Today, we’re fortunate to have a guest contribution by Jeffry Frieden, Stanfield Professor of International Peace at Harvard University, and author of the newly published Currency Politics: The Political Economy of Exchange Rate Policy (Princeton University Press, 2015). This post is based upon a portion of that book.

Fed moves the markets

As widely expected, at Wednesday’s FOMC meeting the Federal Reserve dropped its statement that “the Committee judges that it can be patient in beginning to normalize the stance of monetary policy”, the magic formula that many observers had thought would open the way for a hike in interest rates at the Fed’s June meeting. But the yield on a 10-year U.S. Treasury bond dropped 10 basis points immediately following the FOMC release.

Continue reading

Guest Contribution: “Currency politics, debt politics”

Today, we’re fortunate to have a guest contribution by Jeffry Frieden, Stanfield Professor of International Peace at Harvard University, and author of the newly published Currency Politics: The Political Economy of Exchange Rate Policy (Princeton University Press, 2015). This post is based upon a portion of that book.

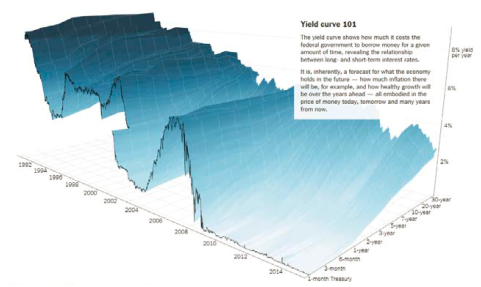

The Yield Curve and Economic Activity, Again

The New York Times has an article in The Upshot today, which shows the yield curve over time in a nifty map. They also show the topography for yields in Germany and Japan.

“Wisconsin job creation rank falls to 38th in U.S.”

That’s the title of an article by John Schmid and Kevin Crowe in the Milwaukee Journal Sentinel today, based upon just-released state level data on the Quarterly Census of Employment and Wages (QCEW):

Wisconsin gained 27,491 private-sector jobs in the 12 months from September 2013 through September 2014, a 1.16% increase that ties Wisconsin with Vermont and Iowa at a rank of 38th among the 50 states in the pace of job creation during that period.

Short Term Implications of the House Budget

The CBO took at face value the revenue and spending levels in the House Budget, FY2016, and assessed the impact on GNP per capita (remember, this is not a score, as there are few details on specific provisions to hit the targets). The impact is shown in Figure 2 from the CBO.

Some Implications of the Dollar’s Rise

Currency appreciation will be a drag; this implies a policy of slower monetary tightening is in order

U.S. oil supply update

The EIA released a new drilling productivity report last week, allowing us to update our graph of the drilling rig count in the four major tight oil regions. Active rigs in those areas are now 32% below their peak last October, the lowest level in 3 years.

Continue reading

2015 Econbrowser NCAA tournament challenge

It’s time to get ready for the world famous eighth annual Econbrowser NCAA tournament challenge, in which readers and friends of our blog are invited to demonstrate their skill (or luck) at predicting the outcome of the U.S. college mens’ basketball tournament. If you want to participate, go to the Econbrowser group at ESPN, do some minor registering to create a free ESPN account if you haven’t used that site before, and fill in your bracket some time between Sunday at 7:00 p.m. EDT and Thursday before noon.

The big question is whether anybody can beat Kentucky?

“For a few dollars more: Reserves and growth in times of crises”

This paper, coauthored with Matthieu Bussière (Banque de France), Gong Cheng (European Stability Mechanism), and Noëmie Lisack (EUI), is now published and online.