It looks even worse than shown in this post.

Term Papers Due this Friday

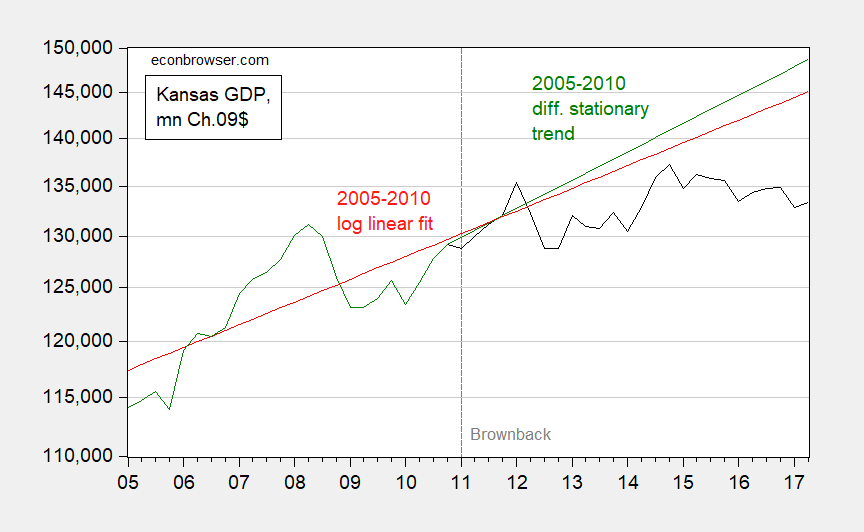

Kansas and Missouri GDP Trends since Brownback

Figure 1: Kansas real GDP in mn.Ch.2009$ SAAR (black) and log linear deterministic trend based on 2005-2010 (red), a log difference stationary fit* (green) all on log scale. Source: BEA and author’s calculations.

“Financial Spillovers and Macroprudential Policies”

That’s the title of a new paper by Joshua Aizenman, Hiro Ito and me.

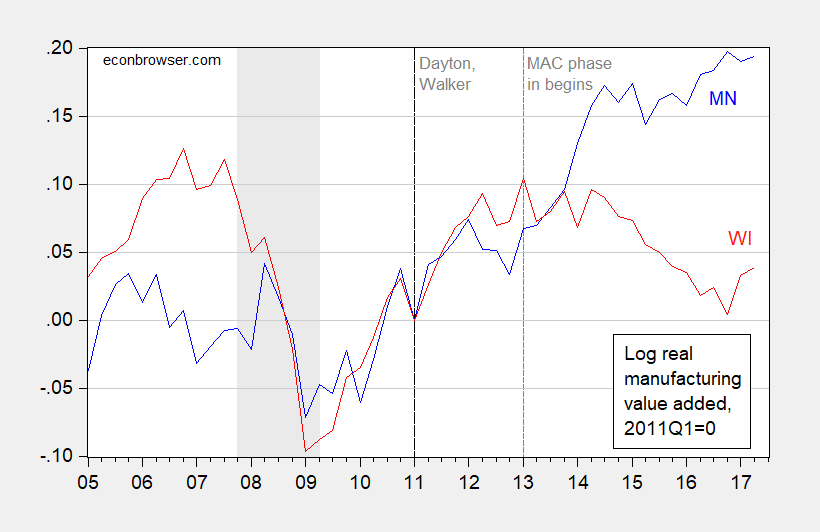

Wisconsin Output since Implementation of the MAC

The Manufacturing and Agriculture Credit, that is.

Continue reading

Wildfires: Acres Burned to Date

Not a record year yet, but still devastating. The upward trend in acres burned is shown below.

