The Chinn-Ito index revised and updated to 2014 is now available here.

Guest Contribution: “How to Save the UK (Inside the EU)”

Today, we are pleased to present a guest column written by Jeffrey Frankel, Harpel Professor at Harvard’s Kennedy School of Government, and formerly a member of the White House Council of Economic Advisers.

I see a possible way out for the trap that Brits now find themselves in, a way to keep Great Britain great.

Policy Uncertainty (in America) in the Wake of Brexit

I find it remarkable that, going by the numbers, economic policy uncertainty is now higher than after the bankruptcy of Lehman — and even higher than in the days after 9/11.

Economic consequences of Brexit

Here are my two pence on some of the consequences of Britain’s vote to leave the European Union.

Continue reading

Guest Contribution: “Does the Economy Really Do Better Under Democratic Presidents?”

Today, we are pleased to present a guest column written by Jeffrey Frankel, Harpel Professor at Harvard’s Kennedy School of Government, and formerly a member of the White House Council of Economic Advisers. This is an extended version of a column appearing at Project Syndicate.

Looking at the UK Economy, Post-Brexit

Here are some assessments of the economic impact on the UK economy, over the short (business cycle horizon) to long run.

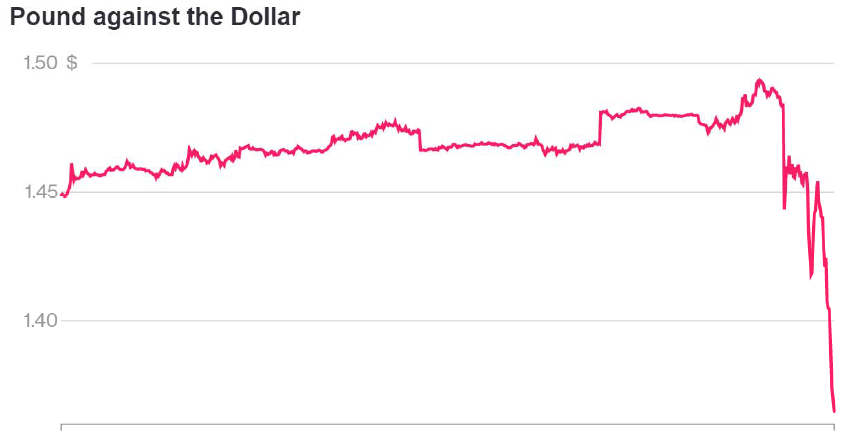

The Pound, 4AM London Time

As assessed probability of Brexit rises, the pound falls.

USD per Pound, last 5 days, as of 4AM London time. Source: Bloomberg.

Pound is down 9.29% against USD since London close (5PM local).

Kansas and Her Neighbors: GDP Edition

Some critics (e.g., [1]) have argued that employment and coincident indicators are too narrow of measures of economic activity to make relevant comparisons. Here I plot the real GDP — the broadest measure of economic activity — for Kansas and her neighbors.

Guest Contribution: “The Effects of Unconventional and Conventional U.S. Monetary Policy: The Role of Expected Inflation”

Today we are pleased to present a guest contribution by Yi Zhang, Ph.D. candidate at the University of Wisconsin-Madison. This post draws upon this paper.

Drumpfarmageddon, Tabulated

Heretofore, I’ve approached in a piecemeal manner the assessment of the impact of massive tax cuts for the wealthy, building a really, really great wall, a final solution for the presence of undocumented immigrants, and the imposition a 45% tariff on Chinese imports. Moody’s Mark Zandi et al. have now done the hard work of trying to figure out what the macro impacts would be to implementing Mr. Trump’s agenda.