That’s a quote from candidate Donald J. Trump in May 2016. And today, he re-affirmed his predelictions, in his tax “sketch”.

Econometrically Assessing the President’s Tax Plan

Well, we don’t know for certain what he’s going to announce (and maybe even he doesn’t know what he will) — but according to Bloomberg…

President Donald Trump plans to propose a 10 percent tax on more than $2.6 trillion in earnings that U.S. companies have stockpiled offshore, said a White House official familiar with the president’s tax plans.

Proceeds from the so-called “repatriation tax” would represent a one-time source of sorely needed revenue, which could offset some of the deep tax cuts Trump has proposed for businesses — or could be devoted toward popular, bipartisan initiatives, like infrastructure spending.

Guest Contribution: “How to Re-Negotiate NAFTA”

Today, we present a guest post written by Jeffrey Frankel, Harpel Professor at Harvard’s Kennedy School of Government, and formerly a member of the White House Council of Economic Advisers. A shorter version appeared on April 22nd in Project Syndicate.

State Employment Trends: Some Selected States and ALEC Rankings

Since 2011 — when Scott Walker and Sam Brownback came into power — California has powered far ahead of Wisconsin and Kansas. The newly released Rich States, Poor States, 2017 allows us to look at how four states, both low and high ranked by Arthur Laffer et al., fared, employmentwise.

Doug Irwin on “The False Promise of Protectionism”

Why Trump’s Trade Policy Could Backfire

That’s a new Foreign Affairs essay out today by Doug Irwin, Professor of Economics at Dartmouth College:

Although Trump’s professed goal is to “get a better deal” on trade, his brand of economic nationalism is just one step away from old-fashioned protectionism. The president claimed that “protection will lead to great prosperity and strength.” Yet the opposite is true. An “America first” trade policy would do nothing to create new manufacturing jobs or narrow the trade deficit, the gap between imports and exports. Instead, it risks triggering a global trade war that would prove damaging to all countries. A slide toward protectionism would also undermine the institutions that the United States has long worked to support, such as the World Trade Organization (WTO), which have made meaningful contributions to global peace and prosperity.

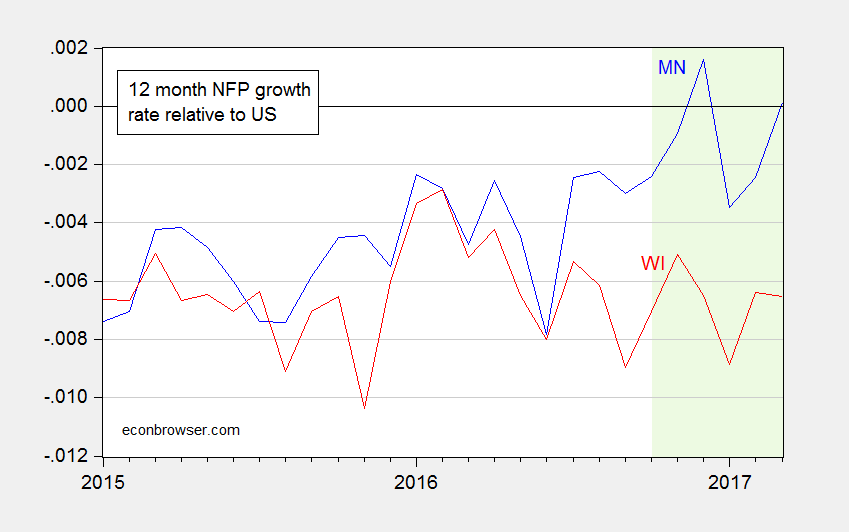

Minnesota Employment Growth Accelerates Relative to Wisconsin (Again)

Wisconsin and Minnesota released March employment figures today. Here, without comment (as none are needed) are year-on-year growth rates relative to the US average for Minnesota (blue) and Wisconsin (red).

Figure 1: 12 month log-differences of nonfarm payroll employment for Minnesota (blue) and Wisconsin (red), relative to US. Green shading denotes sample not updated to reflect QCEW-related benchmarking. Source: WI DWD, MN DEED, BLS, and author’s calculations.

Technically Correct, but Betraying a Certain Mindset

From the Washington Examiner:

I really am amazed that a judge sitting on an island in the Pacific can issue an order that stops the president of the United States from what appears to be clearly his statutory and constitutional power”

China’s tetralemma

Many countries have three policy objectives: (1) being able to set their own monetary policy, in order to keep their own inflation and unemployment at desired levels; (2) having a stable exchange rate, in order to avoid disruptive shifts in exports or imports; and (3) allowing free capital flows, in order to help the country’s citizens and firms find the most efficient sources and uses of capital. But the famous policy trilemma of international economics claims that any country is going to be forced to give up on one of those three goals.

Continue reading

Treasury Semi-Annual Report to Congress on Foreign Exchange Policies Released

The report, released yesterday, is here.

“Major Challenges for Global Macroeconomic Stability: The Role of the G7”

That was the title of a conference organized by Istituto Affari Internazionale (with support of the Italian Ministry of Foreign Affairs and International Cooperation and Banca d’Italia) that I attended a couple of weeks ago in Rome.