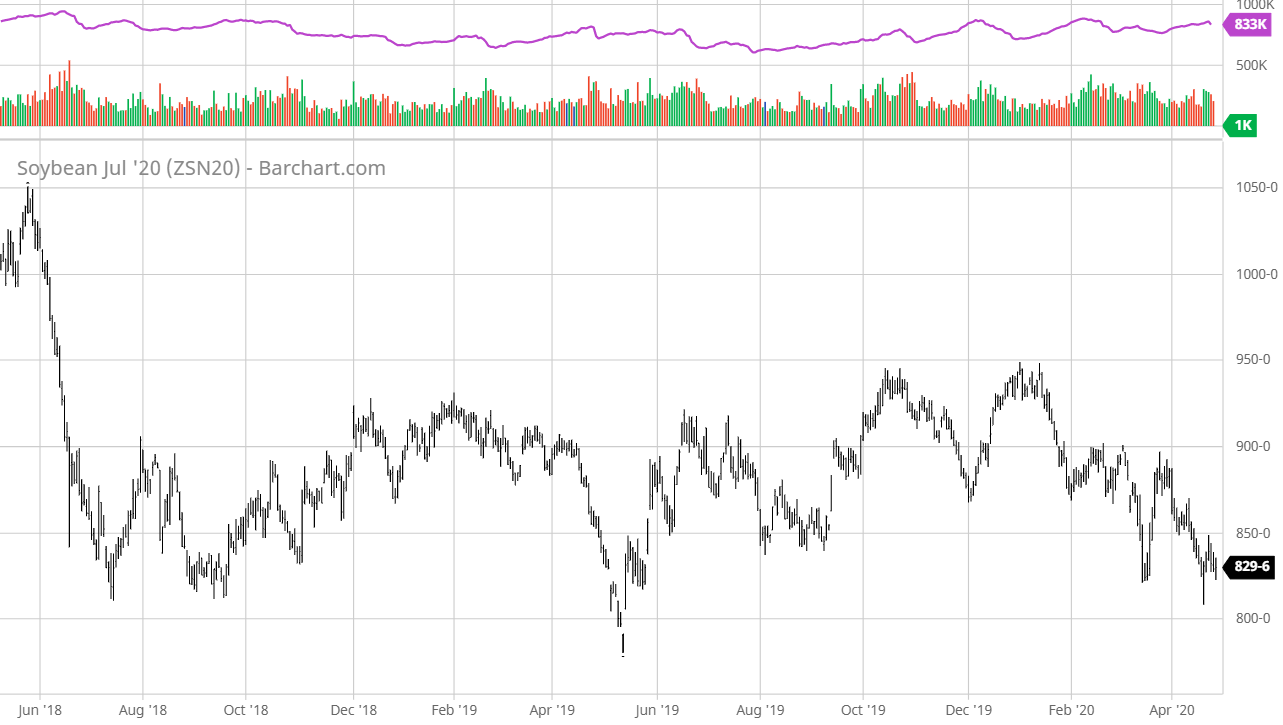

Back on March 23rd, when Mr. Trump announced intent to launch Section 301 actions, nearest month soybean futures closed at 1028. Latest today is 902. Indeed, prices have been falling since Mr. Trump signed the much heralded (by some) Phase 1 deal. This is shown in Figure 1 below.

Figure 1: Front month soybean futures (black). Trump announces intent of Section 301 action against China (red), Section 301 tariffs and Chinese retaliation in effect (orange arrow), and Phase 1 deal signed (blue arrow). Source: barchart.com.

Front month futures prices are now 14% lower now, while the CPI is 2.2% higher (both in log terms). You can do the math. The “blip” is not over.

By Menzie Chinn and Bill Plumley, at EconoFact, posted a few minutes ago:

U.S. agriculture has been caught in the tit-for-tat of the trade wars. Retaliation by China, Canada, Mexico, Turkey and members of the European Union to tariffs imposed by the Trump administration have taken a bite out of U.S. agricultural incomes. Tariffs on imports of steel and aluminum in the United States have also raised costs for machines, equipment and structures used by the agriculture sector. Agriculture incomes would have shown no growth in 2019 but for massive and unprecedented federal assistance. Even with this assistance, however, the agriculture sector shows signs of stress, with a rise in debt, a decrease in solvency and an increased number of bankruptcies.

Despite repeated explanations, some readers still don’t understand futures contracts and forecasting exercises. One point of Chinn-Coibion (2014) is that at the one year horizon, the best predictor of future soybean prices at a one year horizon is the futures contract expiring one year ahead.

Reuters: After trade talks in U.S., China ramps up Brazilian soy purchases:

Nearest month futures are about a dollar lower (at $9.34/bushel) than the nearest month futures on the day when Trump announced Section 301 action against China.

On July 9, 2018, about 14 months ago, reader CoRev wrote:

Those of us arguing against the constant anti-tariff, anti-Trump dialogs have noted this will probably be a price blip lasting until US/Chinese negotiations end. We are on record saying the prices will be back approaching last year’s harvest season prices.

Hah, hah, hah, hah! Time to look at prices relative to March 23, 2018, when Trump announced imposing Section 301 tariffs on Chinese goods…

Well, over the past year, employment growth has been pretty lackluster in the Midwestern states that Trump was going to revive in terms of manufacturing … and in terms of agriculture…

Today, we’re fortunate to have Willem Thorbecke, Senior Fellow at Japan’s Research Institute of Economy, Trade and Industry (RIETI) as a guest contributor. The views expressed represent those of the author himself, and do not necessarily represent those of RIETI, or any other institutions the author is affiliated with.