Last week marked the tenth anniversary of Econbrowser. That gives me an occasion to talk a little about why I started the blog and what we’ve accomplished with it.

Continue reading

One Department to Rule Them All

Not my idea! With apologies to JRR Tolkein.

One the Regents candidates nominated by Governor Walker (from Wisconsin Public Radio):

Gov. Scott Walker’s latest appointment to the University of Wisconsin Board of Regents told a state Senate panel on Thursday that the UW should consider eliminating duplicative degree programs on some campuses.

Assessing the Rational Agent Response to Elimination of Tenure in Wisconsin State Statute

Thinking about “Exit, Voice and Loyalty” in Wisconsin

The Joint Finance Committee motion to remove tenure from state statute. Winners of the most competitive research awards the University of Wisconsin–Madison provides to its scholars have made a statement, found here.

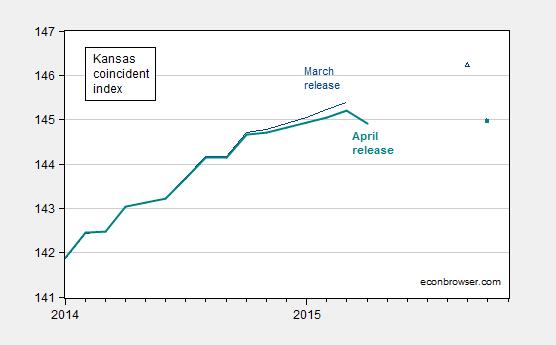

A Parsimonious Error Correction Model of Kansas Economic Activity

Or “Kansas macro crash…and burn”

Patrick Marvin argues that Kansas is doing fine, and the tax cuts just need a bit more time to kick in to spur the economy. My reading of the data and estimates suggest otherwise.

Figure 1: Coincident index for Kansas, March release (dark blue), April release (bold teal). Dark blue triangle (solid teal box) denote corresponding forecasts from March and April releases of leading indices. Source: Philadelphia Fed (coincident), Philadelphia Fed (leading), and author’s calculations.

Guest Contribution: “Inflation Expectations Spur Consumption Expenditure”

Today we are fortunate to have a guest contribution by Michael Weber, assistant professor at the University of Chicago’s Booth School of Business. This post is based upon a paper, co-authored with Francesco D’Acunto and Daniel Hoang.

Current economic conditions: not as bad as it sounds

On Friday the Bureau of Economic Analysis released its second estimate of U.S. 2015:Q1 real GDP growth. The BEA now estimates that the economy contracted at a 0.7% annual rate rather than grew 0.2% as originally estimated. The number is discouraging, though I see some silver linings.

Continue reading

Kansas Macro and Fiscal Crash

Economic activity stalls, and the Republicans conclude that higher taxes are necessary for higher tax revenue.

[with update 6/2 on the April forecast]

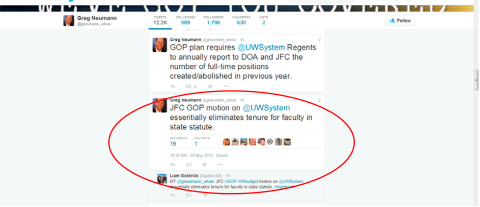

Wisconsin GOP Targets Faculty Tenure

From Greg Neumann/WKOW:

“JFC” is Joint Finance Committee. The text of the motion is here. Stein and Herzog/Journal Sentinel here. The article notes the following contrast: “Minnesota raised taxes with part of the new revenue set aside for higher education.”

“Crony Capitalism”: Wisconsin Edition

RightWisconsin writes:

…crony capitalism is currently wreaking havoc on the conservative Republican brand of free markets and limited government.

Gasoline prices and consumer sentiment

U.S. retail gasoline prices last week averaged over $2.80 a gallon, thirty cents higher than a month ago. The preliminary University of Michigan index of consumer sentiment for May was 88.6, down 7 points from the month before. Are these two developments related?

Continue reading