Continue reading

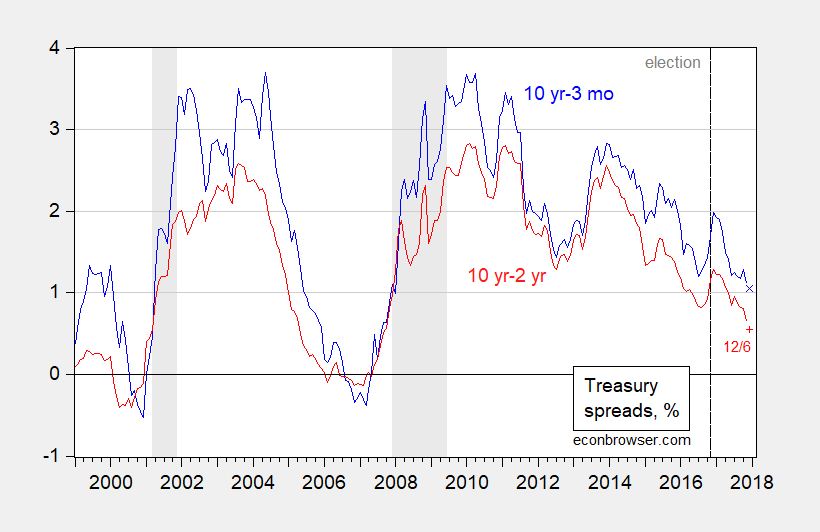

Post-War, How Many Times Has the 10yr-3mo Spread Fallen below 1% Without a Recession Following?

Three times.

Figure 1: Ten year minus three month Treasury spread (blue), and ten year minus three month Treasury spread (blue). December observations pertain to 12/6 daily observation. NBER defined recession dates shaded gray. Source: Federal Reserve via FRED, NBER and author’s calculations.

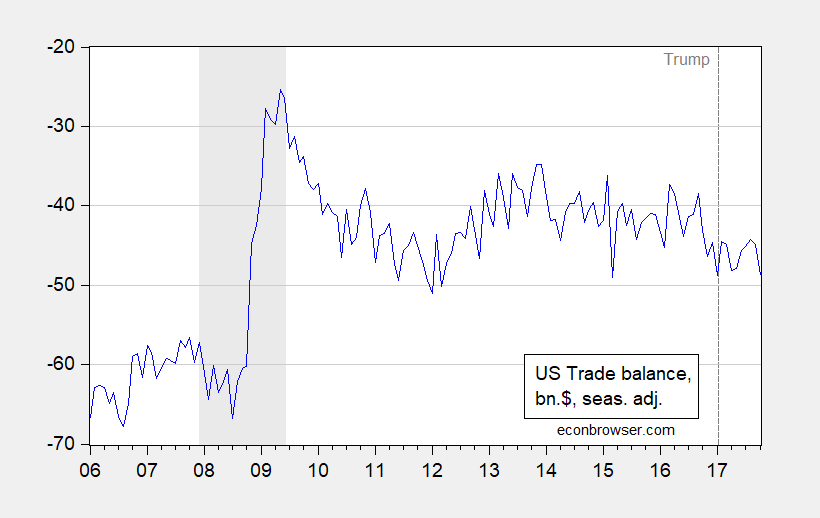

“We have trade deficits with everybody”

Thus spake the Mr. Trump, on a day that the October trade figures were released, indicating a deteriorating balance.

Figure 1: US trade balance, in billions $, seasonally adjusted (blue). NBER defined recession dates shaded gray. Source: BEA/Census via FRED, and NBER.

Continue reading

“Asset Prices and Macroeconomic Outcomes: A Survey”

That’s the title of an excellent review authored by two leading experts, Stijn Claessens and Ayhan Kose, that is required reading for anyone who wants to glean the implications of asset price movements for what’s going to happen in the real economy. From the conclusion:

Challenges to theoretical and empirical findings. The links between asset prices and activity differ from the predictions of standard models in a number of ways. First, asset prices are much more volatile than fundamentals would imply and can at times deviate, or at least appear to do so, from their predicted fundamental values. The term structure of interest rates is not fully consistent with the simple expectation hypothesis. Although exchange rates can be modelled as the present value of expected fundamentals, they appear to be overly volatile,

as is the case between equity prices and their underlying dividend streams (the puzzle of “excess volatility”). Moreover, macroeconomic and financial news seem to have an exaggerated effect on asset prices: equities, bonds and currencies overreact to news about cash flows and other fundamentals.

Where’s the Wisconsin Manufacturing Output Renaissance?

Employment in manufacturing may be estimated to be rising, but output seems to be trending sideways through 2nd quarter.

Figure 1: Log real manufacturing output in Minnesota (blue) and in Wisconsin (red), normalized to 2011Q1=0. NBER defined recession dates shaded gray. Vertical dashed line at 2013Q1 indicates beginning of Wisconsin Manufacturing and Agriculture Credit (MAC). Source: BEA, accessed 12/3/2017, NBER, and author’s calculations.